The decision to purchase a used vehicle is often a financially savvy one, offering a more accessible entry point to car ownership compared to buying new. However, the sticker price is merely the beginning of the financial journey. A crucial, and often overlooked, component of the total cost is the interest rate applied to your auto loan. This rate can dramatically influence your monthly payments and the overall expense of the vehicle over its lifespan. Understanding what constitutes these rates, the factors that dictate them, and how to secure the most favorable terms is paramount for any prospective used car buyer. This comprehensive guide will dissect the intricacies of used vehicle interest rates, offering insights to empower your financial decisions.

Understanding Used Vehicle Interest Rates

At its core, an interest rate is the cost of borrowing money, expressed as a percentage of the principal loan amount. When financing a used vehicle, this rate is added to your monthly payments, compensating the lender for the risk and opportunity cost associated with providing you capital. While the concept seems straightforward, several nuances distinguish used vehicle loan rates from other forms of borrowing.

The Basics of Auto Loan Interest

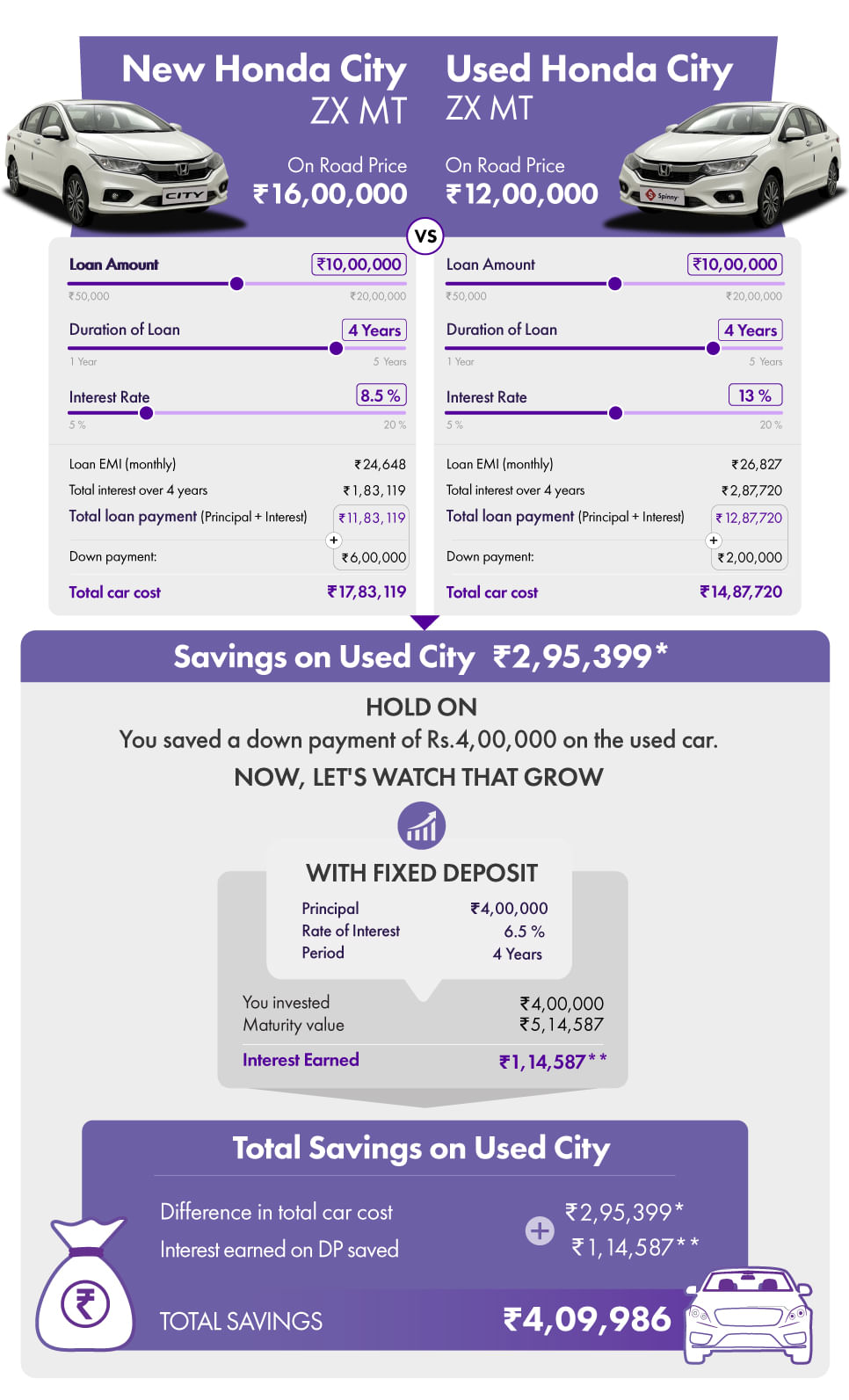

An auto loan is a secured loan, meaning the vehicle itself serves as collateral. Should you default on your payments, the lender has the right to repossess the car to recover their losses. This security typically allows for lower interest rates compared to unsecured loans (like personal loans or credit cards), as the lender’s risk is mitigated. The interest rate determines how much extra you pay beyond the vehicle’s purchase price. A higher interest rate means more money going towards interest and less towards paying down the principal with each payment, increasing the total cost of ownership.

Why Used Car Rates Differ from New Car Rates

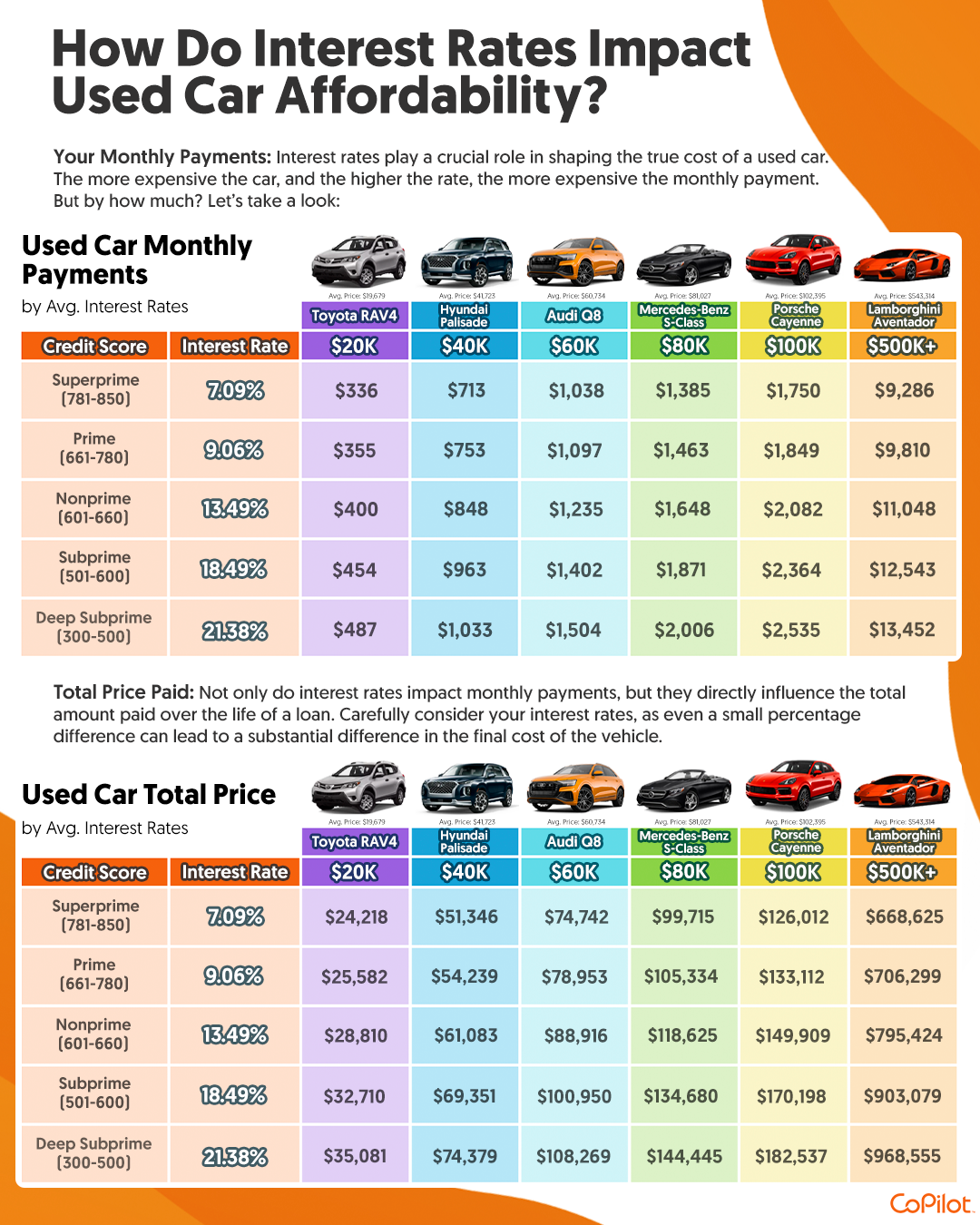

It’s a common observation that interest rates on used vehicles tend to be higher than those on brand-new cars. Several factors contribute to this disparity. Firstly, new cars often come with manufacturer incentives, including subsidized financing rates, to stimulate sales. These “special rates” are rarely available for used vehicles. Secondly, new cars generally have a predictable depreciation schedule and a higher resale value at the outset, making them less risky collateral for lenders. Used cars, by their nature, have already undergone significant depreciation, and their future value can be less certain, depending on age, mileage, and condition. This increased risk for the lender often translates into a higher interest rate for the borrower.

Key Factors Influencing Your Rate

The interest rate you are ultimately offered is not arbitrary. It’s the result of a complex interplay of personal financial health, the specifics of the loan, and the broader economic environment. Your credit score is arguably the most significant individual factor, but it’s far from the only one. The loan term, the amount of your down payment, the age and mileage of the vehicle, and even the current market interest rates all play a crucial role in shaping the final percentage.

The Core Determinants of Your Used Car Loan Rate

Navigating the landscape of used car financing requires a deep understanding of the variables that lenders scrutinize. By identifying these critical determinants, borrowers can take proactive steps to improve their financial standing and secure more favorable loan terms.

Your Credit Score: The Ultimate Predictor

Your credit score is a numerical representation of your creditworthiness, derived from your credit history. It signals to lenders how likely you are to repay your debts. Individuals with excellent credit scores (typically 720 and above) are perceived as low-risk borrowers and consequently qualify for the lowest interest rates. Conversely, those with fair or poor credit scores (below 660) are deemed higher risk, leading to significantly higher interest rates, if approved at all. Lenders use these scores to gauge your past payment behavior, existing debt load, and overall financial responsibility.

Loan Term and Down Payment Impact

The loan term refers to the length of time you have to repay the loan. Shorter loan terms (e.g., 24-36 months) generally come with lower interest rates because the lender’s risk exposure is reduced over a shorter period. However, shorter terms also mean higher monthly payments. Longer loan terms (e.g., 60-72 months) reduce monthly payments but typically result in higher interest rates, and you’ll pay more interest over the life of the loan.

A substantial down payment also plays a pivotal role. By putting down a significant portion of the vehicle’s price upfront, you reduce the amount you need to borrow, which in turn lowers the lender’s risk. A larger down payment can often lead to a lower interest rate, as it demonstrates your financial commitment and reduces the likelihood of owing more than the car is worth (being “upside down” on the loan) as it depreciates.

Vehicle Age and Mileage

Unlike new cars, the age and mileage of a used vehicle directly impact its perceived reliability and future resale value. Lenders view older vehicles with higher mileage as riskier collateral because they are more prone to mechanical issues and depreciate faster. This increased risk often translates into higher interest rates for older, high-mileage cars. Some lenders even have limits on the age or mileage of vehicles they are willing to finance. The type of vehicle also matters; luxury or niche vehicles might be harder to resell, impacting their loan terms.

Economic Environment and Lender Policies

Beyond personal factors and vehicle specifics, broader economic conditions influence interest rates. When the Federal Reserve raises its benchmark interest rate, it typically causes rates across the economy, including auto loan rates, to increase. Conversely, a period of economic slowdown might see rates drop to stimulate borrowing and spending. Furthermore, different lenders (banks, credit unions, dealership financing arms) have their own internal policies, risk assessment models, and profit margins, leading to variations in the rates they offer for similar borrowers and vehicles.

Navigating the Used Vehicle Financing Landscape

Securing the best possible interest rate requires more than just understanding the contributing factors; it demands a strategic approach to the financing process itself. From where you seek your loan to how you prepare for the application, informed decisions can lead to substantial savings.

Comparing Loan Offers: Dealership vs. Banks vs. Credit Unions

The marketplace for auto loans is diverse. Dealerships often offer convenient, on-site financing, sometimes even with competitive rates, especially if they have strong relationships with multiple lenders. However, their primary focus is selling cars, and their financing options might not always be the most competitive for the borrower.

Traditional banks are a common source for auto loans. They offer a range of products and often have established relationships with their customers. Credit unions, on the other hand, are member-owned financial cooperatives. They are often known for offering some of the most competitive interest rates and more flexible terms, as their non-profit status allows them to pass savings onto their members. It is always wise to obtain loan quotes from at least two to three different types of lenders to ensure you are getting the most favorable terms.

The Power of Pre-Approval

One of the most potent tools in a used car buyer’s arsenal is loan pre-approval. Before you even step foot on a dealership lot, apply for a loan with your bank or credit union. A pre-approval letter specifies the maximum loan amount you qualify for and the interest rate you can expect. This not only gives you a clear budget but also transforms you into a cash buyer in the eyes of the dealership. With pre-approval in hand, you can negotiate the vehicle’s price more effectively, separate from the financing discussion, and use the pre-approved rate as a benchmark against any financing offers the dealership might present.

Understanding APR vs. Interest Rate

While often used interchangeably, the interest rate and the Annual Percentage Rate (APR) are distinct. The interest rate is the percentage you pay on the principal loan amount. The APR, however, represents the true annual cost of borrowing. It includes the interest rate plus any additional fees or charges associated with the loan, such as origination fees, application fees, or closing costs. When comparing loan offers, always focus on the APR, as it provides a more accurate picture of the total cost of the loan over a year. A lower interest rate might look appealing, but a higher APR due to hidden fees could make it a more expensive option overall.

Strategies to Secure a Lower Interest Rate

Armed with knowledge of how interest rates are determined and how to navigate the financing market, you can now employ specific strategies to actively reduce the rate you’re offered. These steps can lead to significant savings over the life of your used car loan.

Improving Your Credit Before Applying

Since your credit score is paramount, taking steps to enhance it before applying for a loan is highly effective. This includes:

- Paying bills on time: Payment history is the most significant factor in your credit score.

- Reducing existing debt: A lower credit utilization ratio (how much credit you use vs. how much you have available) can boost your score.

- Checking your credit report for errors: Disputing and correcting inaccuracies can quickly improve your score.

- Avoiding new credit applications: Each hard inquiry can temporarily ding your score.

Even a modest improvement in your credit score can move you into a better rate tier, saving you hundreds or even thousands of dollars over the loan term.

Making a Substantial Down Payment

As discussed, a larger down payment reduces the loan principal and the lender’s risk. Aim for at least 20% of the vehicle’s purchase price, if feasible. This not only typically results in a lower interest rate but also means you’ll finance less, pay less interest overall, and reach equity in your vehicle faster. Moreover, a significant down payment acts as a buffer against rapid depreciation, preventing you from being “underwater” on your loan (owing more than the car is worth).

Considering a Shorter Loan Term

While a longer loan term offers lower monthly payments, it almost always comes with a higher interest rate and a greater total cost of interest over the life of the loan. If your budget allows, opt for the shortest loan term possible. You’ll pay off the vehicle faster, pay less in interest, and achieve full ownership sooner. Calculate whether the slightly higher monthly payment for a shorter term is manageable within your budget, as the long-term savings can be substantial.

Refinancing Options Post-Purchase

Even if you secure what seems like a decent rate initially, the journey doesn’t have to end there. If your credit score improves significantly after you’ve purchased the vehicle, or if market interest rates drop, you might be eligible to refinance your auto loan. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can reduce your monthly payments, the total interest paid, or both. Keep an eye on market rates and your credit score, and explore refinancing options a year or two after your original purchase.

The Long-Term Financial Implications

Understanding used vehicle interest rates goes beyond securing a good deal today; it’s about making financially sound decisions that impact your budget and wealth accumulation for years to come.

Total Cost of Ownership Beyond the Sticker Price

The interest rate is a critical component of the total cost of ownership. A lower interest rate means more of your monthly payment goes towards the principal, reducing the overall amount you pay for the vehicle. Conversely, a high interest rate can add thousands to the effective price of the car. Factor in not just the purchase price, but the total interest paid, insurance, maintenance, and fuel costs when assessing the true affordability of a used vehicle. Overlooking the impact of interest can lead to financial strain and divert funds from other important financial goals.

Budgeting for Your Used Vehicle Loan

Integrating your used vehicle loan payment into your overall budget is essential. Use online loan calculators to estimate your monthly payments based on different interest rates and loan terms. Ensure that this payment, combined with other car-related expenses, fits comfortably within your monthly financial plan without stretching your budget too thin. A good rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 15-20% of your net income.

The Value of Smart Financial Decisions

Securing a favorable interest rate on a used vehicle loan is more than just saving money; it’s a testament to smart financial planning and decision-making. By understanding the factors at play, strategically preparing your finances, and diligently comparing offers, you empower yourself to make a purchase that supports your long-term financial health. The journey to used car ownership, when approached with financial acumen, can be a rewarding and cost-effective path to mobility.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.