For the modern consumer, the question “How much is a new Tesla?” is rarely answered with a single figure. In the volatile landscape of the electric vehicle (EV) market, pricing is a moving target influenced by supply chain dynamics, federal policy changes, and aggressive corporate pricing strategies. To understand the financial commitment of owning a Tesla, one must look beyond the sticker price and analyze the broader economic ecosystem of the brand.

From the entry-level Model 3 to the flagship Model X, purchasing a Tesla is not just a lifestyle choice; it is a significant financial maneuver. This guide breaks down the current pricing structures, the impact of federal incentives, and the long-term total cost of ownership to determine whether a Tesla remains a sound investment in today’s economy.

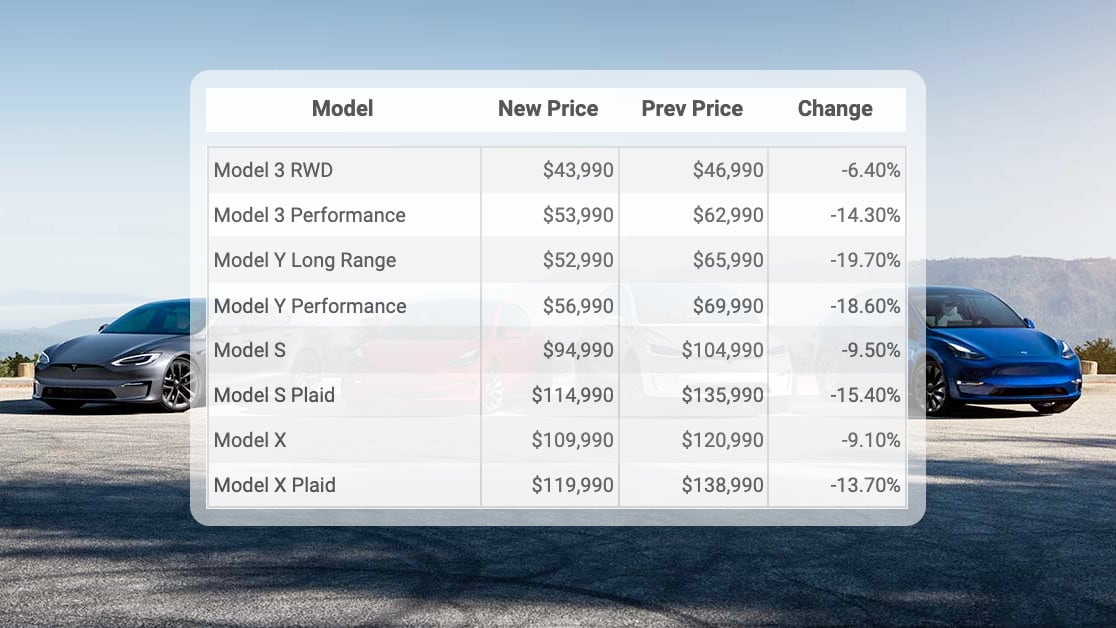

Decoding the Sticker Price: MSRP Breakdown Across the Tesla Lineup

The most immediate answer to the cost of a Tesla lies in the Manufacturer’s Suggested Retail Price (MSRP). However, Tesla operates on a direct-to-consumer model, meaning prices can fluctuate overnight without the buffer of traditional dealership negotiations.

Entry-Level Accessibility: The Model 3 and Model Y

The Model 3 and Model Y represent the “affordable” tier of the Tesla ecosystem. As of 2024, the Model 3—a sleek, rear-wheel-drive sedan—typically starts in the high $30,000 to low $40,000 range. It remains the gateway for those looking to exit the internal combustion engine (ICE) market without a six-figure commitment.

The Model Y, which has recently become one of the best-selling vehicles globally, commands a slight premium over the Model 3, usually starting in the mid-to-high $40,000s. Its status as a compact SUV makes it a more versatile asset for families, which often translates to higher resale demand—a critical factor for the finance-conscious buyer.

High-End Investment: The Model S and Model X

For the affluent investor or the tech-forward executive, the “Legacy” models—the Model S and Model X—represent a different tier of capital expenditure. The Model S, Tesla’s flagship sedan, generally starts in the mid $70,000s, with the high-performance “Plaid” variant easily clearing $90,000.

The Model X, known for its falcon-wing doors and increased towing capacity, sits at the top of the pricing pyramid. Starting in the low $80,000s, it competes directly with luxury European SUVs. From a financial perspective, these vehicles experience different depreciation curves than the mass-market models, often serving as a statement of corporate success rather than simple utility.

The Cybertruck Factor: Pricing in a New Category

The introduction of the Cybertruck has added a layer of complexity to Tesla’s pricing strategy. With various configurations ranging from the Rear-Wheel Drive (slated for future release) to the “Cyberbeast,” prices range from approximately $60,000 to well over $100,000. Because the Cybertruck occupies a niche market—part utility vehicle, part collectible—its current financial valuation is heavily influenced by “early adopter” premiums and limited initial supply.

Federal Incentives and Tax Credits: Navigating the EV Subsidy Landscape

One cannot accurately calculate the cost of a new Tesla without accounting for the significant “invisible” discounts provided by the government. These incentives are designed to lower the barrier to entry for EVs, but they come with strict financial eligibility criteria.

Understanding the Inflation Reduction Act (IRA)

Under the current federal guidelines in the United States, certain Tesla models qualify for a Clean Vehicle Tax Credit of up to $7,500. This is not a guaranteed discount; it is a strategic financial tool. To qualify, the vehicle must meet specific MSRP caps—currently $55,000 for sedans (Model 3) and $80,000 for SUVs and trucks (Model Y, Model X).

Furthermore, the “Point-of-Sale” credit now allows buyers to transfer the credit to the dealer (or in this case, Tesla) at the time of purchase, effectively reducing the down payment or the total amount financed. This provides immediate liquidity to the buyer, rather than forcing them to wait for a tax refund the following year.

State-Level Incentives and Hidden Rebates

Beyond federal aid, savvy buyers look to state-level programs. States like California, Colorado, and Massachusetts offer additional rebates that can range from $1,500 to $5,000. Some utility companies also provide “smart charging” rebates or discounted overnight electricity rates. When combined with federal credits, the effective price of a $45,000 Model Y can drop into the mid-$30,000s, making it competitively priced against a gas-powered Honda CR-V or Toyota RAV4.

Beyond the Purchase Price: Total Cost of Ownership (TCO)

The true financial profile of a Tesla is revealed in its “Total Cost of Ownership” (TCO) over a five-year period. In the world of personal finance, the initial purchase price is merely the “entry fee”; the operational savings are where the real wealth preservation occurs.

Charging Infrastructure vs. Traditional Fuel Costs

The most significant financial advantage of owning a Tesla is the decoupling from global oil price volatility. On average, charging a Tesla at home costs significantly less per mile than refueling a gasoline vehicle. For example, if the average cost of electricity is $0.16 per kWh, a Model 3 might cost about $0.04 per mile to operate, whereas a 30-mpg gasoline car at $3.50 per gallon costs roughly $0.12 per mile. Over 100,000 miles, this represents a $8,000 saving in fuel alone.

Maintenance and Insurance Premiums

Tesla vehicles have fewer moving parts than ICE vehicles—no oil changes, spark plugs, or transmission flushes. This significantly reduces long-term maintenance budgets. However, from a financial planning perspective, one must account for the “Tesla Premium” in insurance.

Because Teslas are high-tech machines with specialized aluminum frames and proprietary sensors, they can be more expensive to repair after an accident. Insurance companies often charge higher premiums for Teslas compared to traditional luxury cars. Prospective owners must balance the $0 oil change against a potentially $50-per-month increase in insurance premiums.

Financing and Leasing Strategies for the Modern Investor

How you pay for a Tesla is just as important as how much you pay. With fluctuating interest rates, the decision between a cash purchase, financing, or leasing requires a deep dive into opportunity costs.

Direct Purchase vs. Lease: Which Makes Financial Sense?

For many years, leasing a Tesla was considered a poor financial move because the company did not allow lessees to buy out the car at the end of the term. However, leasing has become more attractive as a hedge against rapid technological obsolescence. If battery technology takes a massive leap forward in the next three years, a person who leased a Model 3 is protected from the resulting drop in resale value of older battery tech.

Conversely, financing through a credit union often yields the lowest APR, allowing the buyer to build equity in an asset that, historically, has held its value better than many other luxury brands—though this trend has stabilized recently.

Resale Value and Depreciation Curves

Depreciation is the largest “hidden” cost of any vehicle. Tesla’s aggressive price cuts in late 2023 and early 2024 have impacted the used market, causing a steeper-than-normal depreciation curve for those who bought at the “peak.” For a new buyer today, the lower MSRP provides a safer entry point, but it is vital to view the vehicle as a depreciating utility asset rather than a speculative investment.

The Long-Term ROI: Is a Tesla a Sound Financial Decision?

To conclude the financial analysis of a new Tesla, one must evaluate the Return on Investment (ROI) from a holistic perspective. A Tesla is a high-cap-ex purchase that offers low op-ex (operating expenses).

For a commuter driving 15,000 miles or more per year, the “break-even” point—where the savings in fuel and maintenance offset the higher initial purchase price and insurance—usually occurs between years three and five. For a low-mileage driver, the financial justification is harder to make based on savings alone; in that case, the purchase is more of a luxury expenditure than a financial optimization.

Ultimately, the cost of a new Tesla is a sum of its MSRP, minus federal and state incentives, plus the adjusted cost of insurance and home charging installation. In the current market, with prices more competitive than ever and tax credits available at the point of sale, the Tesla lineup offers a compelling financial case for those looking to transition into the next era of personal transportation. By treating the purchase as a multi-year financial strategy rather than a simple transaction, consumers can maximize their capital and enjoy the benefits of one of the most technologically advanced assets on the road today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.