Investing in stocks has long been considered a cornerstone of wealth building, offering individuals a pathway to grow their capital beyond traditional savings. However, the seemingly simple question, “Where do you invest in stocks?”, unlocks a complex and dynamic landscape of choices. Gone are the days when a single, local brokerage firm was the only real option. Today, the market is teeming with platforms and services catering to every conceivable investor profile, from the seasoned trader to the absolute beginner, from those seeking hands-on control to others preferring automated management.

Navigating this diverse ecosystem requires more than just knowing a few names; it demands a deep understanding of your personal financial goals, risk tolerance, and the specific features each platform offers. This article will demystify the various avenues available for stock investment, guiding you through traditional brokerages, the latest online platforms, automated advisors, and niche services, empowering you to make an informed decision that aligns with your individual financial journey.

Understanding Your Investment Goals and Style

Before you even consider which platform to use, the most critical first step is to look inward. Your investment strategy should be a reflection of your personal financial situation, objectives, and comfort level with risk. Without a clear understanding of these foundational elements, even the most sophisticated platform might not serve you effectively.

Defining Your Investment Horizon

Your investment horizon dictates the timeframe over which you plan to keep your money invested. This is a crucial factor in determining your strategy and the types of investments you might consider.

- Short-term goals (e.g., saving for a down payment in 2-3 years) typically warrant more conservative investment approaches, often favoring instruments with lower volatility, even if it means lower potential returns. Stocks, particularly individual stocks, are generally not recommended for very short-term goals due to their inherent volatility.

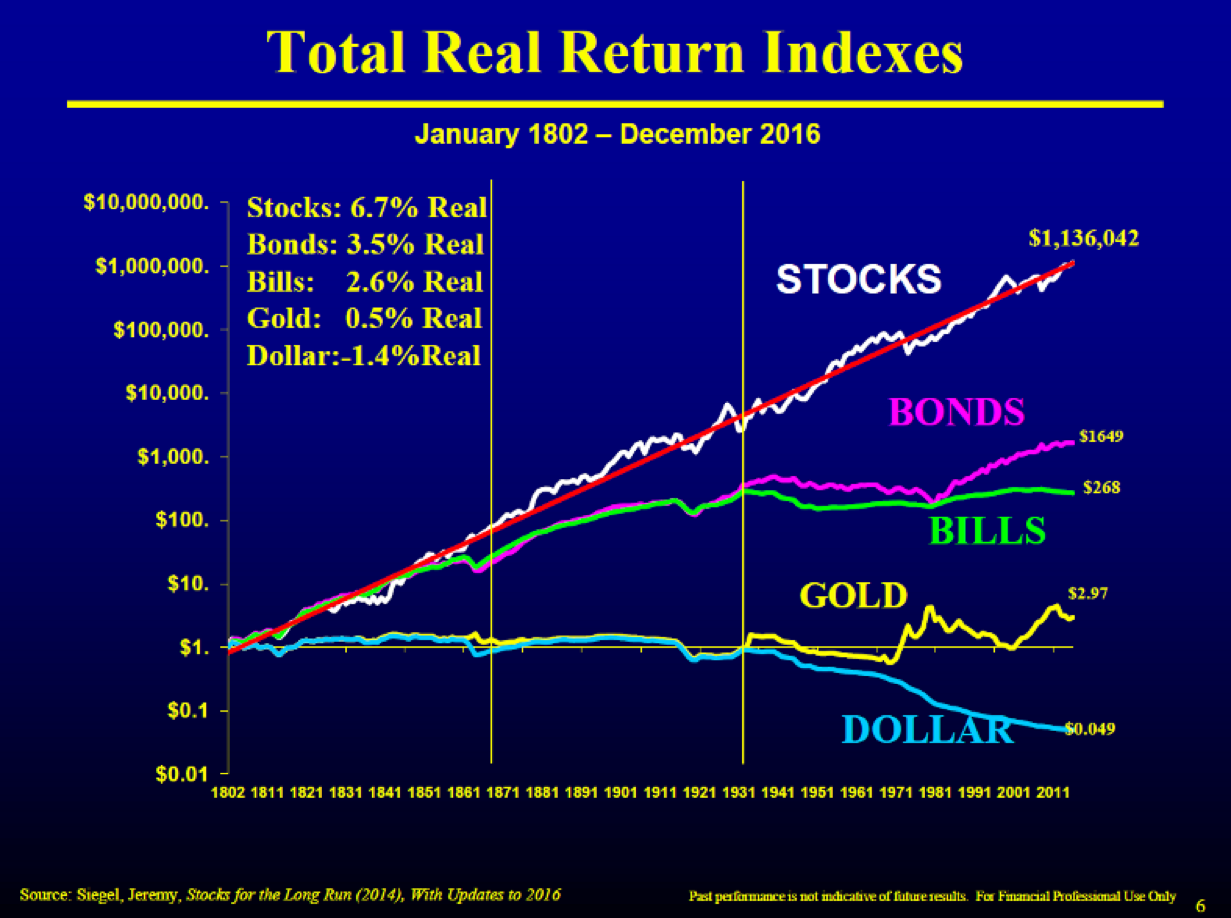

- Long-term goals (e.g., retirement planning in 20+ years, college savings for a newborn) provide a longer runway to ride out market fluctuations. This longer horizon makes stocks, especially diversified portfolios of stocks, an attractive option for their potential for significant growth over time. The power of compounding truly shines over decades. Your investment horizon will influence how aggressively or conservatively you allocate your assets and what type of platform might best support that allocation.

Assessing Your Risk Tolerance

Risk tolerance is a measure of how much financial risk you are willing and able to take in pursuit of higher returns. It’s a deeply personal metric, influenced by your financial stability, age, income, existing assets, and psychological comfort with potential losses.

- Aggressive investors are comfortable with significant market fluctuations and are willing to take on higher risk for the potential of greater returns. They might lean towards individual growth stocks, emerging markets, or more speculative ventures.

- Moderate investors seek a balance between growth and capital preservation. They might invest in a diversified mix of stocks and bonds, aiming for steady growth without extreme volatility.

- Conservative investors prioritize capital preservation over high returns. They often prefer stable, dividend-paying stocks, blue-chip companies, or a higher allocation to bonds and cash equivalents.

Understanding your risk tolerance isn’t just about what you say you can handle; it’s about what you actually can handle during a market downturn without panicking and making rash decisions. Most platforms will ask you to complete a risk assessment questionnaire to help guide your choices.

Active vs. Passive Investing

Your preferred level of involvement in managing your investments will also heavily influence your platform choice.

- Active investing involves regularly buying and selling securities in an attempt to outperform the market. This requires significant research, time commitment, and a strong understanding of market dynamics. Active investors might gravitate towards platforms with advanced trading tools, detailed research reports, and low commission fees.

- Passive investing, on the other hand, involves building a diversified portfolio that mirrors a market index (e.g., S&P 500) and holding it for the long term with minimal intervention. This strategy is based on the belief that it’s difficult to consistently beat the market. Passive investors often prefer low-cost index funds or Exchange Traded Funds (ETFs) and might find robo-advisors or platforms with robust ETF offerings more appealing. Your choice here impacts not only the platform’s features you’ll prioritize but also the fee structures you’ll find acceptable.

Traditional Brokerage Firms: The Established Path

Before the advent of widespread internet access, traditional brokerage firms were the primary gateways to the stock market. While the landscape has evolved dramatically, these firms continue to play a crucial role, offering a range of services from highly personalized advice to self-directed trading.

Full-Service Brokers

Full-service brokers are the quintessential “stockbrokers” of yesteryear, though their services have modernized. They offer a comprehensive suite of financial services, including personalized investment advice, financial planning, estate planning, tax guidance, and even insurance products.

- Benefits: The primary advantage is the access to human expertise. A dedicated financial advisor can help you craft a tailored investment strategy, provide insights into complex financial products, and offer guidance through market volatility. This hands-on, personalized approach is particularly valuable for individuals with complex financial situations, high net worth, or those who simply prefer a delegated approach to their investments.

- Drawbacks: The main disadvantage is cost. Full-service brokers typically charge higher fees, which can include a percentage of assets under management (AUM), commissions on trades, and various service fees. These costs can significantly eat into your returns over time. Examples include Merrill Lynch, Morgan Stanley, and UBS.

Discount Brokers

Discount brokers emerged as a more cost-effective alternative, focusing primarily on executing trades at a lower cost than their full-service counterparts. They empower self-directed investors by providing access to the market without the overhead of personalized advice.

- Cost-Effectiveness: Their main draw is significantly lower fees, often offering zero-commission trades on stocks and ETFs. This makes them highly attractive to investors who are comfortable making their own investment decisions and don’t require personal advisory services.

- Accessibility: Discount brokers have democratized investing, making it accessible to a broader range of individuals, including those with smaller initial capital. They provide the tools and platforms for you to research, buy, and sell securities yourself.

- Key Players: Well-known examples include Fidelity, Charles Schwab, and Vanguard. While originally “discount,” many of these firms have evolved to offer a blend of services, including extensive research tools, educational content, and even hybrid advisory options, blurring the lines with full-service firms.

Key Considerations for Traditional Brokers

When evaluating a traditional brokerage, whether full-service or discount, several factors warrant close attention:

- Research Tools: How robust are their research capabilities? Do they provide access to analyst reports, market data, charting tools, and screeners that align with your investment style?

- Customer Service: What is the quality and accessibility of their customer support? Do they offer phone, email, and chat support, and how quickly do they respond?

- Fees and Commissions: Beyond trade commissions, scrutinize all potential fees: account maintenance fees, transfer fees, inactivity fees, and mutual fund expense ratios. Transparency in fee structures is paramount.

- Account Types: Do they offer the specific account types you need (e.g., taxable brokerage, Roth IRA, Traditional IRA, 401(k) rollovers)?

The Rise of Online Brokerages and Robo-Advisors

The internet revolutionized investing, ushering in an era of unprecedented accessibility, lower costs, and innovative tools. Online brokerages and robo-advisors stand at the forefront of this transformation, catering to the modern investor’s demands for efficiency and affordability.

Online Brokerage Platforms

Online brokerage platforms are the digital evolution of discount brokers, providing investors with direct, self-directed access to financial markets through user-friendly websites and mobile applications. They have become the go-to for many individual investors due to their convenience and low-cost structure.

- User-Friendly Interfaces and Mobile Apps: Modern online brokerages prioritize intuitive design, making it easy to open accounts, fund them, research investments, and place trades from anywhere, at any time. Mobile apps offer unparalleled convenience, allowing investors to monitor portfolios and react to market news on the go.

- Low/Zero Commission Trading: One of the most significant shifts has been the widespread adoption of zero-commission trading for stocks and ETFs. This has drastically lowered the barrier to entry and encourages more frequent, smaller trades, although other fees may still apply.

- Comprehensive Features: Beyond basic trading, many online platforms offer a wealth of features: advanced charting tools, technical analysis indicators, options trading, margin accounts, extended trading hours, and access to a wide array of investment products including stocks, ETFs, mutual funds, and sometimes even cryptocurrencies.

- Educational Resources: Recognizing the need for investor education, many platforms provide extensive learning centers, webinars, articles, and tutorials to help users understand market concepts and platform functionalities.

- Key Players: Popular examples include E*TRADE (now part of Morgan Stanley), Fidelity, Charles Schwab, Robinhood, and Interactive Brokers. Each platform has its unique strengths, with some excelling in advanced trading tools for active traders (e.g., Interactive Brokers) and others prioritizing simplicity and ease of use for beginners (e.g., Robinhood).

Robo-Advisors: Automated Investing Solutions

Robo-advisors represent an innovative leap in automated financial advice. These platforms use algorithms to construct and manage diversified investment portfolios tailored to an individual’s financial goals and risk tolerance, with minimal human intervention.

- Algorithm-Driven Portfolios: After a user completes an initial questionnaire about their financial situation, goals, and risk appetite, the robo-advisor uses sophisticated algorithms to recommend and automatically manage a diversified portfolio, typically composed of low-cost ETFs. This takes the guesswork out of asset allocation and security selection.

- Low Fees: A major appeal of robo-advisors is their significantly lower advisory fees compared to traditional human financial advisors. Fees are usually a small percentage of assets under management (e.g., 0.25% to 0.50% annually), making them highly cost-effective for long-term investing.

- Passive Investing and Rebalancing: Robo-advisors are built on the principles of passive investing, focusing on long-term growth through diversification and market-tracking index funds. They automatically rebalance portfolios to maintain the target asset allocation, ensuring the portfolio stays aligned with the investor’s risk profile without requiring manual adjustments.

- Suitability: They are ideal for beginners, investors with smaller capital, or those who prefer a hands-off approach to wealth management. They simplify the investment process, making sophisticated portfolio management accessible to everyone.

- Key Players: Leading robo-advisors include Betterment, Wealthfront, and Vanguard Digital Advisor. Many traditional brokerage firms have also launched their own robo-advisor services to compete in this growing segment.

Hybrid Models

Recognizing that some investors might appreciate both the affordability of automation and the reassurance of human guidance, many platforms now offer hybrid models. These services combine the algorithmic efficiency of robo-advisors with access to human financial advisors for more complex planning needs or personalized consultations. This blended approach offers a middle ground, providing a balance between cost-effectiveness and personalized support, ideal for investors whose needs evolve beyond basic automated management.

Exploring Niche Investment Platforms and Options

Beyond the mainstream online brokerages and robo-advisors, a growing number of niche platforms and specialized investment options cater to specific investor needs, interests, or capital constraints. These can offer unique ways to engage with the stock market or broaden your investment horizons.

Micro-Investing Apps

Micro-investing apps are designed to make investing accessible to everyone, regardless of their budget. They allow individuals to invest very small amounts of money, often by rounding up debit/credit card purchases or making small, recurring contributions.

- Accessibility for Beginners: These apps are excellent entry points for new investors who might feel intimidated by traditional brokerage minimums or the perceived complexity of investing. They foster a habit of regular saving and investing without requiring significant lump sums.

- Examples: Acorns, for instance, rounds up spare change from everyday purchases and invests it into a diversified portfolio of ETFs. Stash allows users to invest in fractional shares of individual stocks and ETFs, curated around themes or companies they believe in. These platforms demystify the process and make starting an investment journey incredibly simple.

ESG (Environmental, Social, Governance) Investing Platforms

ESG investing, also known as sustainable or ethical investing, has gained significant traction as investors increasingly seek to align their financial goals with their personal values. ESG platforms focus on companies that demonstrate strong performance in environmental stewardship, social responsibility, and corporate governance.

- Values-Based Investing: These platforms allow investors to build portfolios that support companies committed to sustainability, fair labor practices, diversity, and ethical leadership.

- Specialized Screening: They often provide proprietary screening tools and research to help identify companies that meet specific ESG criteria, making it easier for investors to make impactful choices.

- Examples: Platforms like Ethic and OpenInvest (now part of JP Morgan Chase) offer customized ESG portfolios. Many traditional and online brokers also now offer ESG-focused ETFs and mutual funds, allowing investors to integrate these considerations into broader portfolios.

Fractional Share Investing

Fractional share investing is a game-changer for many, allowing investors to buy a fraction of a single share of stock rather than being limited to full shares. This innovation addresses the challenge of investing in high-priced stocks (e.g., Amazon, Google) with limited capital.

- Lower Barrier to Entry: Instead of needing hundreds or thousands of dollars to buy one share of a blue-chip company, you can invest just a few dollars. This enables greater diversification even with a small budget.

- Accessibility to Expensive Stocks: It democratizes access to stocks that were previously out of reach for many small investors, allowing them to participate in the growth of leading companies.

- Widespread Adoption: Many major online brokerages, including Fidelity, Charles Schwab, Robinhood, and M1 Finance, now offer fractional share investing, making it a standard feature for modern investors.

Direct Stock Purchase Plans (DSPs) and Dividend Reinvestment Plans (DRIPs)

For investors keen on owning shares directly from a company, DSPs and DRIPs offer a unique route.

- Direct Stock Purchase Plans (DSPs): These plans allow individuals to buy stock directly from the company itself, bypassing a traditional broker. They are typically offered by larger, well-established companies and often have minimal fees, though minimum initial investments might apply.

- Dividend Reinvestment Plans (DRIPs): DRIPs allow investors to automatically reinvest cash dividends received from a company back into purchasing additional shares or fractional shares of that company’s stock. This is a powerful way to leverage compounding interest without incurring additional transaction costs.

- Long-term Holding Strategy: Both DSPs and DRIPs are particularly suited for long-term investors focused on accumulating shares in specific companies over time, often for a lower cost basis and benefiting from compounding through dividend reinvestment.

Essential Factors When Choosing an Investment Platform

With such a vast array of options, making the right choice can seem daunting. To simplify the decision-making process, it’s crucial to evaluate potential investment platforms against a consistent set of criteria that align with your individual needs.

Fees and Commissions

This is often the most straightforward, yet frequently overlooked, aspect. Fees can significantly erode your investment returns over time, so understanding the complete cost structure is paramount.

- Trading Commissions: While many platforms now offer zero-commission trading for stocks and ETFs, verify this for all asset classes you might be interested in (e.g., options, mutual funds).

- Advisory Fees: If you opt for a robo-advisor or a hybrid model, understand the percentage of assets under management (AUM) they charge annually.

- Account Maintenance Fees: Some platforms charge fees for maintaining an account, especially if it falls below a certain balance or if there’s no activity.

- Inactivity Fees: Similar to maintenance fees, these can be levied if you don’t make trades or maintain a certain level of activity.

- Transfer Fees: If you decide to move your account to another broker, check for potential outbound transfer fees.

- Expense Ratios: For mutual funds and ETFs, pay close attention to the expense ratio, which is the annual fee charged by the fund itself. Lower expense ratios are generally better.

Available Investment Products

Ensure the platform offers access to the types of investments you plan to use in your portfolio.

- Stocks: Individual stocks (domestic, international), fractional shares.

- ETFs (Exchange Traded Funds): A diversified basket of securities that trades like a stock.

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other investments.

- Bonds: Government, municipal, or corporate bonds.

- Options and Futures: More complex derivative instruments for advanced traders.

- Cryptocurrencies: A growing number of traditional brokers are now offering crypto trading.

- International Markets: Access to foreign exchanges if you plan to diversify globally.

User Experience and Tools

A platform’s usability and the quality of its tools can significantly impact your investing experience, especially if you plan to be self-directed.

- Platform Interface: Is it intuitive, easy to navigate, and visually appealing?

- Mobile App: Does the mobile app offer full functionality, or is it a stripped-down version? Is it stable and responsive?

- Research Capabilities: What kind of research resources are available? Are there stock screeners, analyst reports, news feeds, economic calendars, and educational content?

- Charting Tools: For active traders, robust and customizable charting tools are essential.

- Trade Execution: How quickly and reliably are trades executed?

Customer Support and Education

Even the most experienced investors may occasionally need assistance.

- Accessibility: How can you reach customer support (phone, email, live chat)? What are their hours of operation?

- Quality of Support: Are representatives knowledgeable and helpful?

- Educational Resources: Does the platform offer articles, videos, webinars, or courses to help you learn about investing and use their tools effectively?

Security and Regulation

Protecting your investments and personal information is paramount.

- SIPC (Securities Investor Protection Corporation) Insurance: Most legitimate U.S. brokerage firms are SIPC members, which protects customer securities up to $500,000 (including $250,000 for cash) in case the brokerage firm fails. This does not protect against market losses.

- FDIC (Federal Deposit Insurance Corporation) Insurance: For any uninvested cash held in sweep accounts, ensure it’s FDIC-insured, typically up to $250,000 per depositor.

- Regulatory Compliance: Ensure the firm is registered and regulated by relevant authorities like the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) in the U.S.

- Account Security: Look for features like two-factor authentication, encryption, and other cybersecurity measures to protect your account from unauthorized access.

Conclusion

The question “Where do you invest in stocks?” is fundamentally a personal one, with no single correct answer for everyone. The ideal platform for you will be a direct reflection of your individual financial goals, your comfort with risk, your desired level of involvement, and the specific features that best support your investment strategy.

From the personalized guidance of full-service brokers to the cost-efficiency of online platforms and the hands-off simplicity of robo-advisors, the modern investment landscape offers a rich tapestry of choices. Niche options like micro-investing apps, ESG-focused platforms, and fractional shares further broaden the accessibility and customization available to investors today.

By diligently assessing your own needs and carefully evaluating potential platforms based on factors like fees, available products, user experience, support, and security, you can confidently select the investment home that will empower your financial growth. Remember that investing is a journey, not a destination, and the right platform can be a crucial partner in achieving your long-term financial aspirations. Start small, stay consistent, and continue learning—your future self will thank you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.