Compound growth, often heralded as the “eighth wonder of the world” by Albert Einstein, is arguably the most powerful concept in finance. Its ability to generate returns not just on your initial investment, but also on the accumulated interest from previous periods, makes it an indispensable tool for wealth creation. For anyone aspiring to achieve financial independence, build a robust retirement fund, or simply grow their savings effectively, understanding how to calculate and harness compound growth is not just beneficial—it’s essential. This article will demystify the mechanics of compound growth, provide a clear guide to its calculation, and explore its profound implications across various financial landscapes.

Understanding the Fundamentals of Compound Growth

At its core, compound growth is the process where the earnings from an asset are reinvested to generate additional earnings. Unlike simple growth, where interest is only earned on the initial principal, compound growth allows your money to grow exponentially by earning “interest on interest.” This seemingly subtle difference has a dramatic impact over time, turning modest sums into substantial wealth.

Simple Interest Explained

To fully appreciate the power of compounding, it’s helpful to first understand simple interest. Simple interest is calculated solely on the principal amount of a loan or deposit. For instance, if you invest $1,000 at a 5% simple annual interest rate, you would earn $50 each year, regardless of how long the money is invested. After 10 years, you would have earned $500 in interest, bringing your total to $1,500. While straightforward, simple interest lacks the dynamic growth potential that compounding offers.

The Power of Reinvestment

The magic of compound growth lies in reinvestment. When interest earned is added back to the principal, that larger principal then earns interest in the subsequent period. This continuous cycle of earning and reinvesting accelerates the growth of your investment over time. Imagine that same $1,000 investment at 5% annual compound interest. In the first year, you earn $50, bringing your total to $1,050. In the second year, you earn 5% on $1,050, which is $52.50, making your new total $1,102.50. This incremental increase in the base amount for interest calculation is what fuels exponential growth.

Key Variables Influencing Compound Growth

Several critical variables dictate the speed and magnitude of compound growth:

- Principal (P): This is the initial amount of money invested or borrowed. A larger principal will naturally lead to a larger absolute return, given the same rate and time.

- Interest Rate (r): Expressed as a decimal (e.g., 5% is 0.05), this is the annual percentage rate at which your investment grows. Higher rates significantly accelerate growth.

- Compounding Frequency (n): This refers to how often the interest is calculated and added to the principal within a year (e.g., annually, semi-annually, quarterly, monthly, daily). More frequent compounding leads to faster growth.

- Time (t): The duration, in years, over which the money is invested or borrowed. This is arguably the most crucial factor, as compounding effects are most pronounced over long periods.

The Compound Growth Formula Demystified

Calculating compound growth doesn’t require advanced mathematics; a simple yet powerful formula can do the job. Understanding this formula is key to predicting your investment’s future value and making informed financial decisions.

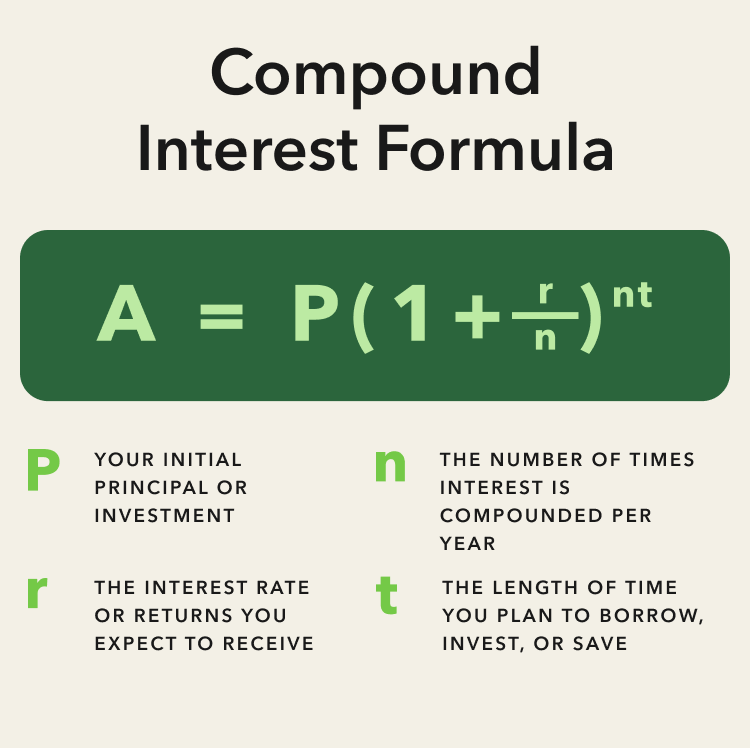

The standard formula for calculating compound growth is:

A = P (1 + r/n)^(nt)

Let’s break down each component:

- A = The future value of the investment/loan, including interest. This is the amount you want to find.

- P = The principal investment amount (the initial deposit or loan amount).

- r = The annual interest rate (as a decimal).

- n = The number of times that interest is compounded per year.

- t = The number of years the money is invested or borrowed for.

Identifying Your Variables

Before applying the formula, clearly identify each variable based on your specific scenario:

- Principal (P): How much are you starting with?

- Annual Interest Rate (r): What is the stated annual interest rate? (Remember to convert percentage to decimal, e.g., 6% becomes 0.06).

- Compounding Frequency (n): How often is the interest added?

- Annually: n = 1

- Semi-annually: n = 2

- Quarterly: n = 4

- Monthly: n = 12

- Daily: n = 365

- Time (t): For how many years will the investment grow?

Applying the Formula

Once you have identified your variables, simply plug them into the formula and solve. Remember the order of operations (PEMDAS/BODMAS): parentheses first, then exponents, then multiplication.

Practical Example Walkthrough

Let’s calculate the future value of an investment of $10,000 at an annual interest rate of 5% compounded quarterly over 10 years.

-

Identify Variables:

- P = $10,000

- r = 0.05 (5%)

- n = 4 (compounded quarterly)

- t = 10 years

-

Plug into the Formula:

A = 10,000 * (1 + 0.05/4)^(4*10)

A = 10,000 * (1 + 0.0125)^(40)

A = 10,000 * (1.0125)^(40) -

Calculate:

(1.0125)^(40) ≈ 1.6436

A = 10,000 * 1.6436

A = $16,436

So, after 10 years, your initial $10,000 investment would grow to approximately $16,436, having earned $6,436 in interest. If this were simple interest, you would have only earned $5,000 ($500 per year for 10 years). The power of compounding is evident.

Variations in Compounding Frequency

The frequency of compounding significantly impacts the final accumulated amount.

- Annual Compounding: Interest is added once a year (n=1). This is the simplest form but often yields the least growth compared to more frequent options.

- Semi-Annual, Quarterly, and Monthly Compounding: As ‘n’ increases, so does the final amount, albeit with diminishing returns. For example, compounding monthly (n=12) means interest is calculated and added back to the principal 12 times a year, leading to slightly higher returns than quarterly (n=4) or semi-annual (n=2) compounding for the same annual rate.

- Continuous Compounding: In theory, continuous compounding represents the maximum limit of compounding frequency, where interest is compounded an infinite number of times. While rarely encountered in practical personal finance (banks typically use daily), it’s a concept used in advanced financial modeling. Its formula involves the mathematical constant ‘e’.

Beyond the Basics: Practical Applications and Considerations

Understanding compound growth is not merely an academic exercise; it’s a fundamental principle that underpins strategic financial planning and wealth accumulation. Its impact extends across various facets of personal and business finance.

Compound Growth in Investing

The most common application of compound growth is in investment. Whether you’re saving for retirement, a child’s education, or a down payment on a house, compounding is your greatest ally.

- Retirement Planning (401k, IRAs): These tax-advantaged accounts are perfect vehicles for harnessing compound growth. Contributions grow over decades, often reinvesting dividends and capital gains, leading to substantial nest eggs by retirement. The earlier you start, the more time compounding has to work its magic.

- Stock Market Investments and Dividends: When you invest in stocks, any dividends received can be reinvested to buy more shares, thus increasing your principal and accelerating future dividend income and capital appreciation. This is known as dividend reinvestment plans (DRIPs).

- Real Estate Investments: Rental income, when reinvested into property improvements or additional properties, can also create a compounding effect, increasing property value and future income streams.

The Impact of Time and Rate

Two variables have a disproportionately large impact on compound growth: time and the interest rate.

- The “Rule of 72”: This handy rule of thumb provides a quick estimate of how long it will take for an investment to double in value. Simply divide 72 by the annual interest rate. For example, at a 6% annual rate, an investment would roughly double in 12 years (72/6 = 12). While an approximation, it effectively illustrates the power of compounding.

- Starting Early: The Biggest Advantage: Due to the exponential nature of compounding, the earlier you begin investing, the less you generally need to contribute to achieve your financial goals. A dollar invested today has far more growth potential than a dollar invested 10 or 20 years from now. This is why financial advisors consistently stress the importance of early saving.

- Small Differences in Rate Over Long Periods: Even a seemingly small difference in the annual interest rate (e.g., 1-2%) can lead to a dramatically different outcome over a long investment horizon. This underscores the importance of seeking out the best possible rates for your savings and investments.

The Dark Side: Compound Debt

While compound growth is a powerful force for wealth creation, it can also work against you in the form of compound debt.

- Credit Cards and Loans: How Compounding Works Against You: High-interest debts, particularly credit card debt, leverage the same compounding principle. If you only make minimum payments, the unpaid interest is added to your principal, and then you’re charged interest on that new, higher principal. This can lead to a vicious cycle where debt grows rapidly, making it incredibly difficult to pay off. Understanding how to calculate compound growth helps you see the true cost of prolonged debt and motivates you to pay it off swiftly.

Leveraging Tools for Easier Calculation and Planning

While the compound growth formula is straightforward, performing repeated calculations or running multiple scenarios manually can be cumbersome. Fortunately, a variety of tools can simplify this process and enhance your financial planning.

Online Compound Interest Calculators

These readily available online tools are perhaps the easiest way to compute future values. They typically require you to input the principal, interest rate, compounding frequency, and time horizon, then instantly provide the result.

- Benefits of Using Digital Tools:

- Speed and Accuracy: Eliminates manual calculation errors and provides instant results.

- Scenario Planning: Allows you to quickly adjust variables (e.g., change interest rate, add more contributions) to see how different choices impact your outcome. This is invaluable for exploring various financial strategies.

- Visualization: Many calculators offer charts or graphs that visually demonstrate the growth over time, making the concept more tangible.

- Key Features to Look For:

- Ability to add regular contributions (e.g., monthly deposits).

- Option to change compounding frequency.

- Clear display of total interest earned vs. total principal contributed.

Spreadsheet Applications (Excel/Google Sheets)

For those who prefer a more customized approach or need to integrate compound growth calculations into broader financial models, spreadsheet applications like Microsoft Excel or Google Sheets are excellent choices.

- Setting Up a Compound Interest Spreadsheet: You can easily create a table to track principal, interest earned, and ending balance year by year (or period by period). This provides a granular view of how your money grows.

- Using Financial Functions: Spreadsheets come equipped with powerful financial functions. The

FV(Future Value) function is specifically designed for compound interest calculations.FV(rate, nper, pmt, [pv], [type])rate: The interest rate per period (e.g., 0.05/12 for monthly compounding).nper: The total number of payment periods (e.g., 10 years * 12 months/year = 120).pmt: The payment made each period (e.g., monthly contributions).pv: The present value, or the lump-sum amount that a series of future payments is worth right now (this would be your principal, entered as a negative value).type: (Optional) When payments are due (0 for end of period, 1 for beginning).

Financial Advisors and Planning Software

For complex financial situations, multi-faceted goals, or a desire for expert guidance, consulting a financial advisor or utilizing advanced financial planning software can be highly beneficial.

- When Professional Guidance is Beneficial: A financial advisor can help you understand how compound growth applies to your entire financial picture, including investments, debt management, retirement planning, and estate planning. They can also assist with sophisticated calculations that factor in inflation, taxes, and fluctuating market conditions. Planning software offers comprehensive tools to model various scenarios, project long-term growth, and track progress toward financial objectives.

Conclusion

The ability to calculate compound growth is a cornerstone of financial literacy and a prerequisite for successful long-term financial planning. From understanding its fundamental principles to mastering the formula and leveraging modern tools, every step toward grasping this concept empowers you to make smarter decisions with your money.

Remember that time and consistent reinvestment are your most valuable assets when it comes to compounding. By starting early, contributing regularly, and understanding how interest rates and compounding frequency influence your returns, you can effectively harness this “eighth wonder” to build substantial wealth and achieve your financial aspirations. Whether you are planning for retirement, saving for a major purchase, or simply aiming to grow your savings, embracing the power of compound growth is the surest path to financial prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.