In the current landscape of financial technology, the phrase “Venmo me” has transitioned from a niche colloquialism to a standard operational command for peer-to-peer (P2P) transactions. As a subsidiary of PayPal, Venmo has redefined the user experience of digital transfers, blending social connectivity with robust software architecture. However, for a new user or a professional looking to optimize their digital workflow, the platform offers more than just a simple “send” button. Understanding how to use Venmo effectively requires a deep dive into its technical setup, security protocols, and the nuances of its social-digital interface.

Getting Started: The Architecture of the Venmo Application

The journey into Venmo begins with its installation and the foundational setup of your digital profile. Unlike traditional banking apps that often prioritize a utilitarian interface, Venmo is built on a framework that emphasizes speed and accessibility.

Installation and Initial Configuration

The Venmo application is available for both iOS and Android platforms, designed to leverage the native security features of these operating systems. Upon downloading the app, the first technical hurdle is identity verification. In compliance with federal regulations—specifically the USA PATRIOT Act—Venmo requires a verified identity to utilize the full spectrum of its features. Users must input their legal name, date of birth, and Social Security number. This data is encrypted using 256-bit encryption, ensuring that the initial handshake between the user and the server remains secure.

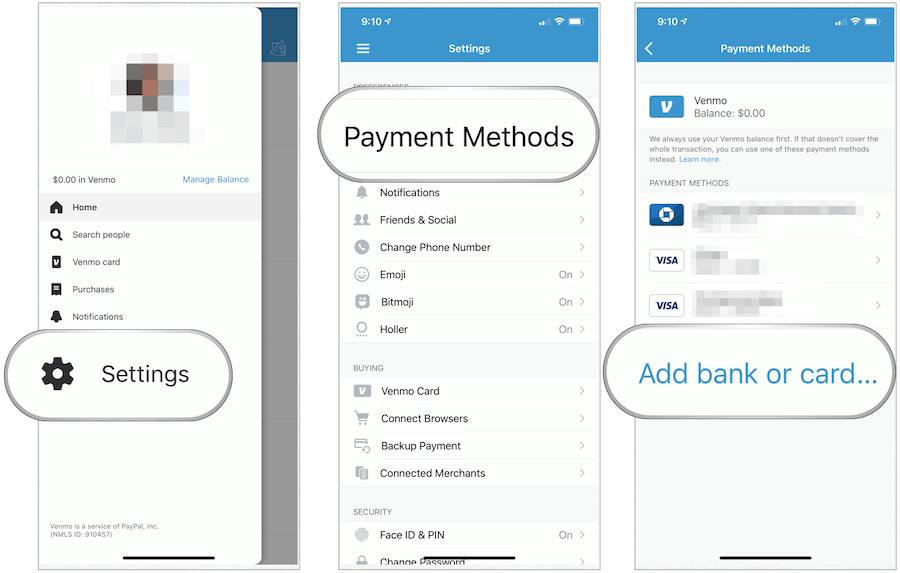

Linking Financial Protocols and Bank Integration

Once the profile is established, the software acts as a bridge between your traditional bank account and the digital economy. Users have two primary ways to link funds: via a debit/credit card or a direct bank account connection. For the latter, Venmo often utilizes third-party APIs like Plaid, which allows for a secure, credential-less login to your banking portal. This technical integration minimizes the manual entry of routing and account numbers, reducing the risk of human error during the setup of the Electronic Funds Transfer (EFT) pipeline.

Executing Transactions: The Mechanics of P2P Transfers

At its core, Venmo is a ledger-based system. When you “Venmo” someone, you are initiating a request to the platform to update its internal database, moving a balance from one digital bucket to another.

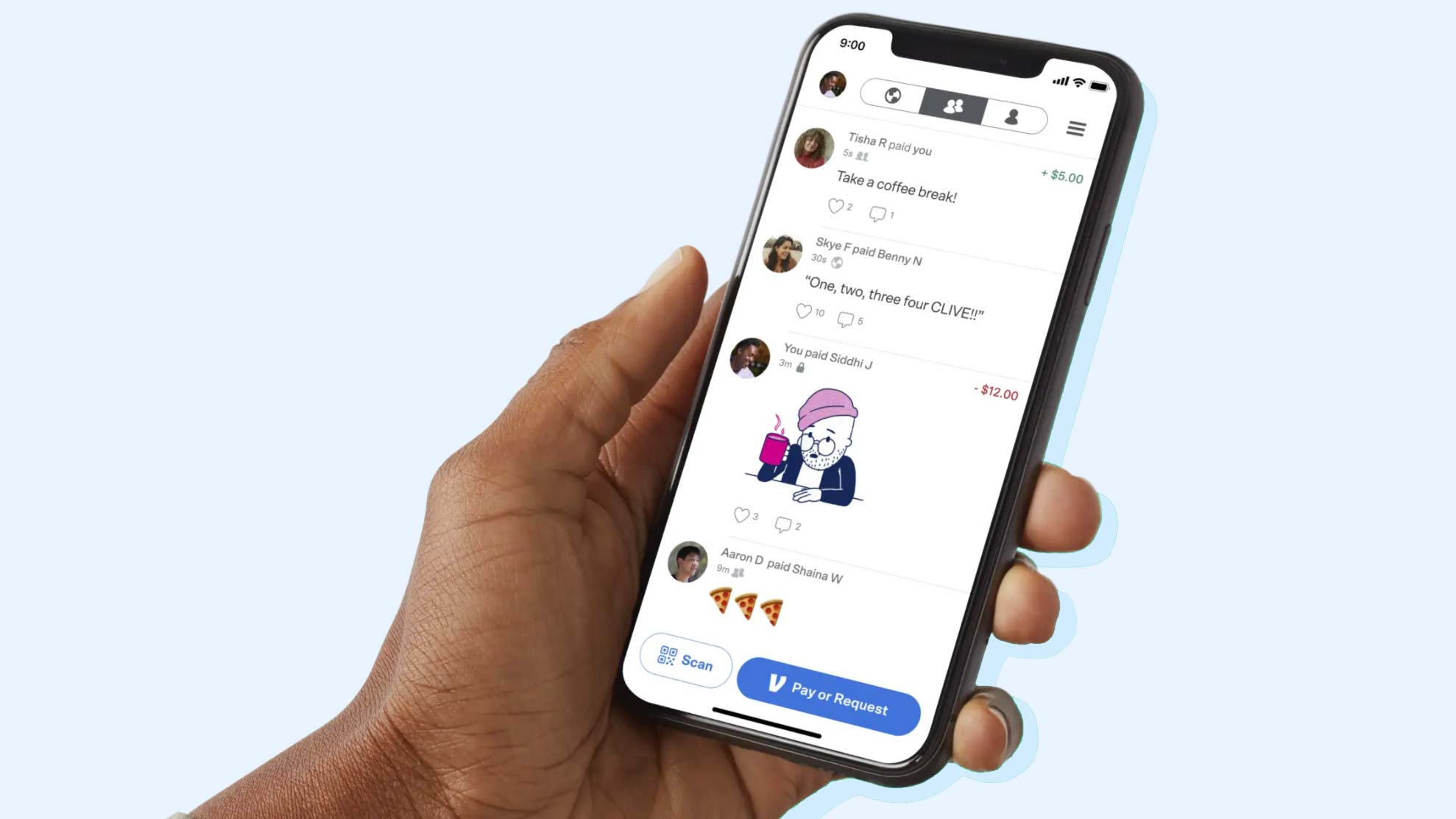

Navigating the User Interface for Payments and Requests

The primary interface of Venmo is designed for high-speed navigation. The “Pay or Request” button is the central node of the app. To initiate a transaction, a user must specify a recipient. The app offers several technical solutions for this: searching by a unique username (the @handle), synchronizing phone contacts via API, or scanning a personalized QR code. Once the recipient is identified, the user enters the amount and a mandatory note. This note is more than a social nicety; it serves as a metadata tag for the transaction, allowing users to search and categorize their digital spending history later.

Leveraging QR Code Technology for Instant Connectivity

One of the most efficient technical features within Venmo is the integrated QR code scanner. This removes the “search friction” associated with common names. Each Venmo account generates a unique QR code—essentially a visual representation of a deep link to that user’s profile. In a professional or high-traffic environment, scanning a QR code ensures that the transaction is directed to the correct cryptographic address, eliminating the risk of sending funds to the wrong individual.

Security and Privacy: Safeguarding the Digital Ledger

As a piece of financial software, Venmo is a prime target for digital threats. Consequently, its technical suite includes several layers of defense designed to protect both the user’s funds and their personal data.

Multi-Factor Authentication and Biometric Security

The first line of defense in the Venmo app is its integration with mobile hardware security. Users are encouraged to enable biometric authentication, such as FaceID or TouchID. From a technical standpoint, this ensures that the private keys to the wallet are only accessible via a unique biological signature. Furthermore, Venmo employs Multi-Factor Authentication (MFA). If a login attempt is detected from an unrecognized IP address or device, the software triggers a verification code sent via SMS or email, acting as a secondary gatekeeper against unauthorized access.

Managing Privacy Architecture and Social Visibility

Venmo’s unique selling point—its social feed—is also its most debated technical feature. Every transaction has a visibility setting: Public, Friends, or Private.

- Public: The transaction is visible to the entire Venmo network.

- Friends: Visible only to the sender’s and recipient’s contact list.

- Private: Only the participants can see the record.

Navigating these settings is crucial for digital hygiene. By accessing the “Privacy” sub-menu in the settings, users can retroactively change the visibility of past transactions and set a global default for future ones. For the security-conscious user, shifting the architecture to “Private” is the recommended protocol to prevent social engineering attacks based on spending habits.

Advanced Features: From Business Profiles to Cryptocurrency

As the fintech landscape evolves, Venmo has expanded its software capabilities beyond simple personal transfers, incorporating tools for professionals and digital asset enthusiasts.

Venmo for Business and Professional Interfaces

For freelancers and small business owners, Venmo offers a specialized “Business Profile.” Technically, this functions as a separate sub-account linked to the primary identity. It provides advanced reporting tools, automated tax documentation (such as 1099-K generation), and a different fee structure for “Goods and Services” transactions. This distinction is vital for maintaining a clean audit trail between personal and professional digital assets.

Integration of Digital Assets and Crypto-Wallets

In recent updates, Venmo has integrated a cryptocurrency module, allowing users to buy, sell, and hold assets like Bitcoin and Ethereum directly within the app. This feature utilizes a “custodial wallet” model, where Venmo (via its parent company) manages the private keys on behalf of the user. While this simplifies the user experience for those unfamiliar with blockchain technology, it also requires users to understand the specific risks associated with digital asset volatility and the technical limitations of a custodial system.

Troubleshooting and Optimizing App Performance

Even the most robust software can encounter latency issues or synchronization errors. Understanding the technical triggers for these problems can help users resolve them without significant downtime.

Resolving Connection Errors and Verification Lag

Occasionally, a user may encounter a “Payment Declined” or “Verification Pending” status. This is often not a bank issue but a security trigger within Venmo’s fraud-detection algorithms. If a user’s behavioral patterns—such as a sudden high-value transfer or a change in geographical location—deviate from the norm, the software’s AI may pause the transaction for manual review. Ensuring that the app is updated to the latest version and that the device’s GPS services are active can help the software verify the legitimacy of the transaction.

Best Practices for Digital Hygiene and Maintenance

To keep the Venmo application running at peak performance, users should periodically perform “digital hygiene.” This includes auditing the list of “Connected Apps”—third-party services that may have requested access to your Venmo data—and clearing the app’s cache if the interface becomes sluggish. Furthermore, users should regularly review their “Session Management” settings to see which devices are currently logged into their account, terminating any old or unrecognized sessions to maintain the integrity of their digital wallet.

By viewing Venmo not just as a tool for splitting a dinner bill, but as a sophisticated piece of financial software, users can leverage its full potential while minimizing risks. Whether you are managing personal transfers, running a small business profile, or exploring the world of cryptocurrency, mastering the technical nuances of the Venmo ecosystem is an essential skill in the modern digital age.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.