In the realm of finance, numbers are the alphabet, but percentages are the grammar. Whether you are analyzing the performance of a diversified investment portfolio, calculating the impact of inflation on your purchasing power, or determining the tax implications of a capital gain, understanding how to find a percentage is a fundamental skill. Far from being a mere relic of high school mathematics, percentage calculation is a vital tool for anyone seeking to achieve financial independence and master business operations.

In this comprehensive guide, we will explore the practical applications of percentage calculations within the “Money” niche, providing you with the insights needed to navigate the complexities of personal finance, investing, and corporate accounting.

The Foundation of Financial Literacy: Understanding Basic Percentage Calculations

Before diving into complex financial modeling, one must master the basic mechanics of percentage. In the context of money, a percentage represents a portion of a whole, expressed in hundredths. This allows for a standardized comparison between different financial figures, regardless of their absolute scale.

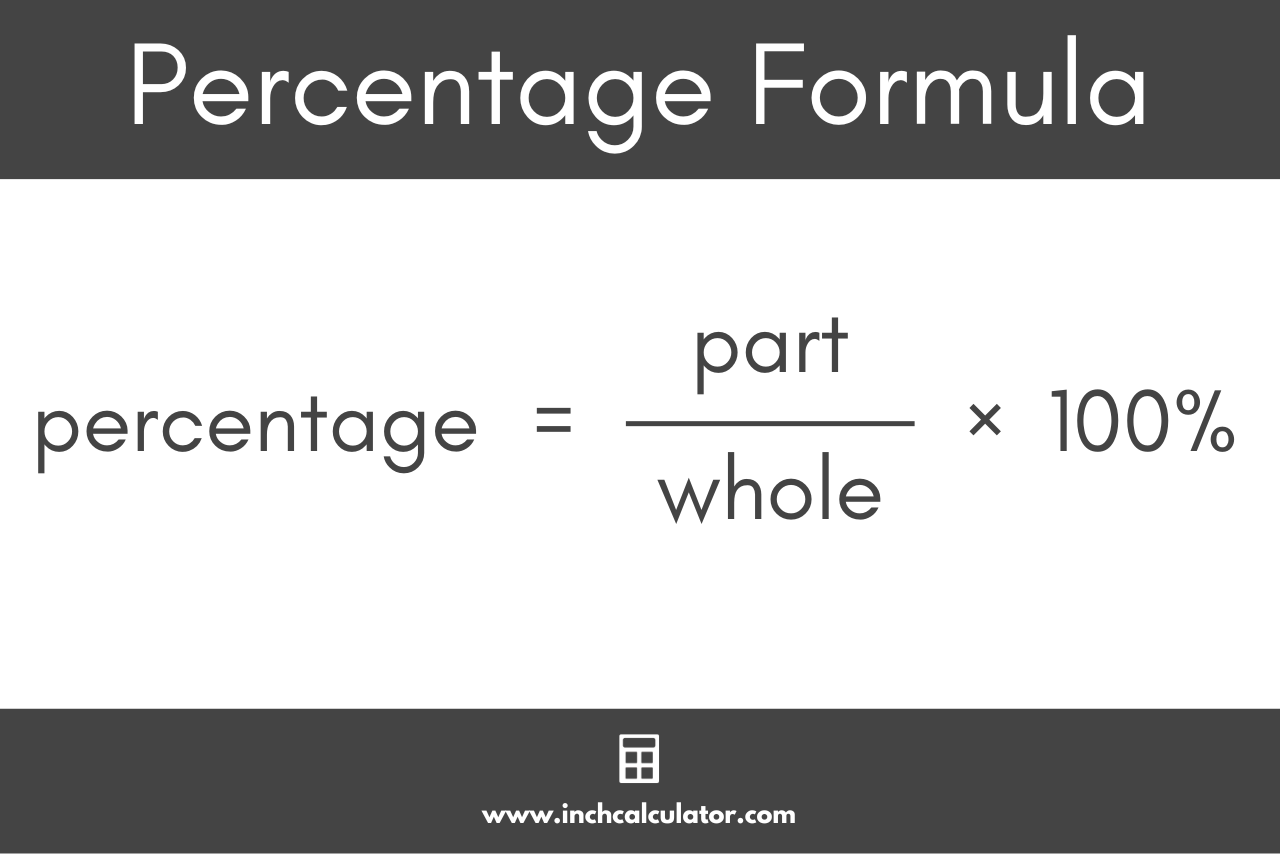

The Core Formula: Part over Whole

The most frequent calculation you will encounter is finding what percentage one number is of another. The formula is straightforward: (Part / Whole) × 100 = Percentage.

In personal finance, this is used for budgeting. For instance, if your monthly income is $5,000 and your rent is $1,500, you find the percentage of your income spent on housing by dividing 1,500 by 5,000, resulting in 0.30, or 30%. Financial advisors often recommend keeping this specific percentage below 30% to maintain a healthy financial profile.

Reverse Percentages: Finding the Original Value

Often in finance, you are presented with a final value and a percentage change, and you need to work backward to find the original amount. This is common when calculating “sales tax inclusive” prices or understanding a portfolio’s value before a market dip.

To find the original value after a percentage increase, the formula is: Final Value / (1 + Percentage Increase). If a stock is currently worth $110 after a 10% gain, you divide 110 by 1.10 to find the original purchase price of $100. Mastering these “reverse” calculations is essential for accurate auditing and tax preparation.

Maximizing Returns: Calculating Percentages in Investing and Portfolio Management

For the savvy investor, percentages are the primary metric for success. Absolute dollar gains are often misleading; a $1,000 profit is impressive on a $5,000 investment (20%) but mediocre on a $100,000 investment (1%).

Return on Investment (ROI) and Compound Growth

The most critical percentage in the world of money is the Return on Investment (ROI). This metric tells you how efficiently your capital is working for you. The formula is: [(Current Value – Original Value) / Original Value] × 100.

Understanding this calculation allows you to compare disparate asset classes. You can compare the 8% return on a mutual fund against the 4% yield of a high-interest savings account. Furthermore, understanding the “Percentage of Growth” is the gateway to understanding compounding. When your investments grow by a certain percentage, and that growth then earns its own percentage of growth in the following period, you leverage the most powerful force in finance.

Dividend Yields and Asset Allocation Percentages

Income-focused investors rely heavily on the “Dividend Yield” percentage. This is calculated by taking the annual dividend per share and dividing it by the current share price. A 4% dividend yield might be a primary reason to hold a specific utility stock during a volatile market.

Equally important is asset allocation—the percentage of your total wealth held in different categories (e.g., 60% stocks, 30% bonds, 10% cash). By calculating these percentages regularly, an investor can “rebalance” their portfolio, selling assets that have grown to represent too large a percentage and buying those that have shrunk, thereby adhering to the “buy low, sell high” mantra.

Navigating the Cost of Capital: Interest Rates and Debt Management

On the flip side of investing is debt. Whether it is a mortgage, a student loan, or credit card debt, the percentage—expressed as an interest rate—is the price you pay for using someone else’s money.

Annual Percentage Rate (APR) vs. Annual Percentage Yield (APY)

One of the most common points of confusion in personal finance is the difference between APR and APY. Both are percentages, but they serve different purposes.

The APR (Annual Percentage Rate) is the simple interest rate charged on a loan over a year. However, if you are looking at a savings account or a loan that compounds monthly, the APY (Annual Percentage Yield) is the more accurate figure. The APY takes into account the effect of compounding interest throughout the year. Knowing how to calculate and compare these two percentages can save a borrower thousands of dollars over the life of a mortgage or earn a saver significantly more in a CD (Certificate of Deposit).

Debt-to-Income Ratio: Your Most Important Credit Percentage

Lenders do not just look at your credit score; they look at your Debt-to-Income (DTI) ratio. This is the percentage of your gross monthly income that goes toward paying debts.

To find this percentage, you add up all your monthly debt obligations (mortgage, car loans, minimum credit card payments) and divide them by your gross monthly income. A DTI ratio of 36% or less is generally considered ideal for mortgage approval. Understanding how to find this percentage allows individuals to proactively manage their debt levels before applying for major credit.

Business Finance: Margin, Markup, and Profitability Ratios

For entrepreneurs and business owners, finding percentages is a daily requirement for survival. Miscalculating a margin by even 1% or 2% can mean the difference between a thriving enterprise and bankruptcy.

Gross vs. Net Profit Margins

Profitability is almost always measured in percentages rather than flat currency. The “Gross Profit Margin” indicates the percentage of revenue that exceeds the cost of goods sold (COGS). It is calculated as: [(Revenue – COGS) / Revenue] × 100.

The “Net Profit Margin” is the “bottom line” percentage—what remains after all operating expenses, interest, and taxes have been deducted from total revenue. A high-revenue company with a 2% net profit margin is often in a much more precarious position than a smaller company with a 25% net profit margin. Investors use these percentages to gauge a company’s efficiency and long-term viability.

Measuring Market Share and Growth Trajectories

In business strategy, percentages define a company’s standing in the industry. “Market Share” is the percentage of total sales in an industry generated by a particular company. It is calculated by taking the company’s sales over a period and dividing it by the total sales of the industry over the same period.

Furthermore, Year-over-Year (YoY) growth is calculated as a percentage. If a business made $1 million last year and $1.2 million this year, the 20% growth rate is the figure presented to stakeholders. This percentage provides a standardized way to track progress and set future financial targets.

Practical Financial Tools for Modern Calculations

While understanding the manual formulas for percentages is essential for conceptual clarity, the modern financial world utilizes tools to ensure accuracy and speed.

Leveraging Spreadsheet Automation (Excel/Google Sheets)

In a professional finance setting, spreadsheets are the gold standard. To find a percentage in Excel, one simply uses the cell references and the division operator. For example, =A1/B1 and then clicking the “Percent Style” button.

Advanced users utilize the PERCENTRANK and PERCENTILE functions to analyze data sets, such as comparing a specific stock’s performance against the broader market index. Automating these calculations reduces human error, which is vital when managing large sums of money or corporate budgets.

Financial Calculators and Fintech Apps

For personal finance management, a variety of fintech tools and specialized financial calculators are available. These tools allow users to input variables—such as loan amount, term, and interest rate—to instantly see the percentage of their monthly payment going toward principal versus interest.

Using these tools effectively requires a foundational understanding of what the percentages represent. Whether you are using a mortgage calculator to see how a 0.5% drop in interest rates affects your monthly payment, or a retirement planner to see the percentage of your income you need to save to reach your goals, the ability to interpret these percentages remains the cornerstone of wealth management.

In conclusion, the ability to find and interpret percentages is not just a mathematical exercise; it is a critical life skill within the domain of money. From the simple act of budgeting to the complex world of corporate margins and investment yields, percentages provide the clarity and comparison necessary to make informed, strategic financial decisions. By mastering these calculations, you move from being a passive observer of your finances to an active architect of your economic future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.