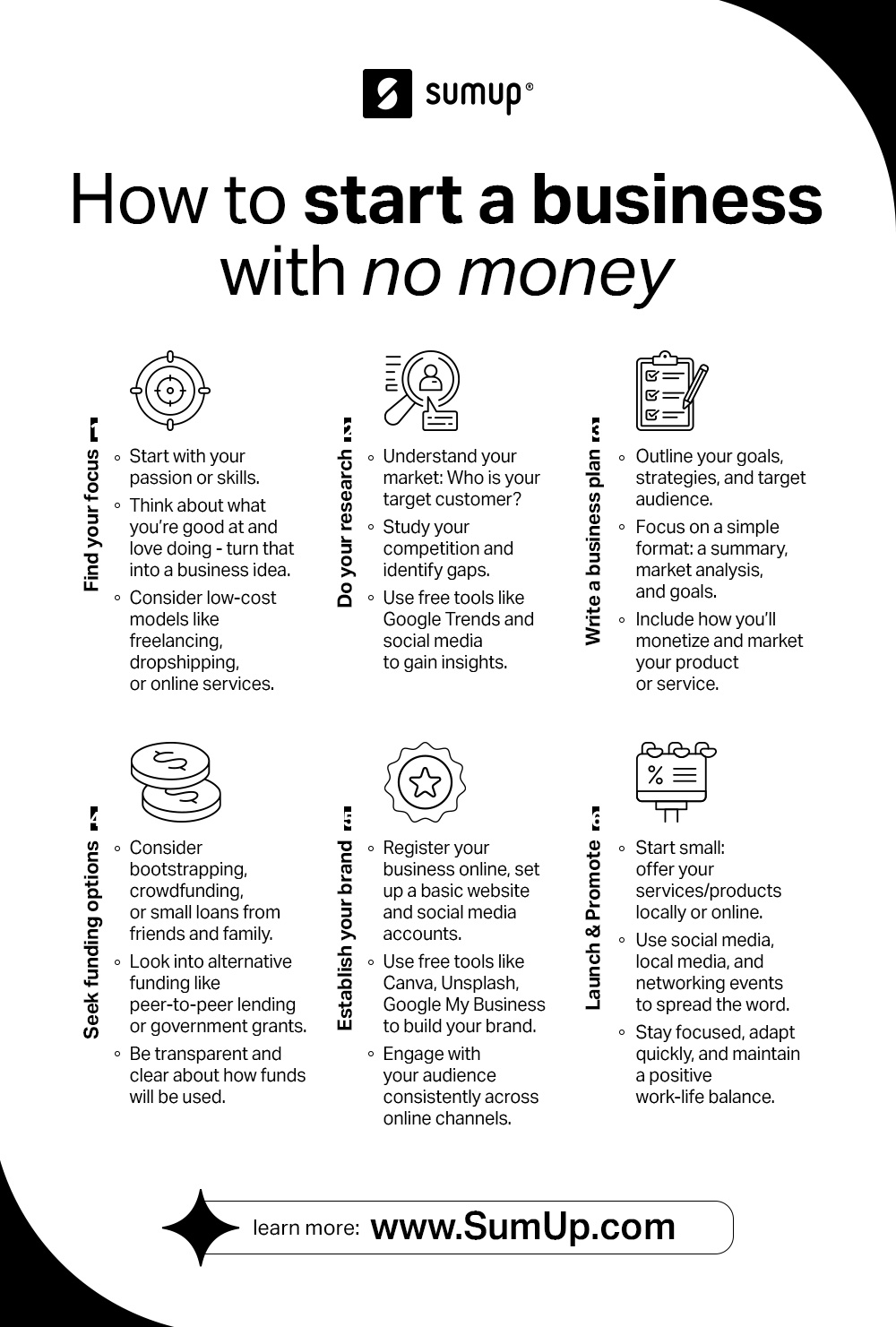

Starting a small business is a quintessential pursuit of the entrepreneurial spirit, a journey fueled by passion, innovation, and an unwavering vision. However, translating that vision into a tangible reality invariably requires one crucial ingredient: capital. For many aspiring entrepreneurs, securing the necessary funding is often the most significant hurdle. It’s a complex landscape with numerous pathways, each with its own advantages and prerequisites. This article delves into the diverse avenues available for acquiring the money needed to launch your small business, offering a comprehensive guide for navigating the financial maze with clarity and strategic foresight. We’ll explore everything from leveraging personal assets to attracting investors, ensuring you’re equipped with the knowledge to make informed financial decisions that pave the way for your venture’s success. Understanding these options is not just about finding money; it’s about finding the right money that aligns with your business model, growth projections, and long-term financial health.

Laying the Financial Foundation: Essential Preparations

Before you even begin approaching potential funders, a meticulous groundwork must be laid. The journey to securing capital isn’t a spontaneous sprint; it’s a well-planned marathon that begins with rigorous internal preparation. Lenders and investors alike demand a clear understanding of your business, its potential, and its financial viability. This foundational work not only enhances your credibility but also solidifies your own understanding of what it will truly take to get your business off the ground.

Developing a Robust Business Plan

A comprehensive business plan is arguably the most critical document for any aspiring entrepreneur seeking funding. It serves as your venture’s blueprint, articulating your vision, strategy, and operational details. More importantly, it’s a powerful communication tool that convinces potential investors and lenders of your business’s viability and your capacity to execute. This document should detail your executive summary, company description, market analysis (including target audience and competition), organization and management structure, service or product line, marketing and sales strategy, and crucially, your financial projections. A well-researched and professionally presented business plan demonstrates foresight, commitment, and a deep understanding of your industry, significantly increasing your chances of securing financial backing. It’s not merely a formality; it’s a living document that guides your decisions and showcases your potential returns.

Understanding Your Startup Costs and Financial Projections

Before you can ask for money, you must know precisely how much you need and what it will be used for. This requires a detailed breakdown of all anticipated startup costs. Think beyond the obvious; consider legal fees, permits, equipment, inventory, initial marketing, rent, utilities, insurance, website development, and even your own salary for the first few months. Categorize these into one-time expenses and recurring operational costs. Beyond initial outlays, you need to project your revenue, expenses, and cash flow for at least the first three to five years. These financial projections—including income statements, balance sheets, and cash flow statements—are crucial. They illustrate your anticipated profitability, demonstrate how you will repay loans, and provide investors with a clear picture of their potential return on investment. Accurate, realistic projections, backed by market research, are essential for building trust with funders.

Assessing Your Personal Financial Readiness

While your business plan focuses on the venture, your personal financial situation also plays a significant role in securing funding. Lenders often scrutinize an applicant’s personal credit score, as it’s a strong indicator of financial responsibility. A higher personal credit score (typically 680 or above) can open doors to better loan terms and more favorable interest rates. Furthermore, assessing your personal savings and assets helps determine how much personal capital you can contribute, which shows commitment and reduces the amount you need from external sources. Lenders and investors view personal investment as a strong positive signal, indicating that you have “skin in the game.” Understanding your personal financial standing, including any existing debts, allows you to present a holistic and responsible financial picture.

Tapping into Personal Resources and “Bootstrap” Funding

For many small businesses, especially those in their nascent stages, the most immediate and often least complicated source of funding comes from within or from one’s immediate network. This approach, often referred to as “bootstrapping,” emphasizes self-reliance and minimal external debt or equity dilution initially. It’s a testament to the entrepreneur’s ingenuity and commitment, and it can provide the crucial initial capital without the stringent requirements of traditional lenders or investors.

Self-Funding (Savings, Personal Loans)

The most direct route to funding your business is often through your own pockets. Utilizing personal savings, retirement funds (with careful consideration of tax implications, such as through a Rollover for Business Start-ups or “ROBS” plan), or even securing a personal loan can provide the initial capital needed to get started. Self-funding demonstrates immense confidence in your business idea and can be particularly attractive to future external investors, as it shows you are willing to invest your own capital. However, it’s crucial to separate personal and business finances from day one to maintain clear financial records and protect personal assets. While highly accessible, be mindful of overextending yourself and ensure you retain a personal emergency fund.

Friends and Family Investments

Your personal network can be a powerful source of startup capital. Friends and family, often referred to as “love money,” might be willing to invest in your venture, driven by personal trust and belief in your capabilities. This can come in the form of a loan, an equity investment, or even a gift. While often more flexible than traditional loans, it’s imperative to treat these arrangements professionally. Formalize everything with clear written agreements, detailing loan terms (interest rates, repayment schedule) or equity stakes, to prevent misunderstandings and protect personal relationships. Transparency and clear communication are key to ensuring these crucial relationships remain intact.

Crowdfunding Platforms

In recent years, crowdfunding has emerged as a democratic and powerful way to raise capital directly from a large number of individuals. Platforms like Kickstarter, Indiegogo (for rewards-based crowdfunding), and Republic (for equity-based crowdfunding) allow entrepreneurs to present their business idea to a global audience. Rewards-based crowdfunding involves offering products or unique experiences in exchange for financial pledges, ideal for product-focused businesses. Equity crowdfunding, on the other hand, allows you to sell small stakes of your company to a broad base of investors. Success in crowdfunding depends heavily on a compelling story, a well-produced pitch, and an active marketing campaign to attract backers. It’s not just about money; it’s also about validating your idea and building a community around your brand.

Exploring Traditional and Alternative Debt Financing Options

When personal resources aren’t enough, or if you prefer to retain full ownership of your company, debt financing becomes a primary consideration. This involves borrowing money that must be repaid, typically with interest, over a set period. The debt financing landscape is diverse, ranging from established financial institutions to specialized government-backed programs and community-focused lenders, each offering different structures and accessibility.

Small Business Loans from Banks and Credit Unions

Traditional banks and credit unions remain a cornerstone of small business financing. They offer a range of products, including term loans, lines of credit, and equipment financing. Banks typically prefer businesses with a proven track record, strong cash flow, collateral, and a solid business plan. They will scrutinize your personal credit score, business credit score (if applicable), and financial projections. While often offering competitive interest rates, the application process can be rigorous and time-consuming, and approval rates can be lower for very early-stage startups without significant collateral or operating history. Credit unions, being member-owned, sometimes offer more flexible terms or a more personalized approach, especially for local businesses.

SBA-Backed Loans: A Government Safety Net

The U.S. Small Business Administration (SBA) doesn’t lend money directly, but it guarantees a portion of loans made by approved lenders, reducing the risk for banks and making them more willing to lend to small businesses. SBA loans, such as the popular 7(a) loan program, offer attractive terms, lower down payments, and longer repayment periods. They are designed to support a wide range of business needs, from working capital to real estate purchases. While the application process is still thorough, an SBA guarantee can be a game-changer for startups or businesses that don’t meet traditional bank lending criteria. It’s important to find an SBA-approved lender, as the application itself goes through the financial institution, not directly to the SBA.

Microloans and Community Development Financial Institutions (CDFIs)

For businesses needing smaller loan amounts, typically under $50,000, microloans offer a vital lifeline. These are often provided by non-profit organizations or Community Development Financial Institutions (CDFIs) that focus on supporting underserved communities and entrepreneurs who may not qualify for traditional bank loans. CDFIs are dedicated to community development and often provide not just capital but also technical assistance and business mentorship. They evaluate loan applications based on a broader set of criteria than traditional banks, often focusing on the business’s potential for job creation and community impact. Microloans are an excellent option for sole proprietors, home-based businesses, or those with limited operating history.

Business Credit Cards: A Double-Edged Sword

Business credit cards can provide quick access to capital for small, immediate expenses or for managing short-term cash flow gaps. They offer flexibility and can help build your business credit history when managed responsibly. Many come with rewards programs that can benefit your business. However, business credit cards typically carry higher interest rates than traditional loans, making them an expensive option if balances are carried over month-to-month. They should be used strategically for working capital, not for funding major startup costs. Mismanagement can quickly lead to accumulating debt and damaging both personal and business credit scores.

Attracting Equity Investors and Grant Funding

For businesses with high growth potential, particularly those in scalable industries or with innovative products, equity financing or non-dilutive grants can provide substantial capital. These sources often come with mentorship and strategic support, but they also require a different approach and a higher level of scrutiny regarding your business’s future prospects.

Angel Investors and Venture Capital

Equity financing involves giving up a portion of your company’s ownership in exchange for capital. Angel investors are high-net-worth individuals who invest their personal funds, often in early-stage startups, and frequently provide mentorship alongside their investment. Venture capital (VC) firms, on the other hand, manage funds from institutional investors and typically invest larger sums in businesses with significant growth potential, often requiring a clear exit strategy (e.g., acquisition or IPO). Both angels and VCs are looking for scalable businesses with strong management teams, innovative solutions, and a large addressable market. The process of attracting equity investors is highly competitive, requiring a compelling pitch, detailed financial projections, and a clear articulation of your vision for exponential growth.

Government Grants and Business Competitions

Unlike loans or equity investments, grants are non-repayable funds typically awarded by government agencies, foundations, or corporations to support specific initiatives or industries. While less common for general startup costs, grants are available for businesses involved in research and development (e.g., SBIR/STTR programs in the U.S.), environmental sustainability, social impact, or those operating in specific distressed regions. The application process for grants is highly competitive and often requires extensive paperwork, demonstrating how your business aligns with the grantor’s mission. Similarly, winning business plan competitions can provide not only prize money but also invaluable exposure, mentorship, and validation for your concept. These funds are non-dilutive, meaning you retain full ownership.

Incubators and Accelerators

Business incubators and accelerators are programs designed to support early-stage companies by providing resources such as office space, mentorship, networking opportunities, and often, seed funding. Incubators typically offer longer-term support for businesses in their nascent stages, while accelerators offer intensive, time-limited programs designed to rapidly scale companies. In exchange for their services and sometimes a small investment, accelerators often take a small equity stake in the participating businesses. These programs are highly selective but can provide a tremendous boost in funding, strategic guidance, and connections that are crucial for growth and attracting further investment. They are particularly valuable for technology or high-growth startups.

Strategic Financial Management Beyond Initial Funding

Securing initial funding is a monumental achievement, but it’s merely the first step. The true test of an entrepreneur lies in how effectively they manage that capital and sustain the business’s financial health moving forward. Strategic financial management ensures longevity, fosters growth, and positions the business for future investment rounds or self-sufficiency.

Managing Cash Flow Effectively

Cash flow is the lifeblood of any small business. It’s not just about having money; it’s about having money when you need it. Effective cash flow management involves monitoring the money coming into and going out of your business, anticipating shortages, and planning for periods of lower revenue or higher expenses. This includes diligent invoicing and collections, managing accounts payable to optimize payment terms, maintaining adequate cash reserves, and accurately forecasting future cash needs. Poor cash flow is a leading cause of small business failure, even for profitable companies. Implementing robust accounting software and regularly reviewing financial statements are crucial practices.

Reinvesting Profits for Growth

Once your business starts generating profits, a critical decision is how to utilize them. While some profits might be distributed to owners or investors, strategically reinvesting a portion back into the business is a powerful way to fuel sustainable growth. This could involve expanding operations, investing in new equipment, developing new products or services, increasing marketing efforts, hiring key talent, or improving infrastructure. Reinvesting profits reduces reliance on external financing for growth, demonstrates financial discipline, and compounds returns over time, enhancing the overall value of your business. It’s a testament to a long-term vision and a commitment to scaling without accumulating excessive debt.

Building and Maintaining Good Financial Relationships

Your relationship with lenders, investors, and even vendors is an ongoing asset. Consistently meeting loan repayment obligations, providing transparent financial updates to investors, and paying vendors on time builds a strong reputation and credit history for your business. This positive track record is invaluable when seeking future financing, negotiating better terms, or expanding credit lines. Maintain open communication with your financial partners, proactively addressing any challenges and demonstrating your commitment to financial responsibility. A strong financial network, built on trust and reliability, can provide a safety net and open doors to opportunities as your business evolves and grows.

The journey to funding a small business is multifaceted, requiring careful planning, persistent effort, and a thorough understanding of the available options. By diligently preparing your business plan, exploring a diverse range of funding sources, and committing to sound financial management, you can transform your entrepreneurial dream into a thriving reality. Remember, securing capital is not just about getting money; it’s about making strategic choices that align with your vision and pave the way for long-term success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.