For decades, the S&P 500 has stood as the gold standard for equity performance, representing the heartbeat of the American economy. Comprising 500 of the largest, most successful publicly traded companies in the United States, it offers investors a diversified gateway to corporate growth. Legendary investors like Warren Buffett have long championed the index, often suggesting that for the average person, a low-cost S&P 500 index fund is the most sensible way to build long-term wealth.

However, for a beginner, the phrase “buying the index” can be slightly confusing. You cannot buy “the index” itself because it is a mathematical list, not a stock. Instead, you buy products that track its performance. This guide will walk you through the nuances of the S&P 500, the vehicles used to invest in it, and the strategic steps required to add this powerhouse to your portfolio.

Understanding the S&P 500: The Barometer of American Business

Before clicking “buy,” it is essential to understand what the S&P 500 is and why it carries such weight in the financial world. The Standard & Poor’s 500 is a stock market index that tracks the performance of 500 leading companies in leading industries. It covers approximately 80% of available market capitalization in the U.S., making it a reliable proxy for the health of the overall stock market.

Market Capitalization Weighting

The S&P 500 is a market-capitalization-weighted index. This means that companies with higher total market values (like Apple, Microsoft, and Amazon) have a larger impact on the index’s performance than smaller companies. When you buy an S&P 500 fund, you are essentially investing more of your money in the largest “winners” of the economy. This structure naturally weeds out failing companies; if a company’s value drops significantly, it is eventually removed from the index and replaced by a rising star.

Historical Performance and Risk

Historically, the S&P 500 has provided an average annual return of approximately 10% before inflation. While this does not mean the index goes up every year—some years see significant drawdowns—the long-term trajectory has been consistently upward. Understanding this historical context helps investors maintain the discipline needed to hold through market volatility. When you invest in the S&P 500, you are betting on the continued innovation and productivity of the American corporate sector.

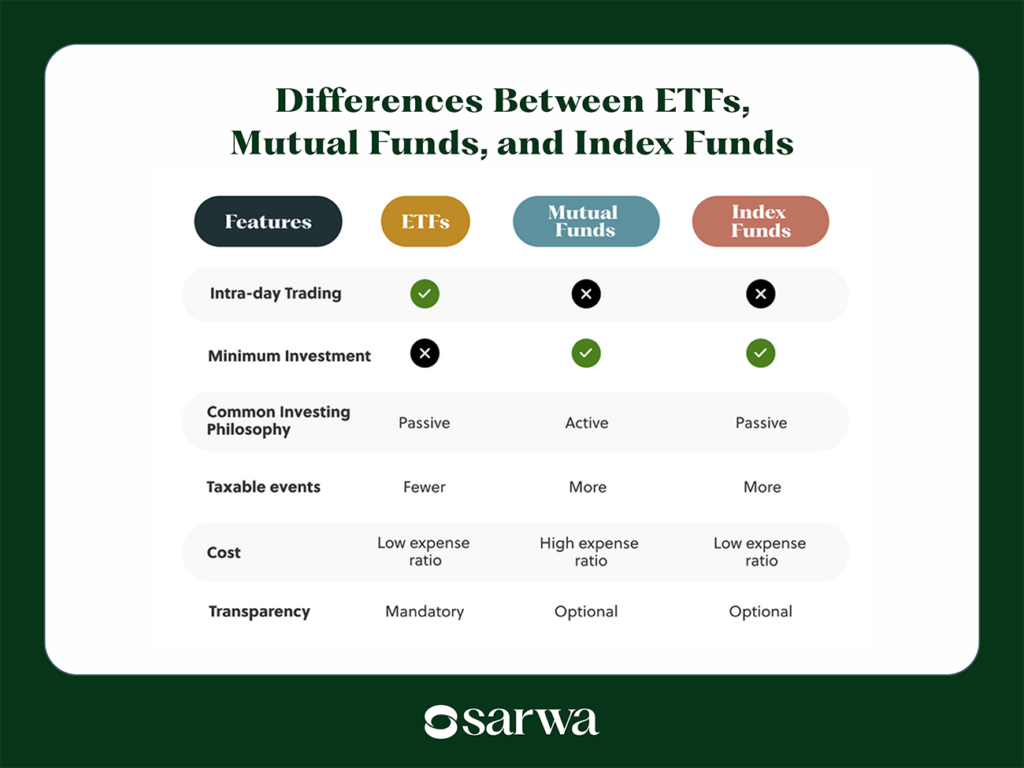

Choosing the Right Investment Vehicle: ETFs vs. Mutual Funds

Since you cannot buy the index directly, you must choose a “wrapper” for your investment. The two primary choices are Exchange-Traded Funds (ETFs) and Index Mutual Funds. Both are designed to mirror the index, but they operate differently in the marketplace.

Exchange-Traded Funds (ETFs)

ETFs are the most popular choice for modern investors. They trade on an exchange just like individual stocks, meaning their price fluctuates throughout the trading day. Major S&P 500 ETFs include the SPDR S&P 500 ETF Trust (SPY), the iShares Core S&P 500 ETF (IVV), and the Vanguard S&P 500 ETF (VOO).

- Liquidity: You can buy or sell ETFs at any time during market hours.

- Lower Minimums: You can often start with the price of a single share (or even less with fractional shares).

- Tax Efficiency: Due to their structure, ETFs generally trigger fewer capital gains distributions than mutual funds.

Index Mutual Funds

Mutual funds are priced only once per day, after the market closes. For long-term investors, this lack of intraday trading is often a benefit, as it discourages “timing the market.” Notable examples include the Vanguard 500 Index Fund (VFIAX) and the Fidelity 500 Index Fund (FXAIX).

- Automatic Investing: Mutual funds are excellent for “set it and forget it” strategies. You can set up an automatic transfer from your bank account to buy $100 worth of the fund every month.

- Minimum Investment Requirements: Some mutual funds require an initial investment (e.g., $3,000 for Vanguard’s VFIAX), though many brokers like Fidelity now offer zero-minimum options.

A Step-by-Step Guide to Purchasing Your First Shares

Once you have decided between an ETF and a mutual fund, the actual process of buying is straightforward. Following a disciplined approach ensures that you minimize fees and maximize your ease of management.

Step 1: Open a Brokerage Account

To access the stock market, you need a brokerage account. You should choose a reputable, low-cost broker. Industry leaders include Vanguard, Charles Schwab, and Fidelity. For those who prefer mobile-first experiences, platforms like Robinhood or Betterment are also options. When opening an account, you will need to choose between a taxable brokerage account (highly flexible) or a tax-advantaged account like a Roth IRA (tax-free growth for retirement).

Step 2: Fund Your Account

After your account is approved, you must link your bank account and transfer funds. Most brokers allow for “Electronic Funds Transfers” (EFT), which typically take 1–3 business days to clear. Once the cash is in your brokerage account, you are ready to execute your trade.

Step 3: Search for the Ticker Symbol

In the search bar of your brokerage platform, type in the ticker symbol of the fund you chose. For example, if you want the Vanguard S&P 500 ETF, you would search for “VOO.” If you prefer the Fidelity Index Mutual Fund, you would search for “FXAIX.”

Step 4: Execute the Trade

For an ETF, you will enter the number of shares you wish to buy and choose a “Market Order” (to buy immediately at the current price) or a “Limit Order” (to buy only if the price hits a specific target). For a mutual fund, you simply enter the dollar amount you wish to invest. Once you click “Place Order,” you officially own a piece of the 500 largest companies in the U.S.

Analyzing Costs: The Importance of Expense Ratios

One of the most critical factors in S&P 500 investing is the “Expense Ratio.” This is the annual fee that the fund management company charges you to run the fund. Because S&P 500 funds are “passively managed” (meaning a computer just follows the index), these fees should be extremely low.

The Impact of Fees on Long-Term Wealth

While a 0.5% fee might sound small, it can cost you hundreds of thousands of dollars over a 30-year career. For example, if you invest $1,000 a month with a 7% return, a fund with a 0.03% expense ratio will leave you with significantly more money than a fund with a 0.75% ratio. When buying the S&P 500, there is no reason to pay a high fee. The underlying assets (the 500 companies) are the same regardless of who provides the fund.

Comparing Tickers

- VOO (Vanguard): 0.03% expense ratio.

- IVV (iShares): 0.03% expense ratio.

- SPY (SPDR): 0.09% expense ratio.

- FXAIX (Fidelity): 0.015% expense ratio.

While SPY is the most famous, it is actually more expensive than VOO or IVV. For a long-term retail investor, VOO or IVV is typically the more cost-effective choice.

Strategic Investing: How to Manage Your S&P 500 Portfolio

Buying the index is just the beginning. To truly build wealth, you must adopt a strategy that accounts for market cycles and personal financial goals.

Dollar-Cost Averaging (DCA)

Instead of trying to “time the market” and buy when you think prices are low, use Dollar-Cost Averaging. This involves investing a fixed amount of money at regular intervals (e.g., $500 every payday), regardless of whether the market is up or down. When prices are high, your $500 buys fewer shares; when prices are low, your $500 buys more shares. Over time, this lowers your average cost per share and removes the emotional stress of market volatility.

Dividend Reinvestment (DRIP)

Most companies in the S&P 500 pay dividends—a portion of their profits distributed to shareholders. When you buy an S&P 500 fund, you will receive these dividends. To maximize growth, you should enable a “Dividend Reinvestment Plan” (DRIP) in your brokerage settings. This automatically uses your dividend payments to buy more shares of the fund, allowing your wealth to compound even faster.

Knowing When to Sell

The S&P 500 is designed to be a long-term investment. Most financial advisors recommend a minimum time horizon of five to ten years. Selling during a market crash is the most common mistake investors make. By understanding that the index represents the collective strength of the U.S. economy, you can find the resolve to stay invested during downturns, waiting for the eventual recovery and subsequent new highs.

In conclusion, buying the S&P 500 index is one of the most effective and accessible ways to participate in the growth of the global economy. By choosing a low-cost ETF or mutual fund, automating your investments through a reputable broker, and maintaining a long-term perspective, you transform from a consumer into an owner of the world’s most powerful corporations. In the world of finance, simplicity often outperforms complexity, and the S&P 500 is the ultimate testament to that truth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.