Navigating the complexities of the internal revenue system can be a daunting task, particularly when dealing with previous tax years. Filing your 2022 taxes—whether you are doing so as a late filer, an individual seeking an overdue refund, or a business owner rectifying past accounts—requires a meticulous approach to documentation and a deep understanding of the specific regulations that governed that fiscal period. The 2022 tax year was characterized by a return to “normalcy” following the expiration of many pandemic-era stimulus measures, yet it introduced new inflationary adjustments and updated credit requirements that remain vital for taxpayers to understand today.

Effective financial management is predicated on accurate tax reporting. This guide provides an in-depth exploration of the 2022 tax landscape, offering professional insights into deductions, credits, and the procedural mechanics required to ensure your filings are both compliant and optimized for your financial health.

Navigating the 2022 Tax Landscape and Inflationary Shifts

The 2022 tax year was significant because it marked the first major adjustment period for tax brackets following a surge in global inflation. For the taxpayer, this meant that the IRS adjusted many provisions to prevent “bracket creep,” a phenomenon where inflation pushes taxpayers into higher income tax brackets even though their actual purchasing power has not increased.

Understanding Tax Brackets and Standard Deductions

For 2022, the tax brackets remained at 10%, 12%, 22%, 24%, 32%, 35%, and 37%. However, the income thresholds for these brackets were widened. For instance, the top 37% rate applied to individual taxpayers with incomes greater than $539,900 ($647,850 for married couples filing jointly). Understanding where your 2022 income fell is the first step in calculating your base liability.

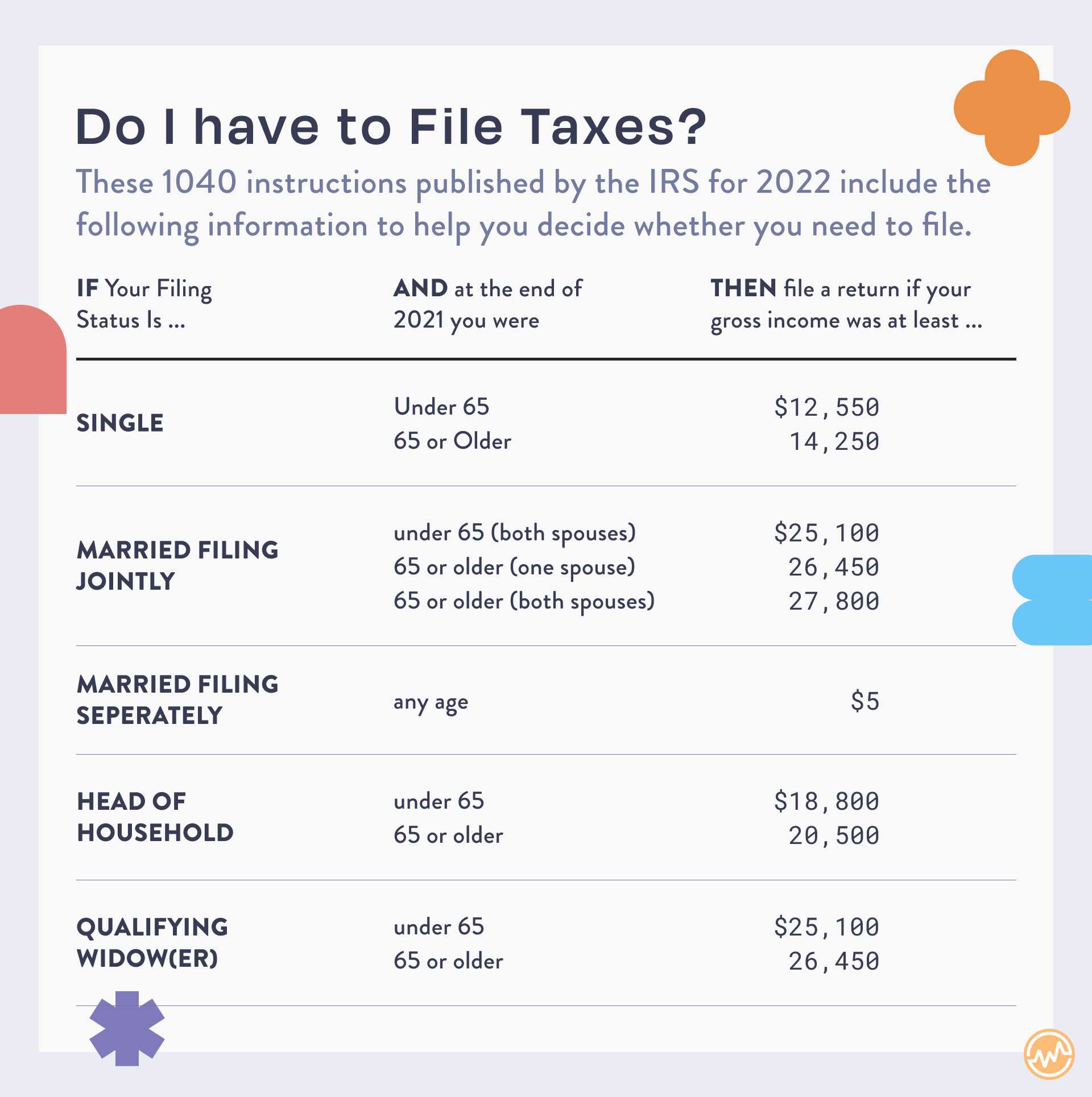

Furthermore, the standard deduction saw a notable increase. For 2022, the standard deduction was set at $12,950 for single filers and $25,900 for married filing jointly. This increase meant that more taxpayers found it financially advantageous to take the standard deduction rather than itemizing their expenses, simplifying the filing process for millions of households while still reducing their overall taxable income.

The Expiration of Pandemic-Era Provisions

A critical aspect of the 2022 filing season was the sunsetting of various provisions from the American Rescue Plan Act. Unlike the 2021 tax year, there were no third-round stimulus checks (Economic Impact Payments) to report, and the temporary expansion of certain credits—such as the Child Tax Credit—reverted to previous levels. Recognizing these changes is essential for those who may be comparing their 2022 returns to their 2021 filings and wondering why their refunds or liabilities have shifted so significantly.

Essential Documentation and Income Reporting Requirements

Precision in personal finance begins with the collection of data. To file a 2022 return accurately, you must reconstruct your financial life for that specific 12-month period. Discrepancies between what you report and what the IRS has on file via third-party reporting are the primary triggers for audits and “math error” notices.

Comprehensive Income Documentation: W-2s and 1099s

The foundation of your 2022 tax return is your income documentation. This includes Form W-2 for salaried employees and the 1099 series for independent contractors, freelancers, and investors.

- Form 1099-NEC: This is used for non-employee compensation. If you performed side work or ran a small business in 2022, this is a critical document.

- Form 1099-INT and 1099-DIV: These report interest and dividend income. With interest rates beginning to rise in late 2022, many taxpayers saw a slight uptick in taxable interest from high-yield savings accounts.

- Form 1099-K: While the IRS delayed the $600 reporting threshold for third-party payment processors (like Venmo or PayPal), many users still received these forms if they met the older, higher thresholds.

Reporting Digital Assets and Cryptocurrency

The 2022 tax year continued the IRS’s aggressive stance on digital assets. The question regarding “digital assets” remained on the front page of Form 1040. Taxpayers were required to answer “Yes” if they received, sold, exchanged, or otherwise disposed of any digital asset. For those who engaged in crypto trading during the 2022 market volatility, calculating capital gains and losses is a complex but necessary task. Accurate reporting requires a detailed log of every transaction’s “cost basis” and the fair market value at the time of the trade or sale.

Maximizing Deductions and Credits for the 2022 Season

Tax credits and deductions are the most powerful tools in a taxpayer’s arsenal to lower their effective tax rate. While deductions lower the amount of income you are taxed on, credits provide a dollar-for-dollar reduction in the tax you owe.

The Reversion of the Child Tax Credit (CTC)

For the 2022 tax year, the Child Tax Credit returned to $2,000 per qualifying child under the age of 17. This was a significant decrease from the enhanced $3,000 or $3,600 amounts seen in 2021. Additionally, the credit became only partially refundable. For families filing their 2022 taxes late, it is vital to ensure that the residency and dependency tests are strictly met to avoid delays in processing.

Education Credits: AOTC and Lifetime Learning Credit

Education remains a high priority in the tax code. The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) remained available in 2022 for taxpayers paying tuition for higher education. The AOTC allows for a maximum credit of $2,500 per eligible student, while the LLC provides up to $2,000 per tax return. These credits are particularly beneficial for adult learners or those pursuing side-hustle certifications to increase their earning potential.

Itemizing in 2022: Charitable Contributions and Mortgage Interest

For those whose expenses exceeded the standard deduction, itemizing on Schedule A remained an option.

- Mortgage Interest: Taxpayers could deduct interest on up to $750,000 of mortgage debt.

- State and Local Taxes (SALT): The deduction for state and local taxes remained capped at $10,000.

- Charitable Giving: In 2022, the “above-the-line” deduction for charitable contributions (which allowed non-itemizers to deduct up to $300) expired. This means only those who itemized could claim their 2022 donations.

Strategizing Filing Methods and Professional Tools

How you file is often as important as what you file. In the modern financial era, leveraging technology is the most efficient way to ensure accuracy and speed up the processing of your return.

Digital Filing vs. Paper Returns

The IRS strongly encourages e-filing. For the 2022 tax year, e-filing combined with direct deposit remains the fastest way to receive a refund. However, if you are filing 2022 taxes significantly late (for instance, filing them now in 2024), you may find that some consumer-grade software no longer supports electronic submission for that specific year, necessitating a paper filing. In such cases, using certified mail with a return receipt is a best practice for financial record-keeping.

Utilizing IRS Free File and Tax Software

For individuals with an Adjusted Gross Income (AGI) of $73,000 or less in 2022, IRS Free File provided access to brand-name software at no cost. For those above that threshold, professional-grade software like TurboTax, H&R Block, or TaxSlayer offers “prior-year” packages. These tools are invaluable because they automatically calculate the specific 2022 limitations and phase-outs, reducing the margin for human error.

The Value of Professional Tax Advice

For business owners, high-net-worth individuals, or those with complex investment portfolios (including K-1s from partnerships), consulting a Certified Public Accountant (CPA) or an Enrolled Agent (EA) is highly recommended. A professional can provide a “holistic” view of your 2022 finances, identifying missed opportunities for carry-forward losses or specialized business deductions that software might overlook.

Managing Late Filings, Penalties, and Refunds

If you are filing your 2022 taxes after the original April 2023 deadline (or the October extension), you must be prepared for the financial implications of a late return.

Understanding Penalties and Interest

If you owe taxes for 2022, the IRS charges two primary penalties: the “failure-to-file” penalty and the “failure-to-pay” penalty. The failure-to-file penalty is generally much higher—5% of the unpaid taxes for each month or part of a month that a tax return is late. If you are owed a refund, however, there is generally no penalty for filing late, but you must file within three years of the original deadline to claim that refund. For the 2022 tax year, that deadline is typically April 15, 2026.

Amending a Previously Filed 2022 Return

If you already filed your 2022 taxes but realized you missed a deduction or failed to report income, you must file Form 1040-X, Amended U.S. Individual Income Tax Return. This is a critical tool for maintaining financial integrity. Whether it is correcting an error in your favor or correcting a mistake that would otherwise lead to an audit, the amendment process allows you to keep your financial records transparent and accurate.

Tracking and Managing Your Refund

Once your 2022 return is processed, you can track the status using the “Where’s My Refund?” tool on the IRS website. For prior-year returns, processing can sometimes take longer than the standard 21-day window for current-year e-filed returns. Maintaining patience and keeping a digital copy of your submitted return is essential for your long-term financial archives.

In conclusion, filing 2022 taxes is a task that requires a blend of historical awareness and technical precision. By understanding the specific brackets, credits, and reporting requirements of that year, you can navigate the process with confidence, ensuring your personal or business finances remain on a solid, compliant foundation. Whether you are catching up on past obligations or refining your current financial strategy, a thorough approach to the 2022 tax year is a hallmark of sound fiscal responsibility.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.