The dream of a “soft retirement”—where one transitions from a high-stress career into a part-time role or a passion-driven side hustle while collecting a monthly Social Security check—is becoming the new standard for modern financial planning. However, the intersection of earned income and Social Security benefits is governed by a complex set of rules known as the “Social Security Earnings Test.”

For many, the central question is: “How much can I earn before the government starts taking back my benefits?” The answer depends entirely on your age and your progress toward what the Social Security Administration (SSA) calls your Full Retirement Age (FRA). Navigating these waters requires a firm grasp of personal finance metrics, tax implications, and long-term wealth preservation strategies.

Understanding the Social Security Earnings Test Mechanics

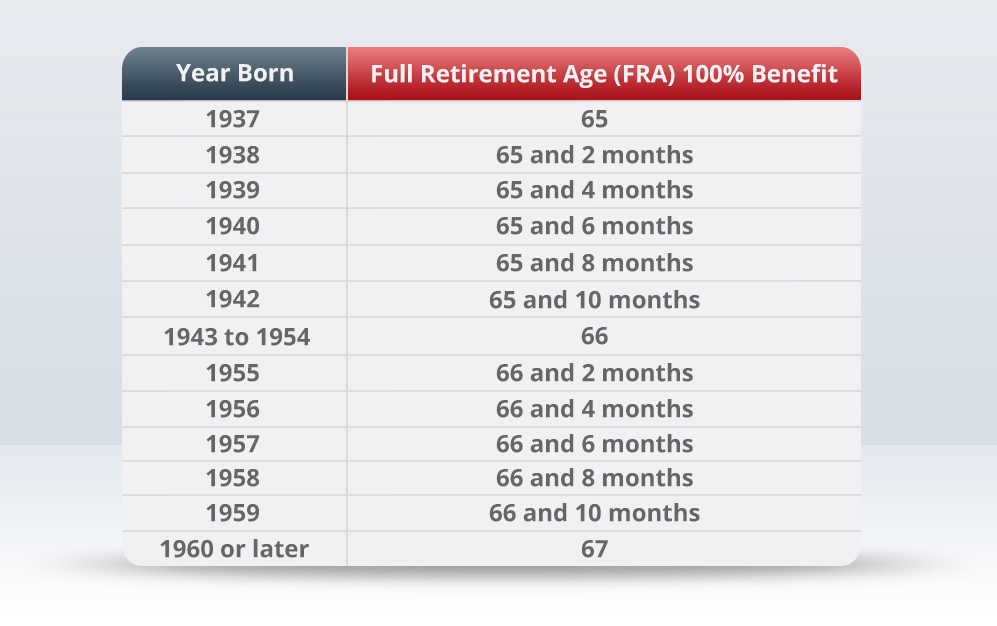

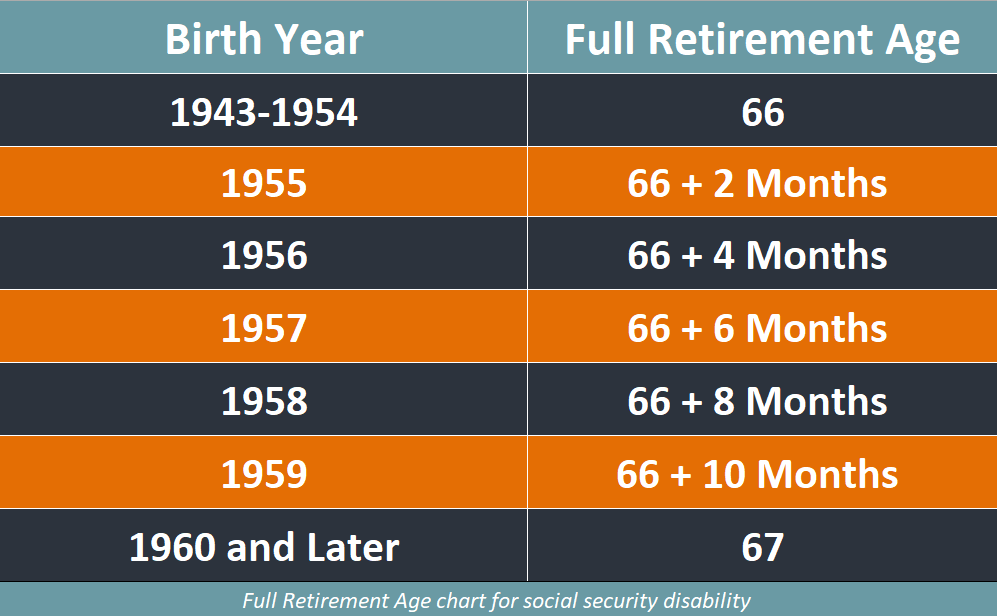

The most critical factor in determining how much you can earn while collecting Social Security is your age relative to your Full Retirement Age. For anyone born in 1960 or later, the FRA is 67. If you were born earlier, your FRA may be 66 and a specific number of months.

Working Before Reaching Full Retirement Age

If you choose to claim Social Security benefits early (anytime between age 62 and your FRA) and continue to work, the SSA applies a strict earnings limit. As of 2024, the annual earnings limit is $22,320.

If your earnings exceed this threshold, the SSA will withhold $1 in benefits for every $2 you earn over the limit. For example, if you earn $32,320 in a calendar year—exactly $10,000 over the limit—the SSA will withhold $5,000 of your Social Security benefits. For many middle-income earners, this “clawback” can significantly diminish the value of claiming benefits early.

The Year You Reach Full Retirement Age

The rules relax significantly during the specific calendar year you hit your FRA. During this year, a different, much higher limit applies. For 2024, the limit is $59,520. However, the SSA only counts the money you earn in the months before the month you reach FRA.

If you exceed this higher threshold, the withholding rate is also more favorable: the SSA withholds $1 for every $3 you earn above the limit. This transition period requires careful month-by-month accounting to ensure you aren’t inadvertently triggering a massive benefit withholding just as you reach your full retirement milestone.

Life After Full Retirement Age

The moment you reach the month of your Full Retirement Age, the earnings test disappears entirely. You can earn $1 million a year or $10,000 a year; your Social Security benefits will remain untouched regardless of your income. This is often the point where high-earners or business owners choose to finally flip the switch on their benefits, as there is no longer a financial “penalty” for continued productivity.

Defining “Earnings”: What Income Counts?

In the world of personal finance, not all dollars are created equal. When the SSA calculates your “earnings” for the earnings test, they are specifically looking at “earned income”—money derived from active labor.

Wages and Self-Employment Income

If you are an employee, the SSA looks at your gross wages (not your take-home pay). This includes bonuses, commissions, and overtime pay. If you are self-employed, they look at your net earnings from self-employment.

It is important to note that for the earnings test, the SSA counts your pay when it is earned, not when it is paid. If you performed a consulting project in December but weren’t paid until January of the following year, that income counts toward the December total. This nuance is vital for freelancers and contractors who may have lumpy income streams.

What Does Not Count as Earnings

One of the most common misconceptions in retirement planning is that all income triggers a benefit reduction. In reality, Social Security is designed to test your ability to work, not your overall wealth. The following types of income do not count toward the earnings limit:

- Pension payments: Income from a previous employer’s retirement plan.

- Investment income: Dividends, interest, and capital gains from brokerage accounts.

- IRA and 401(k) distributions: Taking money out of your retirement accounts does not affect your Social Security check.

- Annuity payments: Regular payments from a private insurance contract.

- Rental income: Profits from real estate holdings (unless you are a real estate professional).

By shifting your income strategy toward these “passive” or “deferred” sources, you can effectively bypass the earnings test and keep your full Social Security benefit.

The Long-Term Impact: Is the Money Gone Forever?

A common fear among retirees is that the money withheld by the SSA due to the earnings test is a “tax” or a permanent loss. From a professional financial perspective, it is more accurate to view it as a forced deferral.

Benefit Recalculation at Full Retirement Age

If the SSA withholds some of your benefits because you worked and earned over the limit, they don’t simply keep that money. Once you reach your Full Retirement Age, the SSA will “recalculate” your monthly benefit amount.

They do this by giving you credit for the months in which you did not receive a benefit because of your earnings. Essentially, the SSA treats you as if you retired a little bit later than you actually did. Over time, your monthly check increases to compensate for the months you “lost” earlier. While this doesn’t provide an immediate lump sum, it increases your “floor” of guaranteed income for the rest of your life.

The Taxability of Benefits (The “Tax Torpedo”)

While your benefits might not be permanently lost due to the earnings test, they may be reduced by Uncle Sam through taxation. This is known as the “provisional income” rule. If the sum of your adjusted gross income, tax-exempt interest, and half of your Social Security benefits exceeds $25,000 (for individuals) or $32,000 (for couples), up to 50% of your benefits become taxable. If you earn even more ($34,000 for individuals/$44,000 for couples), up to 85% of your benefits may be subject to federal income tax.

Working while collecting Social Security can push you into a higher tax bracket where a significant portion of your benefits is lost to taxes. This “tax torpedo” is a critical consideration for anyone planning to earn a high side-hustle income while drawing from the system.

Strategic Planning for the Working Retiree

Given the complexities of the earnings test and the tax implications, how should a savvy individual approach the decision to work and collect?

Minimizing the “Clawback” through Business Expenses

If you are a business owner or a 1099 contractor, you have a unique advantage. Since the SSA looks at “net earnings” for self-employed individuals, legitimate business expenses can be used to lower your reported income below the $22,320 threshold. Investing back into your business—buying new equipment, marketing, or upgrading software—can reduce your net profit, allowing you to keep more of your Social Security benefits while growing your enterprise.

Coordinating with Spousal Benefits

For married couples, the earnings test applies to each person individually. If one spouse is under FRA and working, only their benefits (and any benefits based on their record) are subject to withholding. The other spouse’s earnings do not affect the first spouse’s Social Security check. Financial planning for couples should involve a “coordinated claim” strategy, where the higher-earning spouse might delay benefits to avoid the earnings test, while the lower-earning spouse claims early if they are already under the income threshold.

The Special Monthly Rule

In the first year of retirement, many people have already earned more than the annual limit before they even apply for Social Security. To address this, the SSA offers a “special monthly rule.” This rule allows you to receive a full Social Security check for any whole month you are considered retired, regardless of your total yearly earnings. This is particularly useful for corporate executives who retire mid-year after earning a high salary but want to begin benefits immediately.

Conclusion: Balancing Labor and Leisure

The decision to earn income while collecting Social Security is not just a mathematical one; it is a strategic maneuver within your broader financial life. While the earnings test may seem like a deterrent, it is designed to ensure that Social Security remains a safety net for those who have truly exited the workforce.

If you are under your Full Retirement Age and plan to earn significantly more than the current $22,320 limit, it often makes more financial sense to delay claiming your benefits. Doing so avoids the benefit withholding, bypasses the “tax torpedo,” and allows your future monthly benefit to grow via “delayed retirement credits.” However, if your earnings are modest or if you have reached your FRA, working while collecting is one of the most effective ways to bolster your retirement portfolio and ensure long-term financial independence. In the end, the goal of any money-focused strategy should be to maximize the total value of your lifetime benefits while maintaining the lifestyle you worked so hard to achieve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.