Managing your personal finances effectively often requires making tough decisions about where your capital resides. While opening a bank account is a celebrated milestone of financial literacy, closing one is an equally important administrative task that requires precision, timing, and a clear understanding of the banking ecosystem. Whether you are switching to a high-yield savings account to maximize your interest earnings, consolidating your assets for better oversight, or moving to a financial institution with lower monthly maintenance fees, the process of canceling a bank account is more nuanced than simply withdrawing your balance to zero.

Failure to follow a structured approach can lead to “zombie accounts,” unexpected overdraft fees, and unnecessary stress. This guide provides a professional roadmap to navigating the closure process, ensuring your transition is seamless and your financial reputation remains untarnished.

The Pre-Cancellation Checklist: Safeguarding Your Liquidity

Before you notify your current bank of your intent to leave, you must conduct a thorough audit of your financial life. Your bank account is the central nervous system of your personal economy, and cutting it off prematurely can lead to a cascade of failed payments.

Redirecting Automatic Payments and Direct Deposits

The most common mistake individuals make when closing an account is forgetting a recurring subscription or a utility bill. To avoid this, review at least six months of bank statements to identify all “pull” and “push” transactions.

Begin by moving your direct deposit—whether it is your primary salary, Social Security benefits, or tax refunds—to your new account. Note that payroll departments often take one to two pay cycles to process this change. Simultaneously, update your payment information for recurring expenses like rent, mortgage, insurance premiums, and streaming services. It is advisable to keep a “buffer” amount in the old account for 30 days to catch any straggling automated clearing house (ACH) transfers.

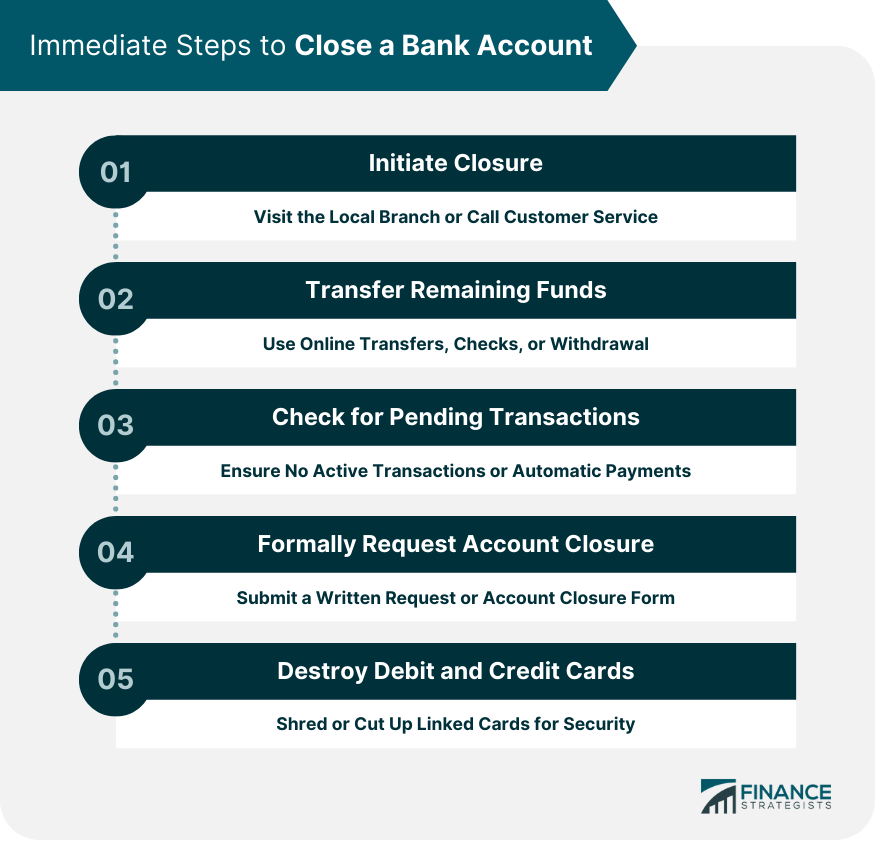

Managing Outstanding Checks and Pending Transactions

In an era of digital payments, it is easy to forget about physical checks. If you have written a check that hasn’t been cashed yet, that money is technically still spoken for. Closing the account before that check hits will result in it being returned for non-sufficient funds (NSF), which can harm your relationship with the payee and potentially incur fees. Reach out to the recipient to ensure they deposit the check, or wait until the transaction is cleared before initiating the closure. Similarly, ensure any pending debit card transactions have moved from “authorized” to “posted.”

Strategic Transfer of the Remaining Balance

Once you are confident that all pending items have cleared, it is time to move the bulk of your funds. While you can ask the bank to cut you a cashier’s check upon closure, it is often more efficient to initiate an electronic transfer (ACH) to your new institution yourself. However, be mindful of your bank’s minimum balance requirements. If you transfer every penny out a week before the account is officially closed, you might trigger a “low balance fee,” which could result in a negative balance at the time of closing. Leave a small margin (e.g., $50) to cover any final month-end service charges.

The Execution: How to Officially Terminate the Relationship

Once your financial footprint has been moved, you must formally request the closure. Simply leaving an account with a zero balance does not mean it is closed; in fact, many banks will keep a zero-balance account open and continue to charge monthly fees until the balance becomes negative, which can eventually lead to a report to ChexSystems.

Choosing the Right Closure Method

Most modern financial institutions offer three primary ways to close an account: in-person, over the phone, or via a secure online portal.

- In-Person: This is the most definitive method. By visiting a branch, you can speak with a personal banker, sign the necessary paperwork, and receive immediate documentation of the closure. If there is a small remaining balance, they can hand you the cash or a cashier’s check on the spot.

- Phone Support: If you use an online-only bank or have moved away from a physical branch, calling the customer service line is the next best option. Be prepared to verify your identity through several security questions.

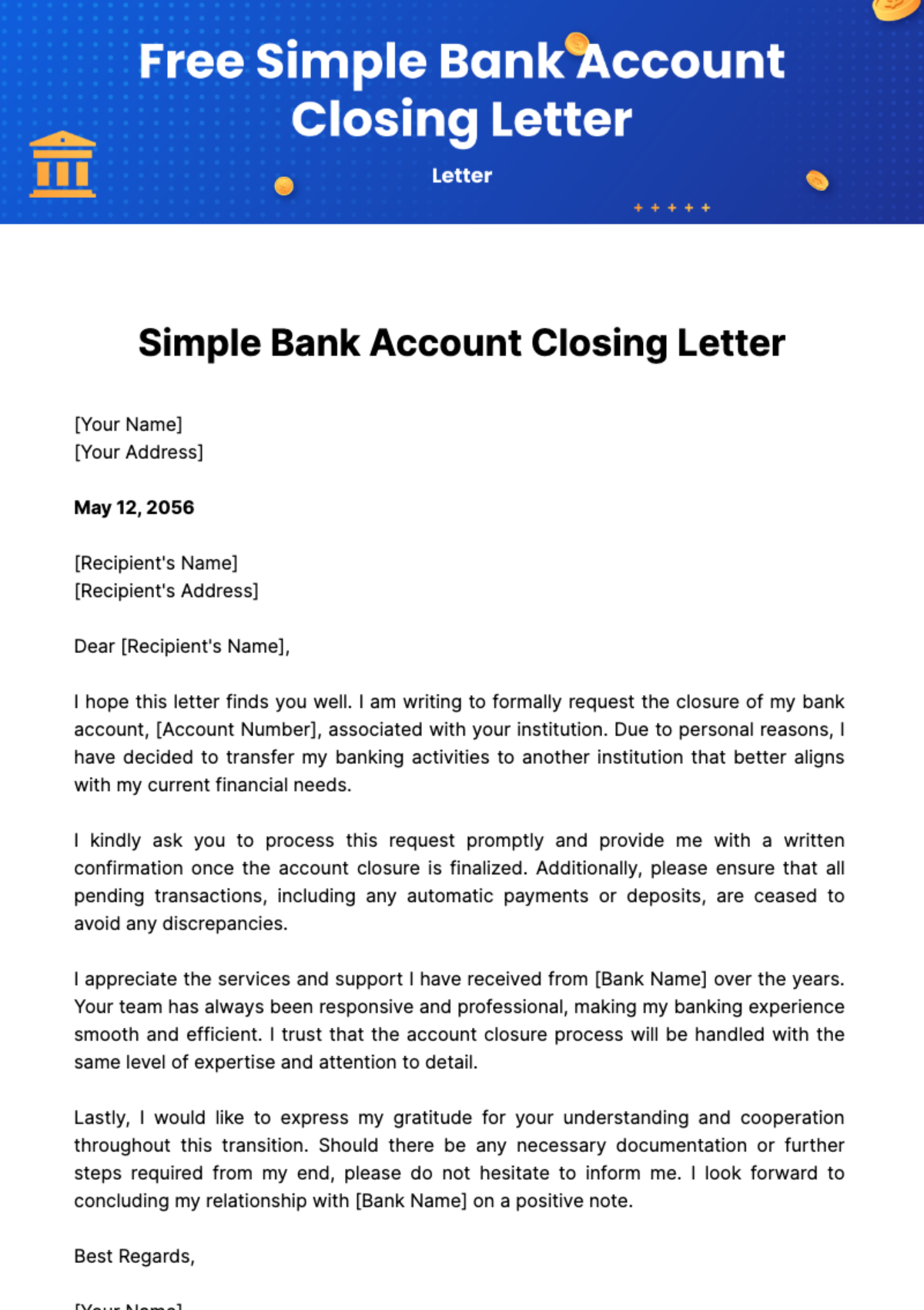

- Written Request: Some traditional institutions require a formal letter of instruction. If you choose this route, send it via certified mail with a return receipt requested. This provides a legal paper trail should the bank fail to act on your request.

Securing Written Confirmation

Never take a verbal “your account is closed” as the final word. Always request a formal “Account Closure Letter” or an email confirmation. This document is your insurance policy. It proves that the account was closed at your request and with a $0.00 balance. In the event that a “zombie” transaction reopens the account later, this documentation will be essential in disputing any subsequent fees or negative reporting to credit agencies or specialized bureaus.

Handling Joint Accounts and Specialized Products

Closing a joint account typically requires the consent—and often the signature—of both parties. If you are closing an account due to a legal separation or divorce, ensure you have a clear agreement on how the remaining funds are to be split to avoid future litigation. Furthermore, if you are closing a Certificate of Deposit (CD) before its maturity date, be prepared to pay an early withdrawal penalty, which usually equates to several months of interest. Weigh this cost against the benefits of moving the money elsewhere.

Common Pitfalls: Avoiding Financial Backlash

The process of closing a bank account is generally straightforward, but several traps can ensnare the unwary. Understanding these risks is key to maintaining a healthy financial profile.

The “Zombie Account” Phenomenon

A “zombie account” occurs when a merchant attempts to charge a closed account via an old ACH authorization. Some banks, in an attempt to be “helpful,” will automatically reopen the account to honor the payment. This immediately puts the account into a negative balance, triggering overdraft fees and daily “extended overdrawn” penalties. The best way to prevent this is to ensure every single subscription has been successfully migrated and to obtain that written confirmation that the account is permanently restricted from reopening.

Understanding the Impact on Your Credit Score

A common misconception is that closing a bank account directly affects your FICO credit score. Since bank accounts (checking and savings) are not lines of credit, they do not appear on your standard credit report. However, if an account is closed with a negative balance due to unpaid fees and you fail to settle that debt, the bank may sell the debt to a collection agency. At that point, the collection will appear on your credit report and significantly damage your score. Additionally, your history of bank account management is tracked by ChexSystems; a history of “accounts closed for cause” can make it difficult to open a new account at any bank for up to five years.

Minimum Balance and Maintenance Fees

During the transition period, you might be tempted to split your loyalty between two banks. Be cautious of the “minimum balance” requirement. If your current bank requires a $1,500 balance to waive a $15 monthly fee, and you move $1,000 to your new bank, you will be hit with that fee. Over the course of a two-month transition, that’s $30 lost for no reason. It is often better to make a “clean break” once your direct deposit has successfully landed in the new institution.

Post-Closure Hygiene: Finalizing Your Security

Once the bank has confirmed the closure, your job is not quite done. There are physical and digital security measures you must take to protect your identity and your assets.

Physical Disposal of Banking Materials

Your old checks and debit cards are a goldmine for identity thieves. Do not simply throw them in the trash. Use a cross-cut shredder for your remaining checkbooks and deposit slips. For debit cards, cut through the EMV chip and the magnetic stripe before disposing of the pieces in separate trash bags. If you have an old metal debit card, many banks provide a prepaid envelope to mail the card back for secure destruction.

Organizing Final Statements for Tax Season

When an account is closed, you may lose access to the online banking portal. This can be problematic come tax season if you need to access Form 1099-INT (for interest earned) or if you need to prove a business expense for a deduction. Before you lose access to the portal, download the last 12 to 24 months of PDF statements and any tax documents. Store these in a secure, encrypted digital folder or a physical fireproof safe.

Monitoring for Identity Theft

In the weeks following a closure, keep a close eye on your other financial accounts. While closing an account doesn’t cause identity theft, the transition period involves sharing your new routing and account numbers with various entities. Using a credit monitoring service or frequently checking your “soft” credit reports can ensure that no unauthorized accounts are being opened in your name during this period of administrative change.

Conclusion: The Path to Financial Optimization

Closing a bank account should never be an impulsive reaction to a single poor customer service experience; rather, it should be a calculated move toward better financial health. By meticulously auditing your automated transactions, following formal closure procedures, and maintaining a paper trail, you protect your liquidity and your reputation.

In the modern financial landscape, your capital should work as hard as you do. If your current institution no longer aligns with your goals—whether due to subpar technology, excessive fees, or low interest rates—you now have the professional framework to move your money to a place where it can thrive. Remember, you are the CEO of your own household finances; managing the “vendors” you use for banking is a fundamental part of that leadership role.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.