For many, purchasing a car represents one of the most significant financial decisions after buying a home. Whether it’s a brand-new vehicle or a reliable pre-owned model, understanding the financing behind it is paramount. At the heart of car financing lies the interest rate—a critical factor that dictates not just your monthly payment, but the total cost of your vehicle over the loan’s lifetime. Far more than just a number, the interest rate is a dynamic figure influenced by a multitude of personal financial elements, market conditions, and the specifics of the loan itself. Navigating the complexities of car loan interest rates requires a clear understanding of its definition, the forces that shape it, and the strategies available to secure the most favorable terms. This comprehensive guide aims to demystify car loan interest rates, empowering prospective car buyers with the knowledge to make informed, financially sound decisions.

The Fundamentals of Car Loan Interest Rates

To effectively approach car financing, one must first grasp the foundational concepts of interest rates and how they apply specifically to vehicle loans. This understanding forms the bedrock upon which all subsequent financial decisions will be built.

Defining Interest Rates and APR

At its core, an interest rate is the cost of borrowing money, expressed as a percentage of the principal amount. When you take out a car loan, the lender charges interest as compensation for lending you the money to purchase the vehicle. This percentage is typically calculated annually.

However, a more comprehensive measure for car loans is the Annual Percentage Rate (APR). While the interest rate reflects just the cost of borrowing the principal, the APR encompasses the interest rate plus any additional fees associated with the loan, such as administrative charges, origination fees, or documentation costs. The APR provides a more accurate representation of the total annual cost of your loan, making it the most effective tool for comparing different loan offers. Always compare APRs, not just interest rates, to get a true sense of the cheapest financing option.

Why Interest Rates Matter for Car Buyers

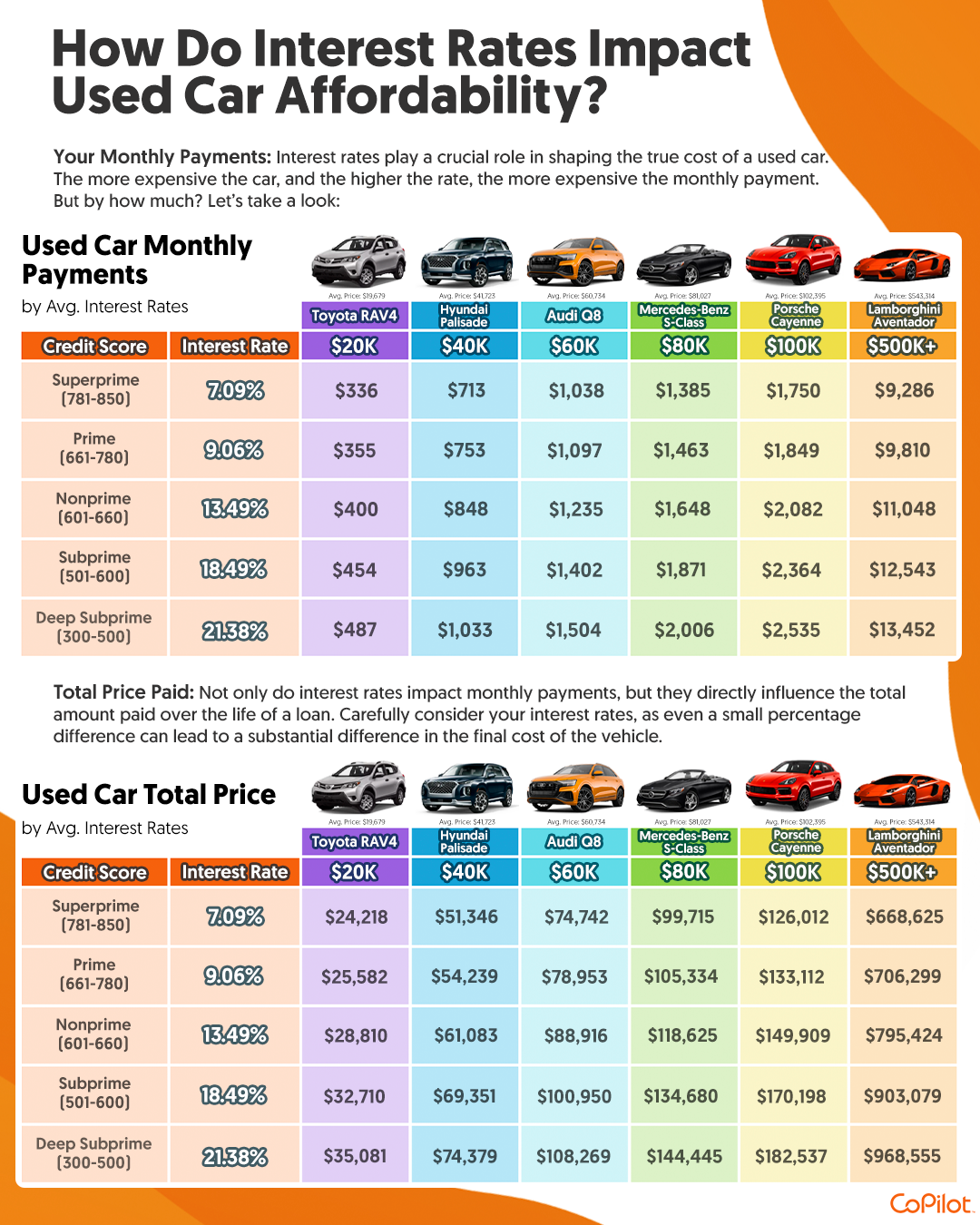

The interest rate on your car loan has a profound impact on two primary aspects of your vehicle purchase: your monthly payment and the total amount you will pay over the life of the loan. A higher interest rate translates directly to higher monthly payments and a substantially larger total cost for the car, even if the sticker price remains the same.

For example, a $30,000 car financed over five years (60 months) at a 3% APR would result in a monthly payment of approximately $539 and a total interest paid of around $2,340. The same car at a 7% APR would push the monthly payment to about $594 and the total interest paid to roughly $5,640—a difference of over $3,300 in interest alone. This demonstrates how even a few percentage points can significantly alter your financial commitment and impact your overall budget. Understanding this impact allows buyers to prioritize securing the lowest possible rate.

Fixed vs. Variable Interest Rates

Car loans primarily come with two types of interest rates: fixed or variable.

- Fixed-rate loans are by far the most common for auto financing. With a fixed rate, your interest rate remains constant throughout the entire loan term. This means your monthly payment for the principal and interest will never change, offering predictability and stability in your budgeting. For most consumers, a fixed-rate loan is preferable as it eliminates the risk of fluctuating payments due to market changes.

- Variable-rate loans, while less common for car purchases, have an interest rate that can change over the loan term based on a specified index, such as the prime rate. If the index rises, your interest rate and monthly payments could increase; if it falls, they could decrease. While a variable rate might offer a lower initial payment, it introduces an element of unpredictability, which can be a significant risk for long-term financial planning. Given the choice, most advisors recommend fixed-rate auto loans for their inherent stability.

Key Factors Influencing Your Car Loan Interest Rate

The interest rate you are offered on a car loan is not arbitrary; it’s a carefully calculated figure based on a risk assessment by the lender. Numerous factors contribute to this assessment, with some carrying more weight than others. Understanding these influences is crucial for preparing yourself to secure the most competitive rate.

Your Credit Score: The Primary Driver

Without question, your credit score is the single most significant factor in determining the interest rate you’ll receive. Lenders use your credit score, derived from your credit report, as a quick snapshot of your creditworthiness and your likelihood of repaying the loan. A higher credit score (typically FICO scores of 700 and above) indicates a lower risk to lenders, which translates into lower interest rates. Conversely, a lower credit score suggests a higher risk, leading to higher interest rates to compensate the lender for that perceived risk. This emphasizes the importance of maintaining good credit health long before you even consider applying for a car loan.

Loan Term and Down Payment

The loan term, or the length of time you have to repay the loan, also plays a crucial role. Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates because the lender’s money is tied up for a shorter period, reducing their risk exposure. However, shorter terms also mean higher monthly payments. Longer terms (e.g., 72 or 84 months) often have higher interest rates but lower monthly payments, making the car seem more affordable on a month-to-month basis, though you’ll pay significantly more in total interest.

A substantial down payment can also positively influence your interest rate. A larger down payment reduces the amount you need to borrow, thus decreasing the lender’s risk. It also demonstrates your financial commitment and ability to save, often leading to more favorable terms. Lenders prefer borrowers who have equity in their vehicle from the start.

Vehicle Type (New vs. Used) and Age

The type and age of the vehicle you intend to purchase can also affect your interest rate. Generally, new car loans tend to have lower interest rates than used car loans. This is because new cars are seen as less of a risk; they depreciate slower initially, have warranties, and often qualify for manufacturer incentives.

Used cars, on the other hand, carry a higher perceived risk due to their unknown history, potential for more immediate maintenance issues, and faster depreciation curve. Lenders account for this higher risk by charging higher interest rates on used car loans. Within the used car market, older vehicles typically command higher rates than newer used models.

Lender Type and Market Conditions

The specific lender you choose can significantly impact the rate you receive. Different financial institutions—banks, credit unions, online lenders, and dealership finance departments—have varying lending criteria, risk appetites, and overheads, leading to a range of interest rates. Credit unions, for instance, are often known for offering very competitive rates to their members.

Furthermore, broader market conditions and the overall economic climate, particularly the prevailing federal interest rates set by central banks, will influence lending rates across the board. When the economy is strong and rates are low, car loan rates tend to be more favorable. Conversely, in periods of economic tightening, rates generally rise. Staying aware of these macro-economic trends can help you time your car purchase more advantageously.

Strategies to Secure the Best Possible Car Loan Interest Rate

Armed with an understanding of what drives interest rates, you can proactively employ strategies to position yourself for the most advantageous financing terms. Securing a low interest rate isn’t just about luck; it’s about preparation and smart consumer behavior.

Improving Your Credit Health

Given that your credit score is the dominant factor, actively working to improve it should be a top priority if you’re not already in the “excellent” category. This involves several key practices:

- Pay all bills on time, every time: Payment history is the most critical component of your credit score.

- Reduce outstanding debt: Especially credit card debt. Lowering your credit utilization ratio (the amount of credit you’re using versus the amount available) can significantly boost your score.

- Avoid opening new credit accounts unnecessarily: Too many recent credit inquiries can temporarily lower your score.

- Check your credit report regularly: Dispute any errors that could be negatively impacting your score.

Implementing these habits well in advance of applying for a car loan can yield substantial benefits in terms of interest rates.

Shopping Around for Lenders

Never accept the first loan offer you receive, especially from a dealership. Instead, treat financing as a separate shopping process.

- Get pre-approved: Apply for pre-approval from multiple lenders (banks, credit unions, online lenders) before you even step foot in a dealership. This gives you a clear understanding of the interest rate you qualify for and establishes a benchmark. Pre-approvals usually only involve a “soft” credit inquiry initially, which doesn’t harm your score.

- Compare APRs: Remember to compare the Annual Percentage Rate (APR) from different offers, not just the quoted interest rate, to get the full picture of the cost.

- Leverage offers: Use a competitive pre-approval offer to negotiate with the dealership’s finance department. They might be able to beat your external offer, but you won’t know unless you have a strong alternative.

Negotiating Terms Beyond the Rate

While the interest rate is critical, it’s not the only negotiable aspect of your loan. You can also negotiate:

- The loan term: A shorter term might increase your monthly payment but drastically reduce total interest.

- Fees: Some lenders may be willing to waive or reduce certain administrative or origination fees, which directly impacts your APR.

- Down payment: If you can afford a larger down payment, it can lower the total amount financed and potentially reduce your interest rate.

Focusing solely on the monthly payment can be a trap; always look at the full picture of the loan terms.

Considering a Co-signer or Higher Down Payment

If your credit score isn’t ideal, or if you’re a first-time buyer with a limited credit history, considering a co-signer with excellent credit can significantly improve your chances of securing a lower interest rate. A co-signer essentially shares the responsibility for the loan, mitigating the lender’s risk. However, this is a serious commitment for the co-signer, as their credit will be affected if you miss payments.

Alternatively, if a co-signer isn’t an option, focusing on saving a larger down payment can serve a similar purpose by reducing the amount you need to borrow and showing the lender your financial commitment, thereby potentially lowering the perceived risk and the interest rate offered.

Calculating and Understanding Your Total Loan Cost

Beyond the monthly payment, truly understanding the financial impact of your car loan means grasping the total cost over its lifetime. This involves not just the principal amount borrowed, but every dollar paid in interest and fees.

The Impact of Interest on Total Payments

As illustrated earlier, interest is not merely an abstract percentage; it’s a tangible cost that adds significantly to the purchase price of your vehicle. The longer the loan term, the more interest you will pay, even if the interest rate is relatively low. This is because the principal amount outstanding remains higher for a longer period, allowing interest to accrue for more months. This phenomenon is often overlooked when buyers focus solely on achieving the lowest possible monthly payment, extending their loan term to make it “affordable” without realizing the substantial long-term financial penalty.

Using Online Calculators and Amortization Schedules

To gain a clear picture of your total loan cost, leverage readily available financial tools:

- Online car loan calculators: These tools allow you to input different scenarios (loan amount, interest rate, term length) to see how they affect your monthly payment and total interest paid. They are excellent for comparing different loan offers or for planning your budget.

- Amortization schedules: An amortization schedule is a table that breaks down each loan payment into its principal and interest components over the entire loan term. It shows how much of each payment goes towards reducing your principal versus how much goes to the lender as interest. Reviewing an amortization schedule highlights how much interest is paid in the early stages of a loan (when a larger portion of your payment goes to interest) and how the balance shifts towards principal reduction over time.

The True Cost of a Low Monthly Payment

While a low monthly payment might seem attractive and make a more expensive car appear within reach, it often comes at the expense of a longer loan term and, consequently, a higher total interest paid. This is a crucial distinction: a low monthly payment does not necessarily equate to a low total cost. Consumers can inadvertently pay thousands more for their vehicle by extending the loan duration just to shave a few dollars off each month’s bill. It’s essential to strike a balance between an affordable monthly payment and a reasonable total cost, aiming for the shortest loan term you can comfortably manage within your budget.

Navigating the Car Loan Application Process

Successfully securing a car loan with a favorable interest rate requires more than just understanding the numbers; it also involves efficiently navigating the application process and avoiding common pitfalls.

Required Documentation and Information

When applying for a car loan, lenders will require specific documentation to verify your identity, income, and financial stability. Be prepared to provide:

- Proof of identity: Government-issued ID (driver’s license, passport).

- Proof of income: Recent pay stubs, tax returns, or bank statements.

- Proof of residency: Utility bills or lease agreements.

- Social Security Number: For a credit check.

- Vehicle information: If you’ve already chosen a car (make, model, VIN, purchase price).

Having these documents organized and ready can significantly expedite the application process.

Pre-approval vs. Dealership Financing

As mentioned earlier, getting pre-approved for a loan from an external lender (bank, credit union, online lender) before visiting a dealership is a highly recommended strategy. Pre-approval gives you a firm offer of credit, including an interest rate and maximum loan amount, allowing you to shop for a car with confidence and negotiate from a position of strength.

While dealerships also offer financing, known as dealership financing, they often act as intermediaries, connecting you with various lenders. While convenient, their primary goal is to sell cars, and their financing terms might not always be the most competitive initially. However, if you have a strong pre-approval in hand, the dealership’s finance manager might be motivated to find you an even better deal to secure the sale. The key is to compare the dealership’s offer (APR, term, total cost) against your pre-approval.

Avoiding Common Pitfalls

Several common mistakes can lead to higher interest rates or less favorable loan terms:

- Focusing solely on the monthly payment: This can lead to longer terms and higher total costs. Always consider the APR and total interest paid.

- Not shopping around: Accepting the first loan offer without comparison shopping can mean missing out on better rates.

- Negotiating trade-in and purchase price simultaneously: Negotiate the car’s price first, then the trade-in, and finally the financing. Mixing them can obscure the true cost of each component.

- Ignoring your credit report: Not addressing errors or improving your score before applying.

- Adding unnecessary extras to the loan: Resist pressure to roll warranties, service contracts, or other add-ons into your loan, as this increases the principal and thus the interest you pay.

By being diligent and informed, car buyers can navigate the financing landscape successfully, securing a loan that fits their budget and minimizes their long-term financial outlay. Understanding “what is the interest rate for a car” is not just about a single percentage, but about comprehending a complex financial instrument that underpins one of life’s significant purchases.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.