To determine what Amazon is worth, one must look far beyond the simple price tag of its stock or the total of its quarterly sales. In the realm of global finance, Amazon.com, Inc. (AMZN) represents a complex ecosystem of logistics, cloud computing, digital advertising, and consumer data. Its “worth” is a fluctuating figure that currently hovers in the trillion-dollar stratosphere, making it one of the most valuable entities in human history.

However, for investors, financial analysts, and business students, the true valuation of Amazon is found in its diversified revenue streams, its aggressive reinvestment strategies, and its unique ability to dominate multiple industries simultaneously. This article explores the financial architecture of Amazon, breaking down the metrics that define its market value and its long-term investment potential.

Understanding Market Capitalization and Shareholder Value

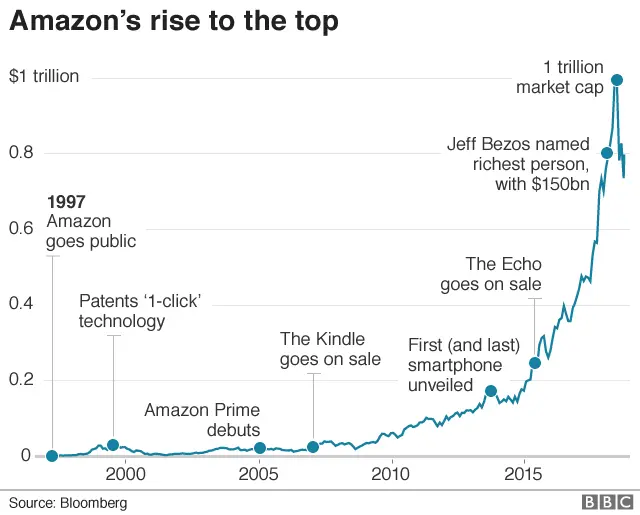

The most common answer to “what is Amazon worth” is its market capitalization. This figure is calculated by multiplying the current share price by the total number of outstanding shares. Since crossing the $1 trillion mark in 2018, Amazon has consistently vied for a top spot in the “Trillion Dollar Club” alongside tech titans like Apple, Microsoft, and Alphabet.

The Trillion-Dollar Benchmark

Market capitalization is more than just a vanity metric; it reflects the market’s collective confidence in a company’s future earnings potential. Amazon’s market cap is a testament to its transition from an online bookstore to a “utility” for modern life. When investors bid up the price of AMZN, they are not just buying into today’s retail sales; they are buying into the future of cloud infrastructure and artificial intelligence. The volatility of this market cap—often swinging by tens of billions of dollars in a single trading session—highlights how sensitive the company’s valuation is to interest rates, consumer spending data, and tech sector sentiment.

Revenue Velocity vs. Profitability Dynamics

Historically, Amazon was famous for reporting little to no net income. Founder Jeff Bezos famously prioritized “Free Cash Flow” and market share over quarterly profits. For decades, the company’s “worth” was built on the premise of deferred gratification—reinvesting every cent of profit back into warehouses, server farms, and new ventures. Today, the financial narrative has shifted. While revenue velocity remains high (approaching $600 billion annually), the company has begun to demonstrate massive profitability, particularly through its high-margin segments. This shift from a “growth-at-all-costs” model to a “profitable growth” model has fundamentally changed how Wall Street values the company’s equity.

Diversified Revenue Streams: The Pillars of Financial Strength

To understand Amazon’s total value, one must perform a “Sum-of-the-Parts” (SOTP) analysis. This financial technique values each of Amazon’s business segments as if they were independent companies. If Amazon were broken up tomorrow, several of its divisions would likely be Fortune 500 companies in their own right.

AWS: The High-Margin Engine

Amazon Web Services (AWS) is arguably the most valuable component of the Amazon empire. As the pioneer and leader in cloud computing, AWS provides the infrastructure for much of the internet. From a “Money” perspective, AWS is the company’s crown jewel because of its operating margins. While the retail division often operates on razor-thin margins of 1% to 3%, AWS frequently sees operating margins exceeding 25% to 30%. In many fiscal years, AWS has accounted for over 100% of Amazon’s total operating income, effectively subsidizing the expansion of the retail and logistics arms. Analysts often value AWS alone at over $500 billion to $800 billion, depending on the prevailing multiples for enterprise software.

The Advertising Juggernaut

A relatively new but explosive contributor to Amazon’s worth is its digital advertising business. By leveraging the data of hundreds of millions of shoppers, Amazon has built a “closed-loop” advertising system where brands can see exactly how an ad spend leads to a purchase. This segment has grown into a $40+ billion annual revenue stream. Because digital advertising has high software-driven margins and requires little physical overhead compared to shipping boxes, it has become a vital driver of the company’s overall valuation. It represents a pivot from being a merchant to being a platform—a much more lucrative financial position.

Prime and Subscription Services

Amazon Prime is the ultimate customer retention tool. With over 200 million members globally, the recurring revenue from Prime subscriptions provides a predictable and stable cash flow. Beyond the membership fees, the financial value of a Prime member is significantly higher than a non-member; Prime members tend to spend more frequently and in higher volumes. This “flywheel effect” creates a moat that competitors find nearly impossible to breach, adding a layer of “intangible” value to the company’s balance sheet.

Investment Metrics and Valuation Frameworks

When institutional investors evaluate what Amazon is worth, they look beyond the standard Price-to-Earnings (P/E) ratio. Because Amazon spends so heavily on research, development, and capital expenditures, traditional metrics can sometimes be misleading.

Price-to-Earnings and Price-to-Sales Ratios

Amazon has historically traded at a high P/E ratio compared to the broader S&P 500, often exceeding 50x or 80x. This suggests that investors are willing to pay a premium for its growth. However, many analysts prefer the Price-to-Sales (P/S) ratio or Enterprise Value-to-EBITDA for Amazon. As the company matures and its capital expenditure (CapEx) on warehouse expansion slows down, its “earnings” are becoming more visible, leading to a gradual normalization of these ratios. The current valuation reflects a balance between its legacy as a high-growth tech stock and its new reality as a cash-generating industrial powerhouse.

Free Cash Flow: The North Star

For Amazon, Free Cash Flow (FCF) is the ultimate metric of worth. It represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. Investors watch FCF closely because it determines Amazon’s ability to fund new moonshot projects (like Project Kuiper satellite internet), acquire other companies (like One Medical or MGM), or eventually initiate share buybacks and dividends. A dip in FCF due to heavy investment in AI or logistics is usually viewed by the market as a temporary “investment phase” rather than a loss of value.

Future Growth Projections and Risks

The “forward” worth of Amazon depends on its ability to capture the next wave of technological commerce. This includes the integration of Generative AI to optimize supply chains and personalize the shopping experience. However, financial risks persist. Antitrust litigation in the US and Europe poses a threat to the company’s structure. If regulatory bodies were to force a spin-off of AWS, the financial profile of “Amazon Retail” would look very different. Therefore, the current valuation includes a “regulatory discount” as investors weigh the potential for a forced breakup.

The Logistics Moat and Capital Assets

Finally, any assessment of Amazon’s worth must include its massive physical footprint. Amazon is no longer just an “internet company”; it is a global transportation and logistics titan that rivals UPS and FedEx.

The Economic Value of the Fulfillment Network

Over the last decade, Amazon has spent hundreds of billions of dollars building a proprietary logistics network, including thousands of fulfillment centers, a fleet of “Prime Air” cargo planes, and a last-mile delivery system. In financial terms, this represents a “moat”—a competitive advantage that is too expensive for any newcomer to replicate. The replacement cost of this infrastructure is astronomical. When valuing Amazon, one must account for the hundreds of millions of square feet of real estate and the sophisticated automation technology housed within those walls. This physical infrastructure ensures that Amazon remains the “lowest-cost provider” in many categories, which is the bedrock of long-term business finance.

Data as a Financial Asset

In the modern economy, data is often compared to oil. Amazon’s worth is intrinsically tied to its vast repository of consumer behavior data. This data allows for hyper-efficient inventory management, reducing the “carrying costs” of goods. It also fuels the high-margin advertising and AWS AI services mentioned earlier. While data doesn’t appear as a line item on a balance sheet, its ability to drive efficiency and open new revenue streams is a primary reason why the market assigns Amazon such a high valuation multiple.

Conclusion: A Multi-Dimensional Valuation

So, what is Amazon worth? Financially, it is a trillion-dollar entity defined by its dual identity: a high-volume, low-margin retail giant and a lower-volume, high-margin technology provider. Its worth is found in the synergy between these parts—where the retail side provides the scale and data, and the cloud/advertising side provides the profits and growth.

For the investor, Amazon’s worth is a calculation of its future cash flows, discounted back to the present. While the numbers on the ticker symbol will change daily, the underlying value of the company remains anchored in its dominance over the digital and physical infrastructure of global commerce. Whether viewed through the lens of market cap, asset value, or cash flow, Amazon remains a fundamental pillar of the modern financial landscape, continuing to redefine what a “business” can be in the 21st century.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.