For millions of Americans, Social Security represents the cornerstone of a stable retirement. It is the only source of inflation-protected, guaranteed lifetime income that most workers will ever receive. However, despite its importance, the mechanics behind how the Social Security Administration (SSA) determines your monthly check are often shrouded in complexity. Determining your benefits is not merely a matter of waiting until you reach a certain age; it is a calculated process involving your earnings history, the timing of your claim, and your marital status.

Understanding these variables is essential for effective personal finance management. Whether you are decades away from retirement or currently weighing your filing options, mastering the logic of Social Security allows you to integrate this federal benefit into a broader wealth-management strategy.

Understanding the Foundation: How the SSA Calculates Your Primary Insurance Amount (PIA)

The journey to determining your benefit begins with your “Primary Insurance Amount” or PIA. This is the base amount you are entitled to receive if you file exactly at your Full Retirement Age (FRA). The SSA uses a specific formula to convert a lifetime of work into a single monthly figure.

The Role of Work Credits

To even qualify for Social Security retirement benefits, you must first earn enough “credits.” As of 2024, you earn one credit for every $1,730 in covered earnings, up to a maximum of four credits per year. To be “fully insured,” most workers need 40 credits, which typically equates to ten years of work. While these credits determine eligibility, they do not determine the actual dollar amount of your check; that is reserved for your actual earnings history.

Identifying Your Highest 35 Years of Earnings

The SSA looks at your entire work history but focuses only on your top 35 years of indexed earnings. “Indexing” is a crucial concept; the SSA adjusts your historical earnings to account for changes in average wages over time, ensuring that the $15,000 you earned in 1985 is weighted fairly against what you earn today.

If you have worked for more than 35 years, the SSA drops the lowest-earning years. Conversely, if you have worked for fewer than 35 years, the SSA averages in “zeros” for the remaining years. This is a critical point for personal finance planning: working even part-time for a few extra years to replace those “zero” years can significantly boost your final benefit amount.

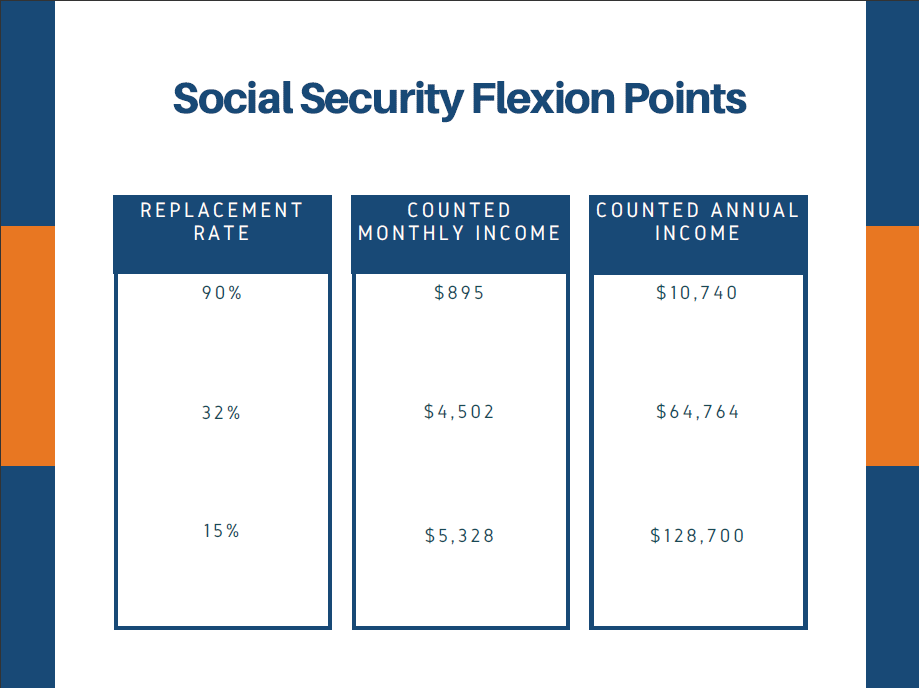

From AIME to PIA: The Formula Explained

Once your top 35 years are indexed and averaged, the SSA determines your Average Indexed Monthly Earnings (AIME). They then apply a formula using “bend points” to calculate your PIA. This formula is progressive; it replaces a higher percentage of income for lower-wage earners than for higher-wage earners. For example, the formula might replace 90% of the first few hundred dollars of your AIME, but only 15% of the earnings above a certain threshold. This ensures a social safety net while still rewarding those who paid more into the system.

Timing Your Claim: The Impact of Early Retirement vs. Delayed Credits

Once you know your PIA, the next step in determining your actual benefit is deciding when to claim it. While your PIA is fixed based on your earnings, the amount you actually receive is heavily modified by your age at the time of application.

Filing at Age 62: The Reduction Penalty

You can begin taking Social Security as early as age 62, but doing so comes at a permanent cost. If your Full Retirement Age is 67 (which it is for everyone born in 1960 or later) and you claim at 62, your monthly benefit is reduced by approximately 30%. This reduction is actuarial; because you are expected to receive checks for a longer period, each check is smaller. For those who do not have pressing health concerns or immediate liquidity needs, filing at 62 often results in significantly less lifetime wealth.

Reaching Full Retirement Age (FRA)

Your FRA is the point at which you receive exactly 100% of your PIA. For those born between 1943 and 1954, the FRA was 66. It gradually increases for those born later, topping out at 67. Navigating the FRA is vital because it is also the point at which the “earnings test” disappears. If you claim benefits before your FRA and continue to work, the SSA may withhold a portion of your benefits if you earn above a certain limit. Once you hit your FRA, you can earn an unlimited amount without any reduction in benefits.

Maximizing Benefits with Delayed Retirement Credits

For every year you delay claiming Social Security past your FRA, your benefit increases by 8% in simple interest, up until age 70. This means that by waiting from age 67 to age 70, you can increase your monthly check by 24%. In the world of personal finance, a guaranteed 8% annual return is virtually unheard of in any other low-risk investment vehicle. Consequently, for individuals in good health with other retirement assets to draw upon, delaying until age 70 is often the most effective strategy for maximizing “longevity insurance.”

Strategic Variables: Spousal, Survivor, and Disability Considerations

Determining your benefit is not always a solo endeavor. Social Security is designed to protect families, meaning your benefit may be influenced by your current or former marriage.

Spousal Benefits and the 50% Rule

If you are married, you may be eligible for a spousal benefit. This allows a lower-earning spouse to receive up to 50% of the higher-earning spouse’s PIA. The SSA automatically calculates whether your own earned benefit or the spousal benefit is higher and pays you the larger amount. It is important to note that the higher-earning spouse must have already filed for their own benefits for the other spouse to claim the spousal portion.

Divorced Spouse Benefits

Many people are unaware that they can claim benefits based on an ex-spouse’s work record. If your marriage lasted at least ten years, you are currently unmarried, and you are age 62 or older, you may be eligible for benefits based on your ex-spouse’s record—even if they have remarried. Crucially, claiming on an ex-spouse’s record does not reduce the benefit that the ex-spouse (or their new partner) receives.

Survivor Benefits for Widows and Widowers

Survivor benefits represent a critical component of life insurance within the Social Security system. If a spouse dies, the survivor is generally eligible to inherit the deceased spouse’s full benefit amount if it is higher than their own. This is a primary reason why the higher-earning spouse is often encouraged to delay filing until age 70; doing so locks in the highest possible survivor benefit for the remaining spouse, providing a financial safety net for the later stages of life.

Tax Implications and the “Tax Torpedo”

A common misconception in personal finance is that Social Security benefits are tax-free. In reality, depending on your total income, a significant portion of your benefits may be subject to federal income tax.

Combined Income and Provisional Tax

The IRS uses a metric called “combined income” (also known as provisional income) to determine if your benefits are taxable. This is calculated by taking your Adjusted Gross Income (AGI), adding any tax-exempt interest (like municipal bond interest), and adding 50% of your Social Security benefits.

- If your combined income is between $25,000 and $34,000 (individual) or $32,000 and $44,000 (joint), you may pay tax on up to 50% of your benefits.

- If your combined income exceeds $34,000 (individual) or $44,000 (joint), up to 85% of your benefits may be taxable.

The “Tax Torpedo” Effect

In financial planning, the “tax torpedo” refers to the sharp increase in marginal tax rates that occurs when an extra dollar of IRA distributions causes another 85 cents of Social Security to become taxable. To avoid this, many retirees use strategic withdrawals from Roth IRAs (which do not count toward combined income) to keep their taxable income below the thresholds.

Tools and Resources for Accurate Benefit Estimation

While understanding the formulas is helpful, you do not have to do the math by hand. There are several professional-grade tools available to help you determine your benefits with precision.

The “my Social Security” Account

The most important first step for any worker is to create a “my Social Security” account at ssa.gov. This portal provides your official Social Security Statement, which lists your year-by-year earnings history. It is vital to review this for errors; if an employer failed to report your income correctly 20 years ago, your benefit will be lower than it should be. The statement also provides personalized estimates for your benefits at ages 62, FRA, and 70.

Using Online Calculators for Scenario Planning

While the SSA’s basic calculator is a good starting point, it often fails to account for complex scenarios like the “Windfall Elimination Provision” (for those with pensions from non-covered work) or complex spousal strategies. For a more robust analysis, tools like “Maximize My Social Security” or “NewRetirement” allow you to run “what-if” scenarios. These tools can help you determine the optimal “break-even” age—the point at which the total cumulative benefits of waiting until 70 surpass the total benefits received by starting at 62.

In conclusion, determining your Social Security benefits is a multifaceted process that requires a deep dive into your work history, an understanding of the federal formulas, and a strategic approach to timing. By viewing Social Security not as a static government check, but as a flexible financial asset, you can better position yourself for a secure and prosperous retirement. In the landscape of personal finance, knowledge of the Social Security system is one of the most valuable investments you can make.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.