The landscape of personal finance is perpetually shifting, but few sectors have experienced as much volatility in recent years as the automotive market. For many consumers, the question “what are car interest rates right now?” is not just a matter of curiosity—it is a critical calculation that determines monthly budgets, long-term debt loads, and the feasibility of reliable transportation. As we move through the current economic cycle, characterized by the Federal Reserve’s efforts to curb inflation and a stabilizing but still expensive car market, understanding the nuances of Annual Percentage Rates (APR) is essential for any savvy borrower.

Navigating car interest rates requires more than a glance at a single number. It involves understanding credit tiers, the distinction between new and used vehicle financing, and the macroeconomic forces that dictate how much it costs to borrow money. This guide provides an in-depth analysis of the current state of car interest rates and the financial strategies you need to secure the best possible deal.

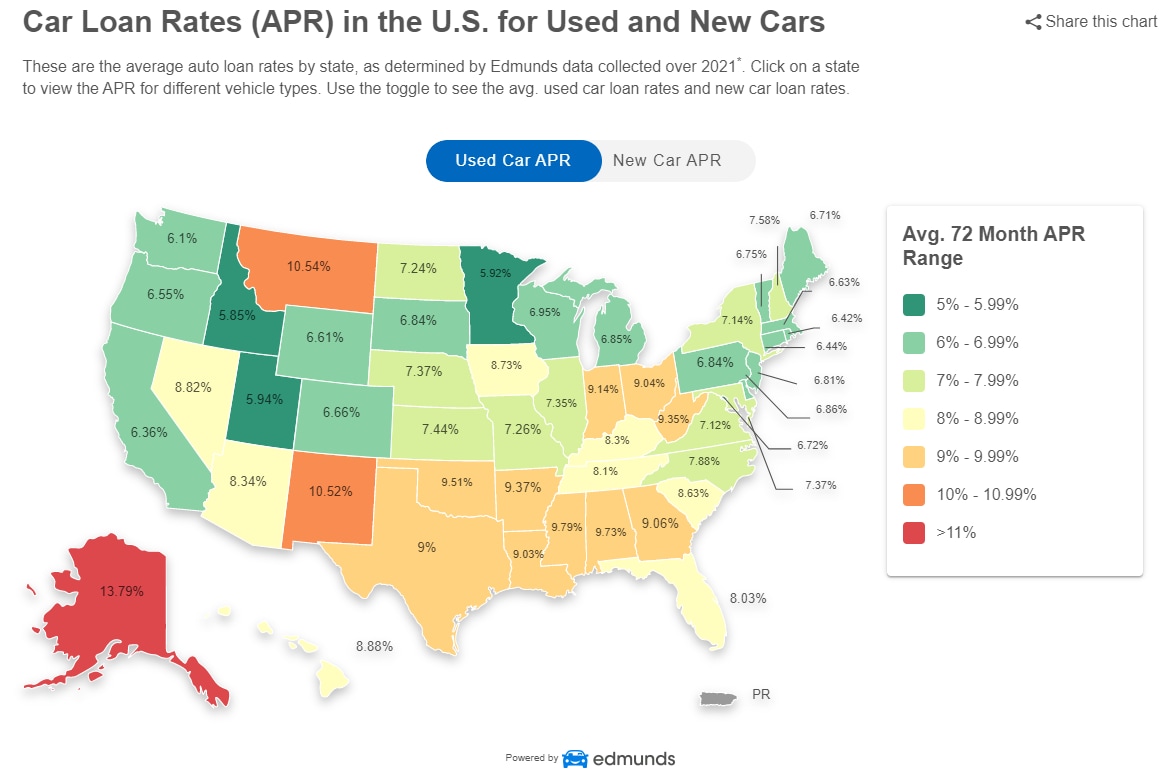

Understanding the Current Average Car Interest Rates

To answer what car interest rates are “right now,” one must look at the averages across the broad spectrum of the American economy. As of the current quarter, interest rates remain at historical highs compared to the previous decade. While the days of 0% or 1.9% APR were common during the mid-2010s, the current baseline for a borrower with excellent credit typically starts around 6.5% to 7.5% for new vehicles.

The Divergence Between New and Used Car Rates

There is a consistent “spread” between new and used car interest rates. Historically, used car loans carry higher interest rates because used vehicles represent a higher risk to the lender. Used cars have more volatile resale values and a higher likelihood of mechanical failure, which could lead to a borrower defaulting on the loan. Currently, while a new car loan might average 7% for a prime borrower, a used car loan for that same borrower could easily hover between 10% and 12%. For those in the subprime category, used car rates can frequently climb into the high teens or even surpass 20%.

How Credit Scores Dictate Your Specific Rate

In the world of personal finance, your credit score is the primary lever that determines your interest rate. Lenders generally categorize borrowers into five tiers: Superprime (781–850), Prime (661–780), Nonprime (601–660), Subprime (501–600), and Deep Subprime (300–500).

Right now, Superprime borrowers are seeing the best available rates, often dipping slightly below the national average if they utilize manufacturer-sponsored “captive” financing. Conversely, the “Subprime” gap has widened. Because lenders are tightening their belts in a high-interest environment, individuals with lower scores are being hit with “risk premiums,” making the cost of borrowing significantly higher than it was just twenty-four months ago.

Factors Influencing Today’s Auto Loan Market

Car interest rates do not exist in a vacuum. They are a reflection of broader fiscal policies and market conditions. Understanding why rates are where they are can help you time your purchase or decide whether to wait for a potential pivot in the market.

Federal Reserve Policy and Inflation

The single biggest driver of car interest rates is the Federal Reserve’s federal funds rate. When the Fed raises rates to combat inflation, the cost for banks to borrow money increases. To maintain their profit margins, banks pass these costs onto consumers in the form of higher APRs on mortgages, credit cards, and auto loans. Even if the Fed pauses rate hikes, the “higher for longer” sentiment in the bond market keeps auto loan yields elevated. Until inflation consistently hits the Fed’s 2% target, significant downward pressure on car interest rates is unlikely.

Lender Competition and Risk Assessment

While the Fed sets the floor, commercial banks and credit unions set the ceiling based on their appetite for risk. Currently, many regional banks have become more conservative with their lending portfolios. They are looking for higher debt-to-income (DTI) ratios and more substantial “skin in the game” (down payments) from borrowers. This cautious approach by lenders naturally pushes rates upward, as they are only willing to lend at a premium that justifies the risk of a potential economic downturn.

Inventory Levels and Dealership Incentives

For the first time since the 2020 supply chain disruptions, vehicle inventory is beginning to normalize. This is good news for the consumer’s wallet. When lots are full, manufacturers (like Ford, Toyota, or GM) offer “subsidized” interest rates to move units. Even if the market rate is 8%, a manufacturer might offer a promotional 3.9% APR for 48 months on specific models. Monitoring these “incentive spends” is currently the most effective way for a buyer to circumvent the high national average interest rates.

Strategies to Secure the Best Rate Right Now

In a high-rate environment, you cannot afford to be a passive consumer. You must treat the financing of the car with as much scrutiny as the price of the car itself. Employing specific financial tactics can save you thousands of dollars over the life of the loan.

Pre-approval vs. Dealership Financing

One of the most common mistakes buyers make is walking into a dealership without a financing offer already in hand. Right now, it is vital to secure a pre-approval from an outside source, such as a credit union or an online bank. This gives you a “benchmark” rate. When you enter the dealership’s finance office, you can present your pre-approval. If the dealer wants your business, they are often incentivized to beat that rate by a fraction of a percent. Without a pre-approval, the dealer has no competition and may “mark up” the interest rate to increase their own profit margin.

The Power of a Substantial Down Payment

With interest rates hovering near 8-10%, the “cost of carry” on a loan is expensive. In the era of low interest, it made sense to put as little money down as possible and invest the rest. Today, the math has flipped. A larger down payment reduces the principal balance, which directly reduces the total interest paid over time. Furthermore, a down payment that covers at least 20% of the vehicle’s value lowers the lender’s “Loan-to-Value” (LTV) ratio, which can often trigger a lower interest rate tier because the loan is seen as less risky.

Shortening the Loan Term

The trend of 72-month and 84-month auto loans is a dangerous path in a high-interest environment. While longer terms lower the monthly payment, they exponentially increase the total interest paid and keep the borrower “upside down” (owing more than the car is worth) for years. By opting for a 48-month or 60-month term, you not only pay off the debt faster, but you also usually qualify for a lower APR. Lenders reward shorter-term commitments with better rates because their capital is at risk for a shorter period.

Comparing Financing Options: Banks, Credit Unions, and Online Lenders

Where you get your money is just as important as how much you get. Different financial institutions have different structures that influence the rates they offer.

Why Credit Unions Often Win

For the average consumer looking for the lowest car interest rates right now, credit unions are often the gold standard. Because they are member-owned, non-profit entities, they return their “profits” to members in the form of lower loan rates and higher savings yields. On average, credit union auto loan rates can be 1% to 2% lower than those of big national banks. They also tend to have more flexible underwriting criteria for those who may have a slightly less-than-perfect credit history.

The Rise of Digital Lending Platforms

Fintech has revolutionized auto financing. Online lenders and digital platforms allow you to compare rates from dozens of sources simultaneously without a “hard” pull on your credit report (until the final application). These platforms are highly efficient and have lower overhead than brick-and-mortar banks, allowing them to offer competitive rates. However, it is essential to read the fine print regarding “origination fees” or other hidden costs that might offset the lower APR.

The Long-term Financial Impact of Your Interest Rate

It is easy to get caught up in the monthly payment, but the true cost of a car is the “Total Cost of Ownership.” The interest rate is a massive component of this.

The Cost of Waiting vs. Buying Now

Many potential buyers are asking: “Should I wait for rates to drop?” This is a complex financial gamble. If you wait six months for a 1% drop in interest rates, but the price of the vehicle increases by $2,000 due to inflation or demand, you haven’t actually saved money. The best strategy is to buy based on necessity and your current ability to afford the payment. If rates do drop significantly in the future, you can always look into the “Money” move of refinancing.

Refinancing Opportunities Down the Road

An auto loan is not a life sentence. If you are forced to take a high interest rate today because of market conditions or a temporary dip in your credit score, you should plan for a refinance. Once you have made twelve months of on-time payments and if the broader market rates have cooled, you can apply for a refinance loan. This allows you to replace your high-interest debt with a more affordable option, effectively “re-negotiating” your purchase long after you’ve driven off the lot.

In conclusion, while car interest rates are currently higher than many are used to, they remain manageable for those who approach the market with a disciplined, informed financial strategy. By monitoring the Fed, boosting your credit score, and shopping across different lender types, you can navigate the “Money” side of car buying with confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.