In the complex ecosystem of global economics, few variables carry as much weight as the interest rate. Often described as the “price of money,” interest rates influence everything from the monthly payment on a starter home to the multi-billion dollar investment decisions of multinational corporations. For the individual consumer and the savvy entrepreneur alike, understanding the nuances of interest rates is not just an academic exercise—it is a fundamental pillar of financial literacy. Whether you are looking to borrow, save, or invest, the prevailing interest rate environment dictates the strategy you should employ to maximize your wealth and minimize your liabilities.

The Mechanics of Interest Rates: How Borrowing and Lending Work

At its core, an interest rate is the percentage of a principal amount charged by a lender to a borrower for the use of assets. While we most commonly associate interest with cash, it can also apply to consumer goods or large assets like vehicles and equipment. The interest rate compensates the lender for the risk of lending and the “opportunity cost” of not having access to that money for a specific period.

Fixed vs. Variable Rates

One of the first distinctions any borrower must understand is the difference between fixed and variable (or floating) interest rates. A fixed interest rate remains constant throughout the life of the loan. This provides predictability, making it an excellent choice for long-term debt like 30-year mortgages. Regardless of how the economy fluctuates, your payment stays the same.

Conversely, variable interest rates are tied to an underlying benchmark, such as the Prime Rate or the Secured Overnight Financing Rate (SOFR). When the benchmark rises, your interest rate rises; when it falls, your costs decrease. While variable rates often start lower than fixed rates, they carry the inherent risk of future “payment shock” if market rates climb significantly.

The Role of the Central Bank and the “Fed Funds Rate”

In the United States, the Federal Reserve (the “Fed”) acts as the primary architect of the interest rate environment. By adjusting the Federal Funds Rate—the rate at which commercial banks lend to one another overnight—the Fed influences the entire “yield curve.” When the Fed raises rates, it is typically to combat inflation by making borrowing more expensive, which slows down spending. When it lowers rates, it is attempting to stimulate a sluggish economy by making it cheaper for businesses and individuals to take out loans and spend money.

Interest Rates in Personal Finance: Mortgages, Credit Cards, and Loans

For the average individual, the question “how much is the interest rate?” usually arises during a major life milestone. The impact of a single percentage point can be the difference between financial freedom and decades of debt.

Navigating the Mortgage Market

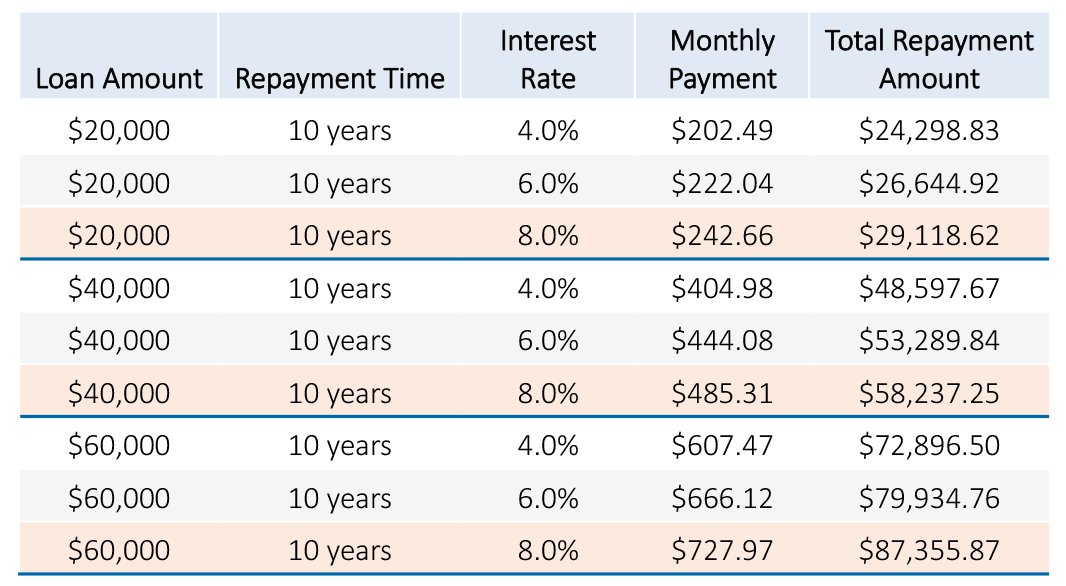

The mortgage market is perhaps the most sensitive to interest rate fluctuations. Because a home purchase involves such a large sum of money over a long duration (typically 15 to 30 years), the interest rate is the primary determinant of the total cost of the home. For example, on a $400,000 mortgage, the difference between a 4% interest rate and a 7% interest rate is over $800 per month in interest alone. Over 30 years, that equates to nearly $300,000 in additional interest paid. Understanding when to “lock in” a rate versus when to wait for a potential drop is a critical skill for any prospective homeowner.

The Cost of Consumer Debt (Credit Cards)

While mortgages are often considered “good debt” because they are tied to an appreciating asset, credit card debt falls on the opposite end of the spectrum. Credit card interest rates are notoriously high, often ranging from 18% to 29% APR (Annual Percentage Rate). Unlike mortgages, which are secured by the property, credit cards are unsecured debt. Banks charge higher rates to offset the risk that the borrower might default. Because interest on credit cards compounds—meaning you pay interest on your interest—carrying a balance can lead to a debt spiral that is difficult to escape.

Personal Loans and Credit Scores

For those looking to consolidate debt or fund a project, personal loans offer a middle ground. The interest rate you receive is heavily dependent on your credit score. A borrower with an “excellent” score (above 800) might see rates in the single digits, while someone with “fair” credit might be quoted 20% or more. This highlights the importance of maintaining a strong credit profile as a means of reducing the “price” you pay for money.

The Impact of Interest Rates on Investing and Wealth Building

Interest rates do not just affect what you owe; they also dictate what you earn. For investors, the interest rate environment is a signal that determines where capital should be allocated for the best risk-adjusted returns.

High-Yield Savings Accounts and CDs

When interest rates rise, the “silver lining” for consumers is that banks begin to pay more on deposits. High-Yield Savings Accounts (HYSAs) and Certificates of Deposit (CDs) become much more attractive. In a low-rate environment, these accounts might offer a negligible 0.50% return. However, in a rising rate environment, these yields can climb to 4% or 5%. For conservative investors or those building an emergency fund, these vehicles provide a safe, liquid way to grow capital without the volatility of the stock market.

The Inverse Relationship Between Interest Rates and Bonds

There is a fundamental rule in finance: when interest rates go up, bond prices go down. This occurs because new bonds are issued with higher yields, making existing bonds with lower yields less valuable to investors. If you hold a bond paying 3% and the market rate moves to 5%, you would have to sell your bond at a discount to entice a buyer. Understanding this relationship is vital for retirees and income-focused investors who rely on fixed-income portfolios.

Stock Market Volatility and Rate Hikes

Interest rates also influence equity valuations. When borrowing costs increase, corporate profit margins can shrink due to higher interest expenses on corporate debt. Furthermore, as the “risk-free rate” (the return on government bonds) increases, investors may pull money out of the “risky” stock market to put it into “safer” bonds or savings accounts. This shift in demand can lead to market corrections or periods of high volatility, particularly for high-growth tech companies that rely on cheap capital to fund expansion.

Strategic Financial Planning in a High-Interest Environment

Managing money when interest rates are high requires a different playbook than when rates are near zero. Adaptability is the key to maintaining a healthy balance sheet.

Debt Consolidation and Refinancing

In a fluctuating market, savvy financial planners look for opportunities to optimize their debt. If you have high-interest credit card debt, taking out a lower-interest personal loan to pay it off can save thousands in interest charges. Similarly, if you purchased a home when rates were high and they eventually drop, “refinancing”—replacing your current mortgage with a new one at a lower rate—can significantly reduce your monthly overhead.

Rebalancing Your Investment Portfolio

A change in interest rates is often a catalyst for portfolio rebalancing. If rates are rising, you might shift more capital toward short-term bonds or cash equivalents to take advantage of higher yields while minimizing the “duration risk” of long-term bonds. On the equity side, you might look for “value” stocks—companies with strong cash flows and low debt—which tend to perform better in high-interest environments than “growth” stocks that carry heavy debt loads.

Future Outlook: Predicting Rate Trends for Smarter Money Management

While no one can predict the exact movements of the market with 100% certainty, staying informed on macroeconomic trends allows you to anticipate the direction of interest rates. Factors such as the Consumer Price Index (CPI), employment data, and global geopolitical stability all influence the Fed’s decisions.

For the modern consumer, the question “how much is the interest rate?” is the starting point for a deeper conversation about financial health. By understanding how these rates are set, how they affect your personal debt, and how they drive investment returns, you move from being a passive participant in the economy to an active strategist. Whether we are in a cycle of “easy money” with low rates or a “tight money” cycle with high rates, the goal remains the same: to make informed decisions that protect your purchasing power and grow your net worth over time. In the world of money, knowledge of the interest rate is the ultimate leverage.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.