When you look at the landscape of modern personal finance, few tools are as iconic or as distinctive as the American Express card. Whether you are holding a classic Green Card, a high-status Platinum Card, or a business-centric Gold Card, you may have noticed that it looks and feels slightly different from your other plastic. One of the most immediate points of differentiation is the sequence of numbers printed on the front. While the vast majority of credit cards in your wallet likely feature a 16-digit sequence, American Express follows its own path.

So, how many digits are on an Amex card? The answer is 15.

While this may seem like a minor technical detail, the 15-digit structure is a cornerstone of the American Express financial identity. It reflects a unique history, a specific security architecture, and a specialized approach to transaction processing. In this comprehensive guide, we will explore the anatomy of the Amex numbering system, the security features that protect your wealth, and how this unique tool fits into a sophisticated personal finance strategy.

The Anatomy of an American Express Card Number

To understand the 15-digit Amex number, one must look at the international standards that govern the financial world. Most payment cards follow the ISO/IEC 7812 standard, which provides a numbering system for card issuers. However, American Express utilizes a configuration that sets it apart from competitors like Visa, Mastercard, and Discover.

Why 15 Digits Instead of 16?

The 16-digit format used by Visa and Mastercard is organized into four blocks of four. American Express, conversely, organizes its 15 digits into three distinct blocks: a group of four, a group of six, and a group of five (4-6-5).

This difference is rooted in the legacy of the American Express network. Unlike Visa or Mastercard, which are primarily payment networks that partner with banks (like Chase or Bank of America) to issue cards, American Express often acts as both the network and the issuing bank. This “closed-loop” system allowed Amex to develop its own internal numbering logic without needing to conform to the 16-digit “interbank” standards that emerged later.

Breaking Down the Number Segments

Every digit on an American Express card serves a specific financial purpose. You can think of these numbers as a coded language that tells a merchant’s terminal exactly who you are and where the money is coming from.

- The Major Industry Identifier (MII): The first digit of any card indicates the industry of the issuer. Amex cards always begin with the number 3, specifically 34 or 37. In the ISO system, the number 3 is reserved for the travel and entertainment industry—a nod to Amex’s origins as a freight and travel company.

- The Issuer Identifier: The first six digits (including the MII) make up the Issuer Identification Number (IIN). This identifies American Express as the institution responsible for the transaction.

- The Account Identifier: Digits 7 through 14 are unique to the individual cardholder. This is your specific account number within the American Express ecosystem.

- The Check Digit: The 15th and final digit is the “checksum.” It is calculated using the Luhn algorithm, a mathematical formula used to validate the card number and prevent errors during manual entry.

The Role of the IIN in Global Finance

The Issuer Identification Number (IIN) is crucial for the seamless flow of global commerce. When you swipe your card at a boutique in Paris or enter it into an e-commerce site in Tokyo, the IIN tells the merchant’s payment processor that the transaction must be routed through the American Express network. Because Amex manages its own network, these 15 digits facilitate a direct line of communication between the merchant and the cardholder’s credit line, often leading to faster dispute resolutions and specialized fraud monitoring.

Security Features Beyond the Digits

In the world of personal finance, security is paramount. A credit card number is only as good as the protections surrounding it. American Express has developed a proprietary security architecture that complements its 15-digit numbering system, ensuring that cardholders’ assets remain protected against unauthorized use.

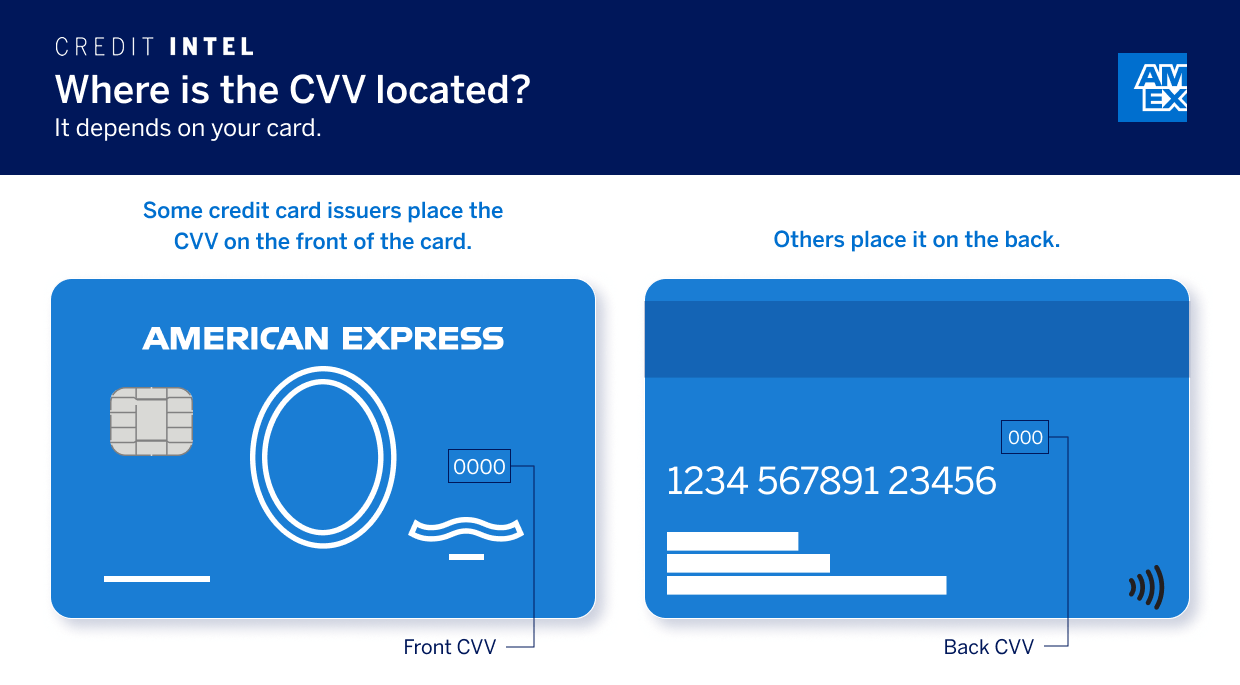

The 4-Digit CVV/CID Code

Perhaps the most significant security difference between Amex and its peers is the Card Identification Number (CID). If you look at a Visa or Mastercard, you will find a 3-digit CVV (Card Verification Value) on the back of the card near the signature strip.

American Express uses a 4-digit CID, which is located on the front of the card, usually positioned above the 15-digit account number. This 4-digit code is an extra layer of security for “card-not-present” transactions, such as online shopping. Because the 4-digit code is not encoded in the magnetic stripe or the chip, it is much harder for hackers to obtain during data breaches that target physical terminals.

Chip-and-PIN and Contactless Technology

While the 15 digits define the card’s identity, the EMV chip defines its physical security. American Express was an early adopter of chip technology, which creates a unique, one-time code for every transaction. This makes it virtually impossible for fraudsters to “clone” the card.

Furthermore, Amex has integrated Near Field Communication (NFC) for contactless payments. When you tap your 15-digit card at a terminal, the card transmits a tokenized version of your account number. This means the actual 15 digits are never shared with the merchant’s system, adding a robust layer of digital privacy to your financial transactions.

Virtual Card Numbers for Enhanced Privacy

For the tech-savvy investor or the security-conscious consumer, American Express offers virtual card numbers. Through their mobile app and partnerships with various digital wallets, Amex allows users to generate temporary or merchant-specific card numbers. These virtual numbers may still follow the Amex logic, but they act as a “mask” for your primary 15-digit account number. If a merchant’s database is compromised, your real financial information remains untouched, allowing you to manage your money with peace of mind.

Comparing American Express to Other Major Networks

To truly appreciate the 15-digit Amex card, one must understand how it sits within the broader financial landscape. The global credit market is dominated by four major players: Visa, Mastercard, American Express, and Discover.

Visa and Mastercard: The 16-Digit Standard

Visa and Mastercard serve as open-loop networks. They do not issue cards directly to consumers; instead, they provide the infrastructure for thousands of different banks. Because of this high volume and variety of issuers, they adopted a 16-digit format to accommodate the massive number of possible account combinations.

For the consumer, the difference is mostly felt during data entry. Most online forms are programmed to recognize that a 15-digit number starting with “3” is an Amex, and a 16-digit number starting with “4” is a Visa. If you find yourself unable to click “Submit” on a payment page, it is often because the website’s validation logic is incorrectly expecting 16 digits for an Amex card.

Why the Difference Matters for Online Shopping

The 15-digit structure occasionally presents a minor hurdle in the user experience of digital finance. Some older or poorly coded payment gateways are hardwired for 16 digits. In these cases, users might mistakenly try to add a leading zero or a trailing digit to make it “fit.” However, as American Express continues to hold a massive share of the high-net-worth market, almost all modern financial tools and e-commerce platforms have optimized their systems to recognize the 4-6-5 spacing of the American Express 15-digit sequence.

Global Acceptance and Transaction Processing

Historically, some merchants were hesitant to accept Amex due to its unique network and slightly higher merchant fees. However, from a financial tool perspective, the gap in acceptance has narrowed significantly. Today, the 15-digit card is accepted by millions of merchants worldwide. The distinctive numbering system acts as a signal to the merchant’s terminal to apply specific processing rules that are unique to American Express, such as specialized “Level 3” data for corporate cards, which helps businesses track spending with more granularity than a standard 16-digit card might allow.

Managing Your American Express Account for Financial Success

An American Express card is more than just a 15-digit number; it is a gateway to a suite of financial tools designed to optimize your spending, rewards, and credit health. Understanding how to use this tool effectively is a key component of sophisticated money management.

Understanding Credit vs. Charge Cards

One of the most important distinctions in the Amex ecosystem is the difference between a credit card and a charge card.

- Credit Cards: These have a fixed credit limit and allow you to carry a balance from month to month while paying interest.

- Charge Cards: Many of Amex’s most famous cards (like the Platinum and Gold) were traditionally “charge cards,” meaning they have no pre-set spending limit but require the balance to be paid in full every month.

While Amex has introduced “Pay Over Time” features for many of its cards, treating your 15-digit Amex like a charge card is often a superior financial strategy. It encourages disciplined spending habits and ensures that you never fall into the trap of high-interest debt.

Leveraging Amex Financial Tools and Rewards

The 15-digit number on your card is your key to the Membership Rewards (MR) program. In the world of personal finance, MR points are often considered the “gold standard” of loyalty currency because of their flexibility. You can transfer these points to various airline and hotel partners, often gaining significantly more value than a simple cash-back card would provide.

Furthermore, American Express provides cardholders with robust financial tracking tools. Their “Spend Analysis” features allow you to categorize your purchases, which is essential for budgeting and tax preparation. By monitoring your 15-digit account through the Amex app, you can see real-time updates on your net worth impact and adjust your spending habits accordingly.

Best Practices for Maintaining Security

Because the American Express brand is associated with higher spending power, it can sometimes be a target for phishing and fraud. To protect your financial standing, always follow these best practices:

- Never share your 4-digit CID: While many people know not to share their 15-digit card number, they are often less cautious with the CID. Treat those four digits with the same secrecy as your PIN.

- Enable Push Notifications: Use the Amex mobile app to set up alerts for every transaction. If a 15-digit number is used without your permission, you will know instantly.

- Utilize “Freeze Card”: If you misplace your card, use the app to freeze it immediately. This prevents any transactions from being processed on your 15-digit account until you find the physical card.

Conclusion

The 15-digit sequence on an American Express card is far more than a numerical quirk; it is a symbol of a unique financial legacy and a testament to a specialized approach to money management. From the initial “3” that identifies its travel heritage to the 4-digit CID that guards its front, every aspect of the Amex card is designed for a specific purpose within the global economy.

By understanding the structure of your Amex card, the security features that protect it, and the financial strategies that leverage its unique position in the market, you can better navigate the complexities of personal finance. Whether you are using it to earn rewards, manage business expenses, or simply facilitate daily transactions, the 15 digits of your American Express card remain one of the most powerful tools in your financial arsenal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.