In the world of personal finance, the term “interest rate” is ubiquitous, yet its definition of “good” is notoriously fluid. Whether you are looking to purchase a first home, finance a vehicle, or grow your emergency fund in a high-yield savings account, the interest rate acts as the primary lever of your financial momentum. At its core, an interest rate is the price of money—the cost to borrow it or the reward for lending it.

However, determining what constitutes a “good” rate is not as simple as looking at a single number. It is a moving target influenced by global economic shifts, central bank policies, and your individual financial health. To navigate the complexities of the modern financial landscape, one must understand the mechanics behind these percentages and how to position themselves to secure the most favorable terms possible.

Understanding the Fundamentals: What Determines an Interest Rate?

Interest rates do not exist in a vacuum. They are the result of a complex interplay between macroeconomic forces and microeconomic realities. Before you can judge a rate offered by a bank, you must understand the “why” behind the number.

The Role of the Federal Reserve and Central Banks

In the United States, the Federal Reserve (the Fed) sets the “federal funds rate,” which is the interest rate at which commercial banks borrow and lend to each other overnight. While the Fed does not directly set the rates for mortgages or credit cards, its decisions create a ripple effect. When the Fed raises rates to combat inflation, the cost of borrowing increases for everyone. Conversely, when the Fed lowers rates to stimulate a sluggish economy, borrowing becomes cheaper. A “good” rate in a high-inflation environment might be 7%, whereas in a stagnant economy, that same 7% would be considered exorbitant.

Inflation and Economic Growth

Inflation is the silent architect of interest rates. Lenders must charge enough interest to ensure that the money they are paid back in the future has more purchasing power than the money they lent out today. If inflation is running at 4%, a 3% interest rate actually represents a loss for the lender in terms of “real” value. Therefore, during periods of high inflation, interest rates naturally climb. A good interest rate is often defined as one that stays as close to the rate of inflation as possible for borrowers, or significantly exceeds it for savers.

Your Credit Profile as a Risk Assessment

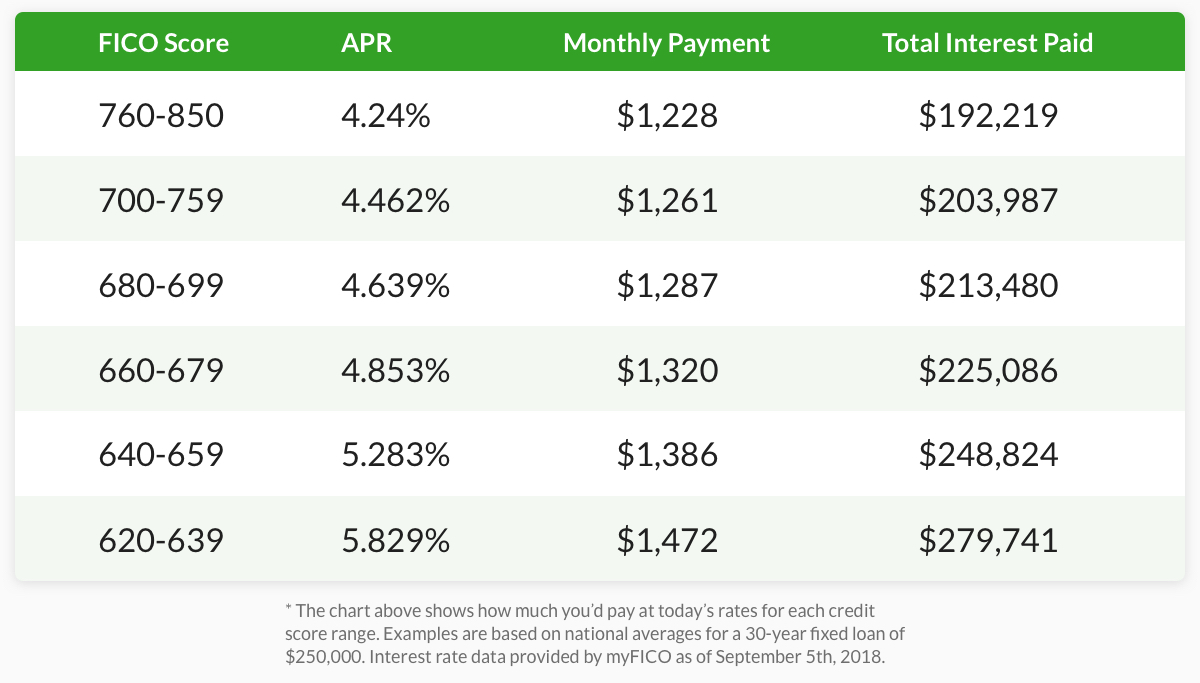

On a personal level, the interest rate you are offered is a reflection of your perceived risk. Banks use your credit score, debt-to-income (DTI) ratio, and employment history to determine the likelihood that you will repay the loan. A borrower with a credit score of 800 is seen as a “sure bet” and will be offered the “prime rate”—the lowest rate available. A borrower with a score of 600 represents a higher risk, and the bank will compensate for that risk by charging a higher interest rate. In this context, a “good” rate is relative to your credit tier.

Benchmarking “Good” Rates Across Different Financial Products

Because different loans carry different levels of risk and duration, a good rate for one product might be a terrible rate for another. Here is a breakdown of what to look for in the current market.

Mortgage Rates: The Cost of Homeownership

Mortgages are generally the largest financial commitment an individual will make. Because these loans are secured by the property itself and typically span 15 to 30 years, their rates are lower than unsecured debt but higher than the “risk-free” rate of government bonds.

Historically, mortgage rates have fluctuated wildly—from highs of 18% in the early 1980s to lows of 2.5% in 2020. In a stabilized market, a “good” mortgage rate is generally anything within one percentage point of the current national average for your specific credit score. For most borrowers, aiming for a rate that keeps the total interest paid over the life of the loan manageable is the ultimate goal.

Auto Loans: New vs. Used

Auto loans are shorter in duration, typically ranging from 36 to 72 months. A good interest rate on a new car is often lower than on a used car because new cars have a higher resale value and are easier for the bank to recoup costs on if they have to repossess the vehicle. Manufacturers also frequently offer “incentive rates” (sometimes as low as 0% or 1.9%) to move inventory. If you are financing through a traditional bank, a good rate is typically anything below the 5-6% mark, though this fluctuates based on the broader economy.

Personal Loans and Credit Cards

These are often “unsecured” debts, meaning there is no collateral like a house or a car for the bank to seize if you stop paying. Consequently, the interest rates are much higher. For a personal loan, a good rate might range from 7% to 12% for those with excellent credit. Credit cards, however, are a different animal. The national average credit card APR often hovers around 20%. In this category, a “good” rate is essentially the lowest one you can find—or better yet, a card with a 0% introductory APR period that allows you to pay off debt interest-free for 12 to 18 months.

The Flip Side: Seeking Good Interest Rates for Your Savings

While high interest rates are a burden for borrowers, they are a boon for savers. If you have cash sitting in a traditional big-box bank, you are likely earning a pittance—often as low as 0.01% APR. In a “good” interest rate environment for savers, your money should be working much harder for you.

High-Yield Savings Accounts (HYSA)

A “good” interest rate for a savings account is one that competes with the top tier of online banks. High-yield savings accounts often offer rates that are 10 to 20 times higher than traditional brick-and-mortar savings accounts. If the federal funds rate is high, a good HYSA rate should be between 4% and 5%. The goal of a good savings rate is to maintain the liquidity of your cash while ensuring its value isn’t eroded by inflation.

Certificates of Deposit (CDs) and Treasury Bills

For money that you don’t need immediate access to, CDs and Treasury bills often offer even higher rates. A good rate for a 12-month CD is typically slightly higher than the best available HYSA rate. This “liquidity premium” rewards you for locking your money away for a set period. In a high-rate environment, locking in a 5% or 5.5% CD can be a brilliant move if you anticipate that rates will drop in the near future.

Tactical Steps to Secure the Best Possible Rate

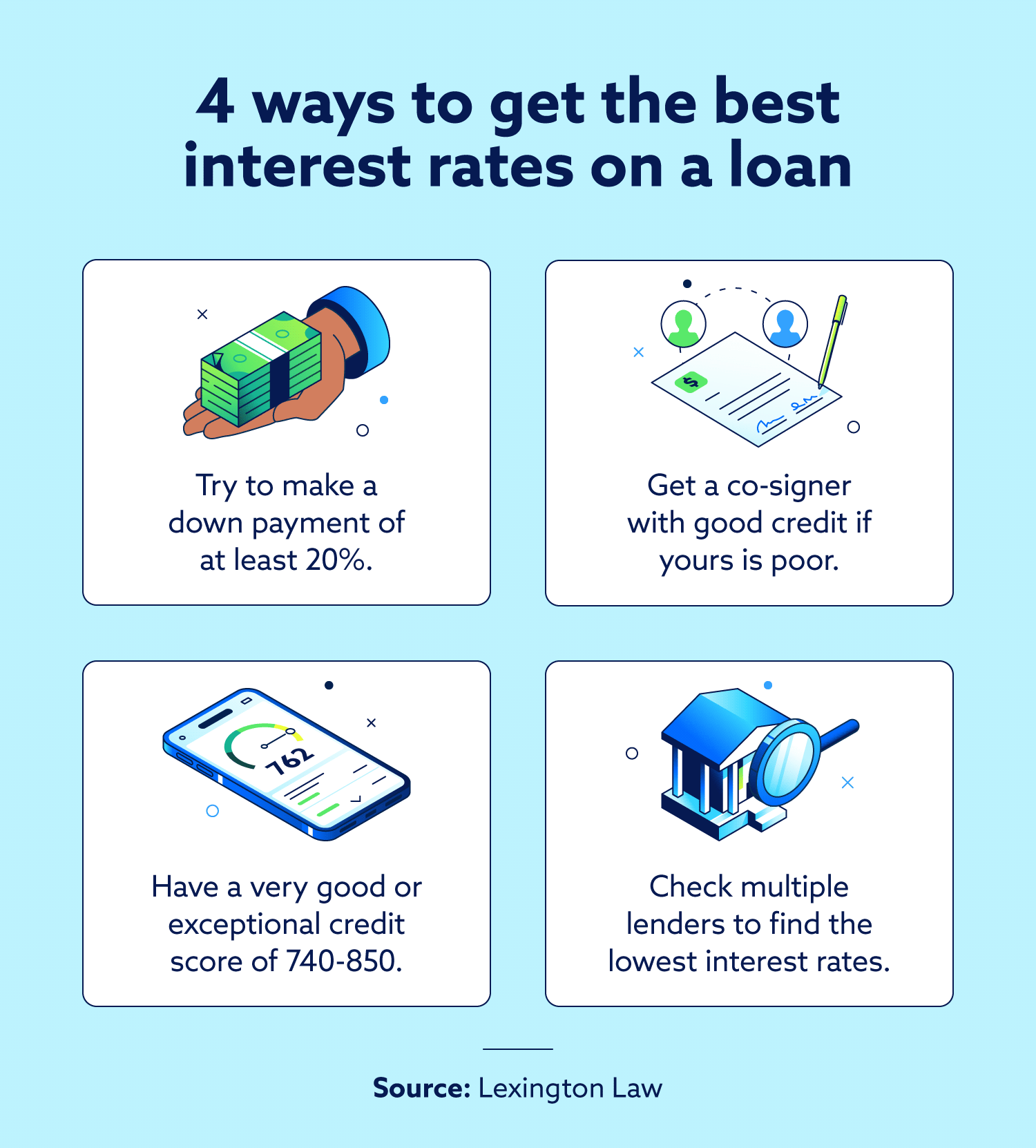

Securing a good interest rate is not just about timing the market; it’s about preparation. You have more control over the rate you receive than you might think.

Improving Your Credit Score

The difference between a “fair” credit score and an “excellent” one can translate into tens of thousands of dollars in interest over the life of a mortgage. To secure the best rates, focus on the “Big Three” of credit health:

- Payment History: Never miss a due date.

- Credit Utilization: Keep your credit card balances below 30% of your total limit.

- Credit Mix: Having a healthy variety of installment loans and revolving credit.

The Importance of Shopping Around

Many consumers take the first rate offered by their primary bank, which is often a mistake. A “good” rate is only verified when compared against the competition. When shopping for a mortgage or an auto loan, you should obtain at least three different quotes. Because credit reporting agencies recognize “rate shopping,” multiple inquiries for the same type of loan within a short window (usually 14–45 days) are typically treated as a single inquiry, protecting your credit score while you hunt for the best deal.

Understanding Fixed vs. Variable Rates

A rate that looks “good” today might not be good tomorrow.

- Fixed Rates stay the same for the life of the loan, providing certainty. They are ideal when rates are historically low.

- Variable (or Adjustable) Rates fluctuate based on an index. These often start lower than fixed rates—making them look “good” initially—but they carry the risk of increasing significantly over time. A good rate is one that fits your risk tolerance and your timeline for holding the debt.

Conclusion: Navigating the Changing Financial Landscape

Ultimately, a “good” interest rate is a subjective figure defined by the intersection of the current economic climate and your personal financial standing. In a high-rate environment, a good rate is one that beats the national average through meticulous credit management and aggressive shopping. In a low-rate environment, a good rate is one that you “lock in” to protect your future self from inevitable market shifts.

Whether you are a borrower looking to minimize costs or a saver looking to maximize returns, the strategy remains the same: stay informed, maintain a high credit standard, and always look beyond the first offer. By understanding the mechanics of interest, you transform from a passive participant in the economy into a strategic manager of your own financial destiny. In the long run, the “best” rate is the one that allows you to achieve your financial goals while maintaining a healthy, sustainable margin of safety.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.