In the labyrinthine world of personal finance, understanding how your money grows or costs you is paramount. Among the myriad of financial metrics, Annual Percentage Yield (APY) stands out as a critical indicator for assessing the true return on an investment or the real cost of a loan, particularly when compound interest is at play. Far more insightful than its simpler cousin, the Annual Percentage Rate (APR), APY reflects the effect of compounding interest, painting a more accurate picture of your financial reality.

While the mathematical formula for APY might seem daunting at first glance, the proliferation of online APY calculators has democratized this crucial financial analysis, empowering individuals to make informed decisions without needing a degree in advanced mathematics. However, merely inputting numbers into a tool without understanding the underlying principles is akin to driving a car without knowing how an engine works – you can get to your destination, but you won’t truly grasp the journey or how to troubleshoot problems.

This article aims to demystify APY, dissect its manual calculation, explore the utility of an APY calculator, and highlight how this knowledge can be strategically applied to optimize your financial well-being. By the end, you’ll not only know how to use an APY calculator effectively but also comprehend the “why” behind its calculations, transforming you from a passive user into an astute financial planner.

Demystifying APY: The Power of Compounding

To fully appreciate an APY calculator, we must first firmly grasp what APY represents and why it holds such significance in financial planning. It’s more than just a number; it’s a window into the true growth potential or cost of your money.

What is APY?

APY, or Annual Percentage Yield, is a standardized metric used to express the real rate of return earned on an investment or paid on a savings account over a year, taking into account the effect of compounding interest. Unlike the nominal interest rate or APR, which only considers the simple interest charged or earned, APY includes the interest earned on previously accumulated interest. This distinction is crucial because it reflects the actual percentage of growth your principal experiences over a year. For instance, if you deposit money into a savings account that compounds interest monthly, the interest earned in the first month will itself earn interest in subsequent months, leading to a higher overall return than a simple interest calculation would suggest.

Why APY Matters More Than APR

The critical difference between APY and APR lies in the treatment of compounding interest. APR (Annual Percentage Rate) represents the simple interest rate charged or earned on an investment or loan over a year, without considering the effects of compounding. It’s often used for loans like credit cards or mortgages, where the interest is typically calculated on the principal amount (though mortgage APRs can also include fees, making comparison complex).

For financial products where you earn interest (e.g., savings accounts, Certificates of Deposit (CDs)), APY is the more accurate measure of your actual return. A bank might advertise an attractive nominal interest rate (APR) of 5%, but if that interest compounds daily, the actual APY will be slightly higher, perhaps 5.12%. This seemingly small difference can accumulate significantly over time, making APY the superior metric for comparing different savings or investment opportunities. Always look for the APY when evaluating where to park your cash to earn interest.

The Magic of Compound Interest

The core principle that elevates APY’s importance is compound interest, often hailed as the “eighth wonder of the world” by Albert Einstein. Compound interest is the interest on interest. It’s the process where the interest earned on an investment or loan is added to the principal, and subsequent interest calculations are made on this new, larger principal.

For savers and investors, compound interest is a powerful ally. It allows your money to grow exponentially over time. For example, if you invest $1,000 at a 5% APY compounded annually, after the first year, you’ll have $1,050. In the second year, the 5% interest is calculated on $1,050, yielding $52.50 in interest, bringing your total to $1,102.50. This snowball effect accelerates over time, demonstrating why starting early and maximizing compounding frequency are vital for long-term wealth creation. Conversely, for borrowers, compound interest can lead to rapidly accumulating debt if not managed effectively, as interest on unpaid balances can quickly inflate the total amount owed.

The Manual Calculation of APY: A Step-by-Step Guide

While APY calculators simplify the process, understanding the underlying formula empowers you to grasp the mechanics and interpret results with greater insight. The manual calculation of APY essentially derives the Effective Annual Rate (EAR).

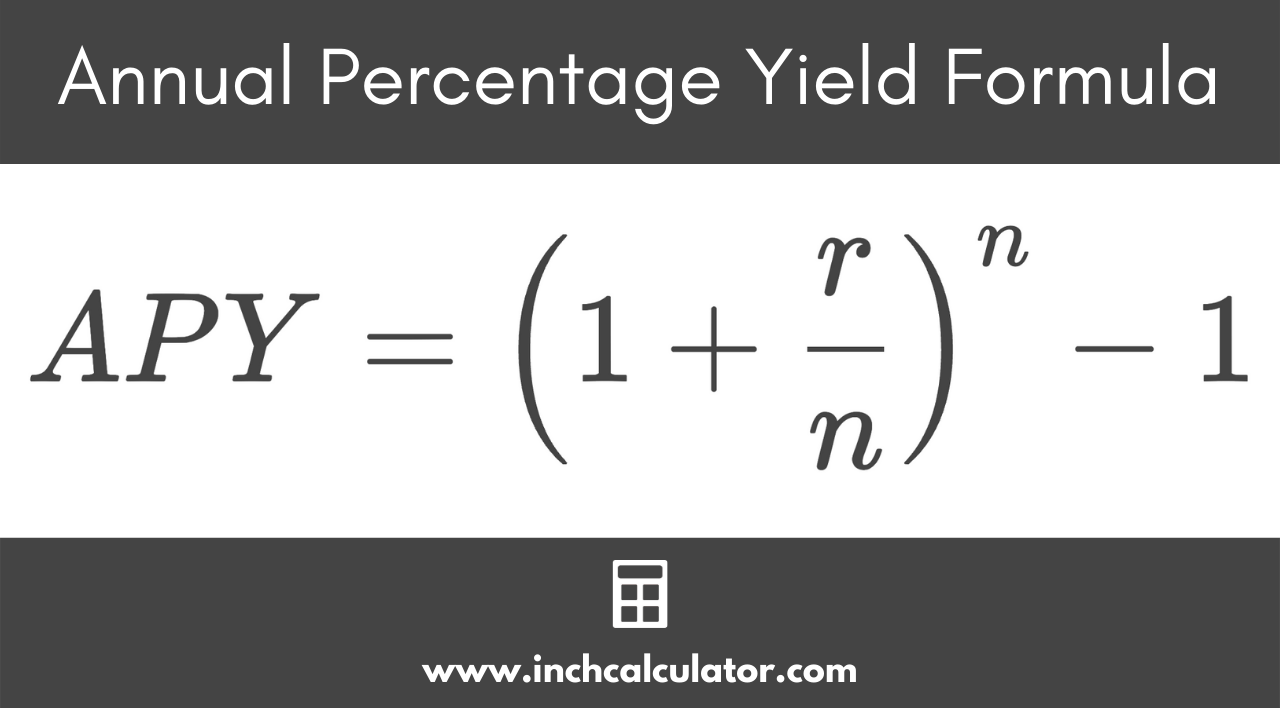

Formula Breakdown: Effective Annual Rate (EAR)

The formula for calculating the Effective Annual Rate (EAR), which is synonymous with APY, is as follows:

APY = (1 + (Nominal Rate / Number of Compounding Periods))^Number of Compounding Periods – 1

Let’s break down each component:

- Nominal Rate (or Stated Rate): This is the advertised interest rate, usually expressed as an Annual Percentage Rate (APR). It should be converted to a decimal for the calculation (e.g., 5% becomes 0.05).

- Number of Compounding Periods (n): This refers to how many times the interest is compounded within a single year.

- Annually: n = 1

- Semi-annually: n = 2

- Quarterly: n = 4

- Monthly: n = 12

- Daily: n = 365 (or 360 for some financial institutions, but 365 is standard for APY)

The formula calculates the total growth factor over one year by adding the interest rate per period to 1, raising it to the power of the total number of periods, and then subtracting the initial principal (represented by 1) to isolate the yield.

Example Calculation for Savings Accounts

Let’s walk through an example. Suppose you find a savings account offering a nominal interest rate of 2.5% compounded monthly.

-

Identify the Nominal Rate: 2.5% = 0.025

-

Identify the Number of Compounding Periods (n): Monthly means n = 12

-

Apply the Formula:

APY = (1 + (0.025 / 12))^12 – 1

APY = (1 + 0.00208333)^12 – 1

APY = (1.00208333)^12 – 1

APY = 1.025287 – 1

APY = 0.025287 -

Convert to Percentage: Multiply by 100 to get 2.5287%

So, an account with a 2.5% nominal rate compounded monthly actually yields an APY of approximately 2.53%. This small but significant difference highlights the power of compounding and why APY is the more accurate figure.

Adjusting for Different Compounding Frequencies

The number of compounding periods (n) is the variable that most significantly impacts the APY, assuming a constant nominal rate. The more frequently interest is compounded, the higher the APY will be, albeit marginally once compounding becomes very frequent (e.g., daily vs. continuously).

- Annual Compounding (n=1): APY = (1 + Nominal Rate/1)^1 – 1 = Nominal Rate. In this case, APY = APR.

- Semi-Annual Compounding (n=2): Interest is added twice a year.

- Quarterly Compounding (n=4): Interest is added four times a year.

- Daily Compounding (n=365): Interest is added every day. This typically results in the highest APY for a given nominal rate, as interest begins earning interest almost immediately.

Understanding how ‘n’ influences the APY allows you to make more precise comparisons between different financial products. For instance, a 3% nominal rate compounded semi-annually will yield a lower APY than a 3% nominal rate compounded daily.

Harnessing the APY Calculator: Your Financial Assistant

While understanding the manual calculation is invaluable for conceptual clarity, for speed, accuracy, and convenience, an APY calculator is an indispensable financial tool.

What an APY Calculator Does

An APY calculator is a specialized online tool or software designed to automate the APY formula. Instead of manually plugging numbers into a complex equation, you simply input the nominal interest rate and the compounding frequency. The calculator then instantly provides the corresponding APY. Many advanced calculators might also allow you to input an initial deposit and a time horizon to show the future value of your investment, further illustrating the impact of APY.

Benefits of Using an APY Calculator

- Accuracy and Speed: Eliminates human error in calculations and provides instant results, saving time and ensuring precision, especially with complex compounding frequencies.

- Ease of Comparison: Allows you to quickly compare different savings accounts, CDs, or investment opportunities advertised with varying nominal rates and compounding frequencies. You can input the details of multiple options and see their true APY side-by-side.

- Informed Decision-Making: By revealing the true rate of return, APY calculators empower you to make more informed decisions about where to save or invest your money to maximize growth.

- Illustrative Power: Many calculators can demonstrate the long-term impact of APY on your savings, showing how small differences in interest rates or compounding frequencies can lead to substantial differences in accumulated wealth over years or decades.

Key Inputs and Outputs

Most APY calculators require two primary inputs:

- Nominal Interest Rate: The advertised annual interest rate (e.g., 2.0%, 3.5%).

- Compounding Frequency: How often the interest is calculated and added to the principal (e.g., annually, semi-annually, quarterly, monthly, daily, continuously).

The primary output is the Annual Percentage Yield (APY), usually presented as a percentage. Some calculators may also show the “Effective Annual Rate (EAR)” or “True Interest Rate,” which are synonymous with APY. More sophisticated calculators might also output:

- Total Interest Earned: The absolute dollar amount of interest accrued over a specified period.

- Future Value: The total amount of money you would have after a certain number of years, considering your initial deposit, additional contributions (if applicable), and the calculated APY.

Strategic Application of APY Knowledge

Beyond just understanding the number, the true value of knowing how to calculate and interpret APY lies in its practical application to your financial decisions.

Comparing Savings and Investment Opportunities

One of the most immediate uses of APY knowledge is in comparing different savings vehicles. When banks advertise varying interest rates and compounding schedules, using an APY calculator allows you to normalize these offers to a single, comparable metric.

- Example: Bank A offers 2.0% compounded daily. Bank B offers 2.05% compounded semi-annually.

- Bank A (2.0% daily): APY ≈ 2.020%

- Bank B (2.05% semi-annually): APY ≈ 2.060%

In this scenario, despite Bank A’s more frequent compounding, Bank B’s slightly higher nominal rate results in a better APY, making it the more attractive option for earning interest. This kind of nuanced comparison is impossible without calculating or consulting the APY.

Understanding Loan Costs and Returns

While APY is predominantly used for earnings, its inverse logic applies to the cost of borrowing, though APR is more commonly advertised for loans. When a loan compounds interest frequently, the effective cost can be higher than the stated nominal rate. For instance, some payday loans or credit cards might quote a daily or monthly rate that, when annualized, results in an extremely high effective annual rate. Understanding the compounding effect, even if not explicitly termed “APY” for loans, helps you recognize the true cost of debt. Conversely, when evaluating investments that generate returns with compounding (like certain bonds or dividend reinvestment plans), comparing their APY provides a clearer picture of potential gains.

Long-Term Financial Planning

The power of APY becomes most evident in long-term financial planning, especially for retirement savings, education funds, or large purchase goals. Even a fraction of a percentage point difference in APY, compounded over decades, can lead to tens of thousands, or even hundreds of thousands, of dollars in difference in your final accumulated wealth.

By actively seeking out accounts and investments with the highest possible APY (commensurate with your risk tolerance), you leverage the power of compound interest to its fullest. An APY calculator, combined with a future value calculator, can project how your money will grow over time, motivating you to save more, invest wisely, and choose financial products that truly maximize your returns. This foresight is crucial for achieving financial independence and security.

In conclusion, understanding “how to calculate apy calculator” is more than just a technical exercise; it’s a fundamental skill in personal finance. It transforms abstract interest rates into tangible growth or cost, providing clarity and confidence in your financial decisions. By embracing APY, both through manual calculation and the efficient use of digital tools, you empower yourself to navigate the financial landscape with precision, optimizing your savings, investments, and ultimately, your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.