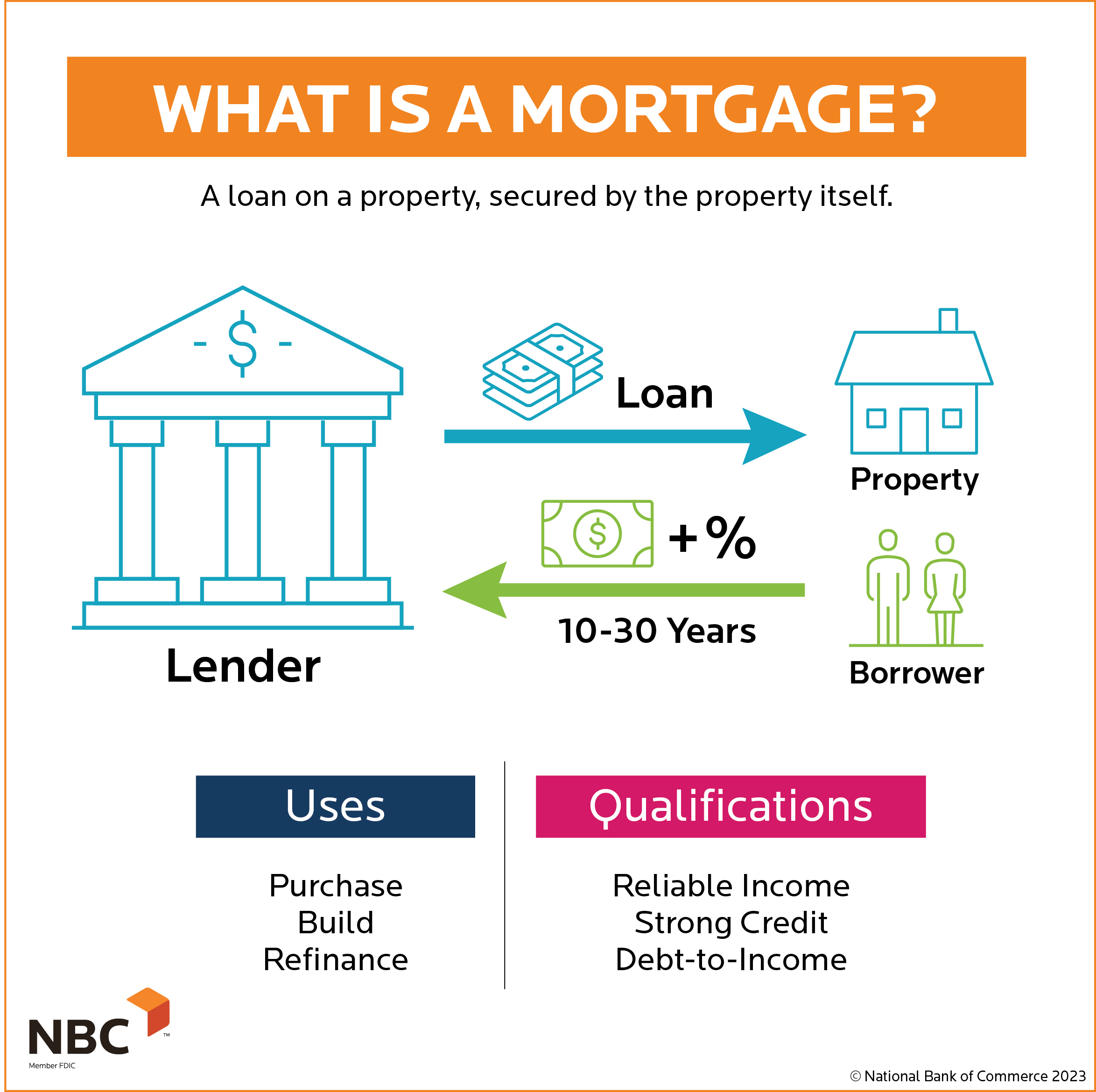

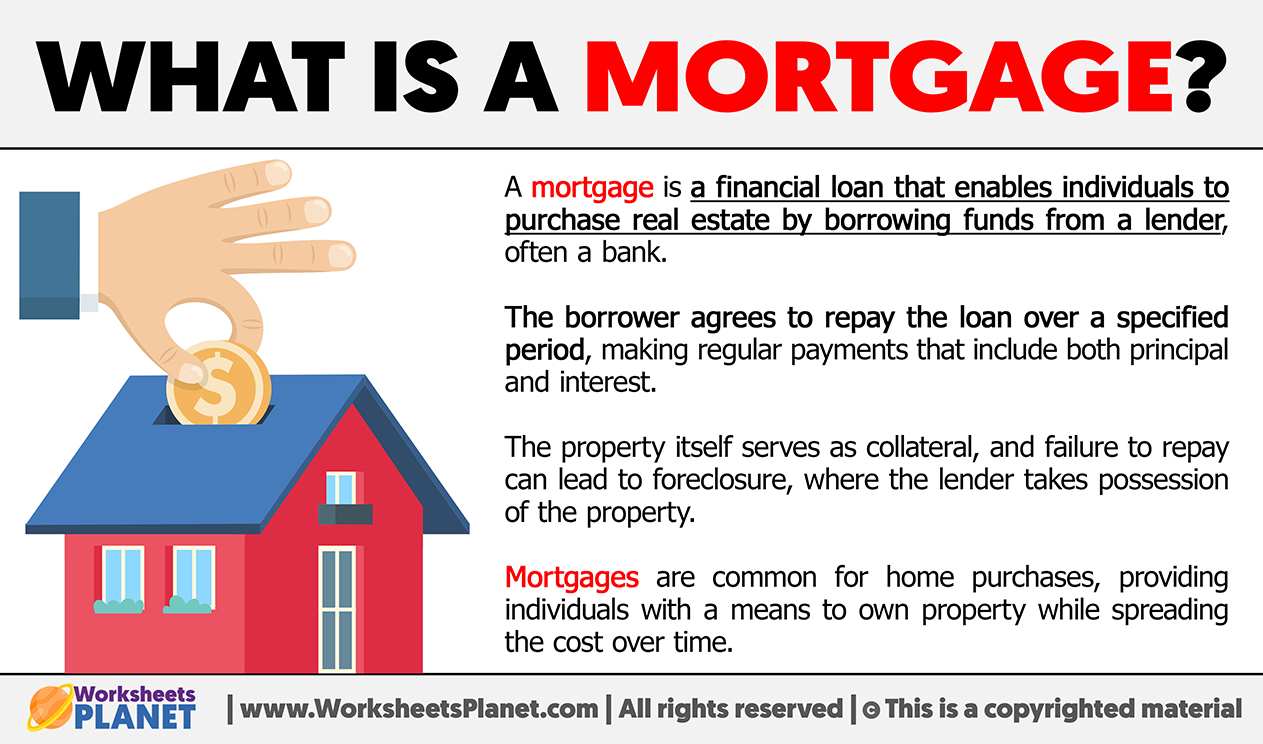

For most individuals, a home is the most significant purchase they will ever make. Because very few people have the liquid capital to buy a property outright, the global real estate market relies heavily on the concept of the mortgage. At its simplest, a mortgage is a type of loan used to purchase or maintain real estate. However, from a financial perspective, it is a sophisticated debt instrument that serves as a cornerstone of personal finance and long-term wealth building.

Understanding the nuances of mortgages is essential for anyone looking to navigate the complexities of the modern financial landscape. A mortgage is not merely a monthly payment; it is a long-term legal agreement where the property itself serves as collateral. This guide explores the mechanics, variations, and strategic implications of mortgages within the broader context of personal finance.

The Fundamental Mechanics of a Mortgage

To master your personal finances, you must first understand the structural components of a mortgage. While a mortgage functions like other loans in that you borrow money and pay it back with interest, its long duration—often spanning 15 to 30 years—and its secured nature make it unique.

Principal and Interest: The Core Components

Every mortgage payment is primarily split into two parts: principal and interest. The principal is the actual amount of money you borrowed from the lender to purchase the home. The interest is the cost of borrowing that money, expressed as a percentage. In the early years of a mortgage, a larger portion of your monthly payment goes toward interest. As the loan balance decreases over time, a greater percentage of your payment is applied to the principal. This shift is a critical concept in wealth accumulation, as it dictates how quickly you build equity in your home.

Down Payments and Loan-to-Value (LTV) Ratios

The down payment is the upfront cash payment you make toward the purchase price of the home. In the world of finance, the size of your down payment determines your Loan-to-Value (LTV) ratio. For example, if you buy a $500,000 home and provide a $100,000 down payment, your loan amount is $400,000, resulting in an LTV of 80%. Lenders use this ratio to assess risk; a lower LTV usually results in better interest rates and may exempt the borrower from paying Private Mortgage Insurance (PMI), a cost intended to protect the lender in case of default.

The Role of Escrow: Taxes and Insurance

A mortgage payment often includes more than just the loan repayment. Many lenders require an escrow account, which acts as a holding pen for funds related to property taxes and homeowners insurance. Each month, a portion of your payment is set aside in this account, and the lender pays the tax and insurance bills on your behalf when they fall due. This ensures that the asset (the home) remains protected and that the government’s tax liens do not take precedence over the lender’s interest.

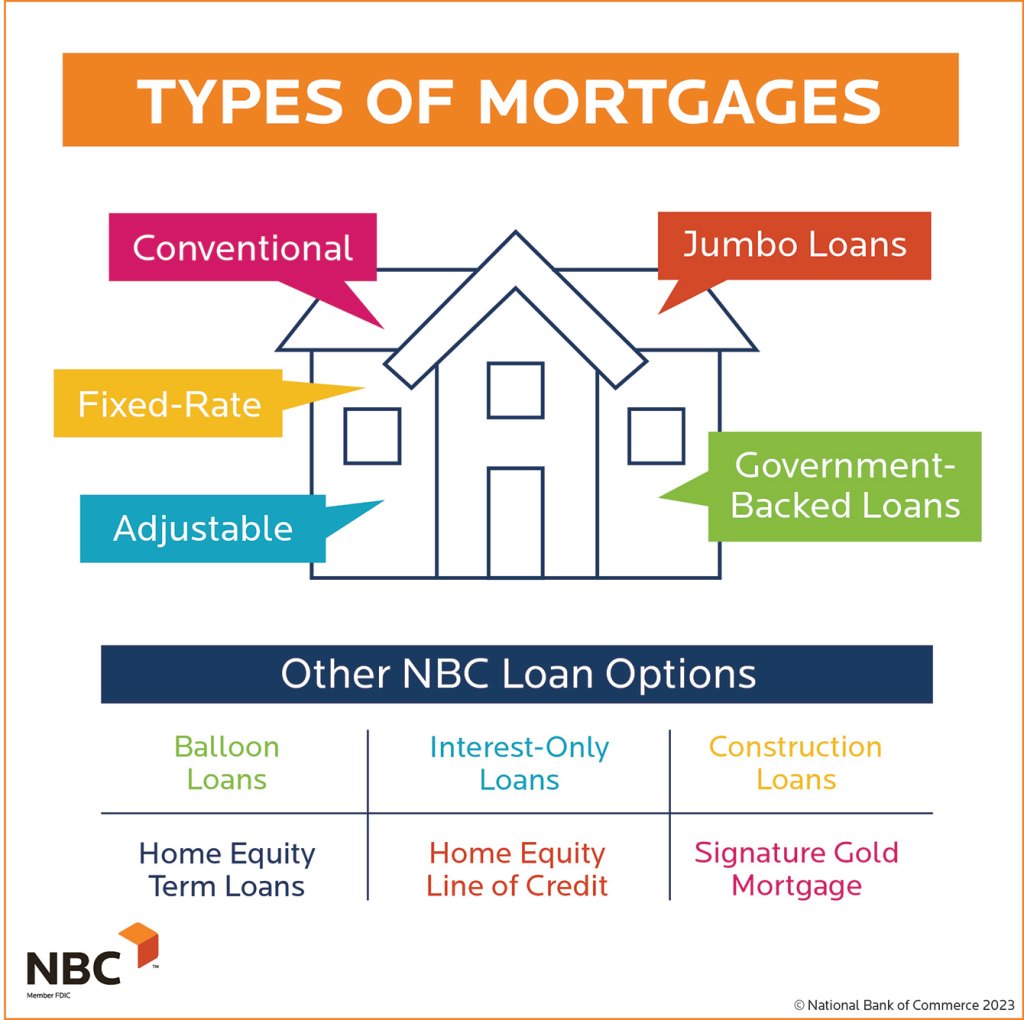

Exploring Different Types of Mortgage Products

Financial institutions offer a variety of mortgage products tailored to different financial situations, risk tolerances, and long-term goals. Choosing the right product can save a borrower tens of thousands of dollars over the life of the loan.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The most common choice for homebuyers is the fixed-rate mortgage. With this product, the interest rate remains the same for the entire life of the loan, providing the borrower with a predictable monthly payment. In contrast, an Adjustable-Rate Mortgage (ARM) offers an initial period of lower, fixed interest (often 5, 7, or 10 years), after which the rate adjusts periodically based on market indices. While ARMs can be riskier if interest rates rise, they can be a strategic choice for individuals who plan to sell the home or refinance before the introductory period ends.

Government-Backed Loans (FHA, VA, and USDA)

To encourage homeownership, various government agencies insure or guarantee loans, making them more accessible to specific demographics. Federal Housing Administration (FHA) loans are popular among first-time buyers due to lower credit score requirements and down payments as low as 3.5%. VA loans, provided by the Department of Veterans Affairs, offer competitive rates and often require no down payment for active-duty service members and veterans. USDA loans target rural homebuyers, offering 100% financing for eligible properties.

Conventional and Jumbo Loans

Conventional loans are not insured by the federal government and typically adhere to the lending guidelines set by Fannie Mae or Freddie Mac. For properties that exceed local “conforming loan limits,” borrowers must seek Jumbo loans. Because Jumbo loans represent a higher risk for the lender due to the large dollar amount and the lack of a government guarantee, they often require higher credit scores, lower debt-to-income ratios, and larger down payments.

The Financial Impact of Interest Rates and Amortization

In the niche of money and investing, the “cost” of a mortgage is defined by more than just the purchase price of the house. The intersection of interest rates and the amortization schedule dictates the true economic cost of the debt.

How Amortization Schedules Work

Amortization is the process of paying off a debt over time through regular installments. A mortgage amortization schedule provides a detailed look at every payment over the life of the loan. Because interest is calculated based on the remaining principal balance, the “cost” of the loan is front-loaded. Understanding your amortization schedule is vital for those considering making extra principal payments, as reducing the principal early in the loan term can exponentially reduce the total interest paid over 30 years.

The Difference Between Interest Rate and APR

When shopping for a mortgage, borrowers often see two different percentages: the interest rate and the Annual Percentage Rate (APR). The interest rate is the cost you pay each year to borrow the money. The APR is a more comprehensive figure, as it includes the interest rate plus other costs such as broker fees, points, and some closing costs. For a savvy investor, the APR is the more accurate tool for comparing the total cost of loans between different lenders.

Strategies for Reducing Lifetime Interest Costs

One of the most effective ways to manage a mortgage as a financial tool is to look for ways to minimize interest. This can be achieved through “points”—prepaying interest at closing to secure a lower monthly rate—or by opting for a 15-year term instead of a 30-year term. While a 15-year mortgage has higher monthly payments, the interest rates are typically lower, and the total interest paid over the life of the loan is drastically reduced, often by half or more.

Navigating the Mortgage Application and Approval Process

Securing a mortgage is a rigorous process that requires a deep dive into an individual’s financial health. Lenders look at several key metrics to determine “creditworthiness.”

Credit Scores and Debt-to-Income (DTI) Ratios

A borrower’s credit score is the primary indicator of their reliability in repaying debt. Higher scores unlock lower interest rates, which can save a homeowner hundreds of dollars a month. Equally important is the Debt-to-Income (DTI) ratio. Lenders calculate this by dividing total monthly debt obligations by gross monthly income. Generally, lenders prefer a DTI of 43% or lower. Keeping other debts—such as car loans or credit card balances—low is essential for maximizing one’s mortgage borrowing power.

Pre-approval vs. Pre-qualification

In a competitive real estate market, a pre-approval letter is a necessity. While a pre-qualification is a simple estimate based on self-reported data, a pre-approval involves a lender verifying your income, assets, and credit history. Being pre-approved tells sellers that you are a serious buyer with the financial backing to close the deal, which is a crucial strategic advantage in the home-buying process.

Closing Costs and Finalizing the Loan

The final stage of obtaining a mortgage is the “closing.” Borrowers must be prepared for closing costs, which typically range from 2% to 5% of the purchase price. these include appraisal fees, title insurance, attorney fees, and recording taxes. Understanding these costs is essential for proper budgeting, as they must usually be paid in cash at the time of the transaction.

Managing Your Mortgage as a Financial Asset

Once a mortgage is secured, it should not be viewed as a static debt but as a dynamic part of a financial portfolio. Homeownership is a primary vehicle for building net worth through equity.

Refinancing Opportunities and Risks

Refinancing involves replacing an existing mortgage with a new one, typically to take advantage of lower interest rates or to change the loan term. For a homeowner, a “rate-and-term” refinance can lower monthly payments or shorten the loan duration. Alternatively, a “cash-out” refinance allows the homeowner to tap into their built-up equity to fund home improvements, consolidate high-interest debt, or invest in other assets. However, refinancing comes with its own closing costs, so a break-even analysis is required to ensure the move makes financial sense.

Building Home Equity Over Time

Equity is the difference between the market value of the home and the remaining mortgage balance. It grows in two ways: as the borrower pays down the principal and as the property appreciates in value. Equity is a powerful financial tool; it can be used as collateral for a Home Equity Line of Credit (HELOC) or realized as a significant capital gain when the property is sold. By viewing a mortgage through the lens of equity management, a homeowner can transform a simple monthly expense into a long-term wealth-building strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.