For decades, the S&P 500 has stood as the quintessential barometer of the American economy. Comprising 500 of the largest publicly traded companies in the United States, it represents approximately 80% of the available market capitalization of the U.S. equity market. For the individual investor, the S&P 500 offers a unique proposition: a way to own a slice of the most successful corporations in the world through a single, diversified investment. legendary investor Warren Buffett has famously championed the index, suggesting that for most people, the best way to invest is through a low-cost S&P 500 index fund.

However, “investing in the S&P 500” is not as simple as buying a single stock. Because the S&P 500 is an index—a mathematical construct—you cannot buy it directly. Instead, you must use specific financial vehicles designed to track its performance. This guide will walk you through the mechanics, strategies, and nuances of building a portfolio centered around this powerhouse index.

Understanding the S&P 500: Why It Is the Gold Standard of Investing

Before committing capital, it is essential to understand what the S&P 500 actually is and why it has become the default choice for both institutional and retail investors. Unlike a simple average, the S&P 500 is a float-adjusted market-capitalization-weighted index. This means that larger companies, like Apple, Microsoft, and Amazon, have a greater impact on the index’s performance than smaller companies within the list.

What Is the S&P 500?

Maintained by S&P Dow Jones Indices, the S&P 500 is a curated list of 500 leading companies in leading industries. To be included, a company must meet strict liquidity and size requirements, and it must be profitable. Because the index is rebalanced periodically, it is “self-cleansing.” Companies that decline in value or relevance are removed, and rising stars are added. This ensures that when you invest in the index, you are always holding the current leaders of the corporate landscape.

The Power of Passive Investing and Market Weighting

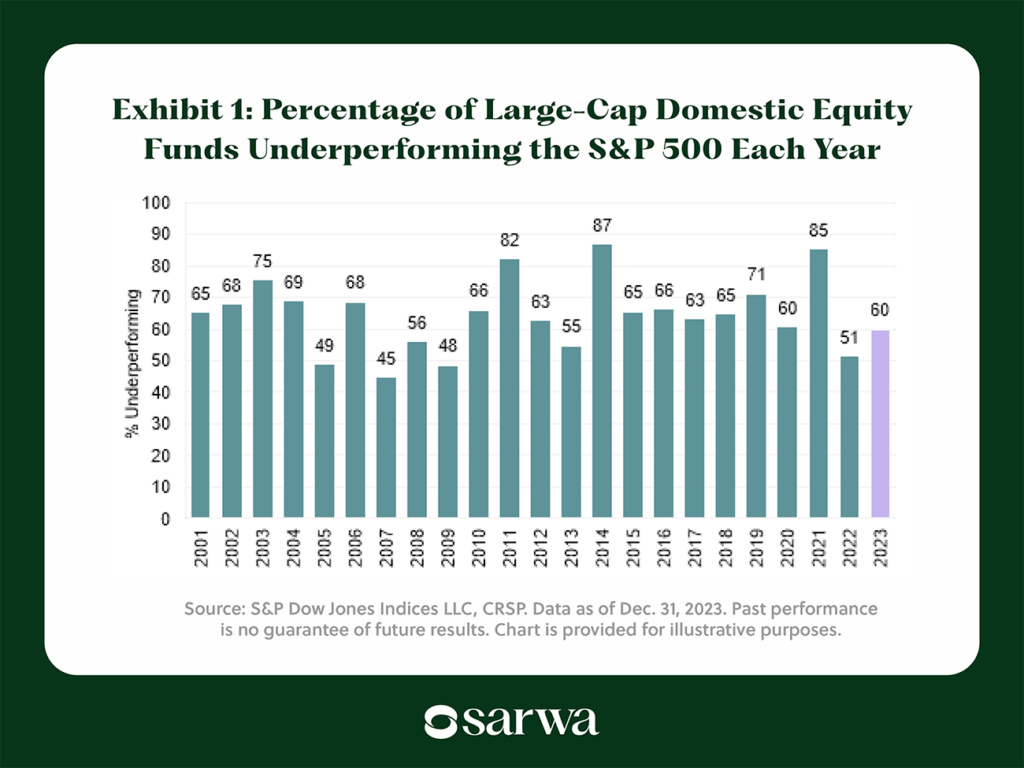

The primary appeal of the S&P 500 lies in the philosophy of passive investing. Rather than trying to “beat the market” by picking individual stocks—a feat that even professional fund managers fail to do consistently over long periods—you simply “own the market.” By mirroring the S&P 500, you benefit from the collective innovation and earnings of the top 500 U.S. companies. Historically, the index has provided an average annual return of roughly 10% before inflation, making it one of the most reliable wealth-building tools in financial history.

The Essential Roadmap to Your First S&P 500 Investment

Transitioning from the concept to the actual investment requires a few logistical steps. The beauty of modern finance is that these steps have become significantly cheaper and more accessible over the last decade.

Choosing the Right Brokerage Account

To buy an S&P 500 fund, you first need a brokerage account. Major platforms like Vanguard, Fidelity, and Charles Schwab are the industry leaders, offering robust tools and zero-commission trades. When selecting a broker, consider the user interface, customer service, and whether they offer “fractional shares,” which allow you to invest a specific dollar amount (e.g., $10) rather than having to buy a full share of a fund.

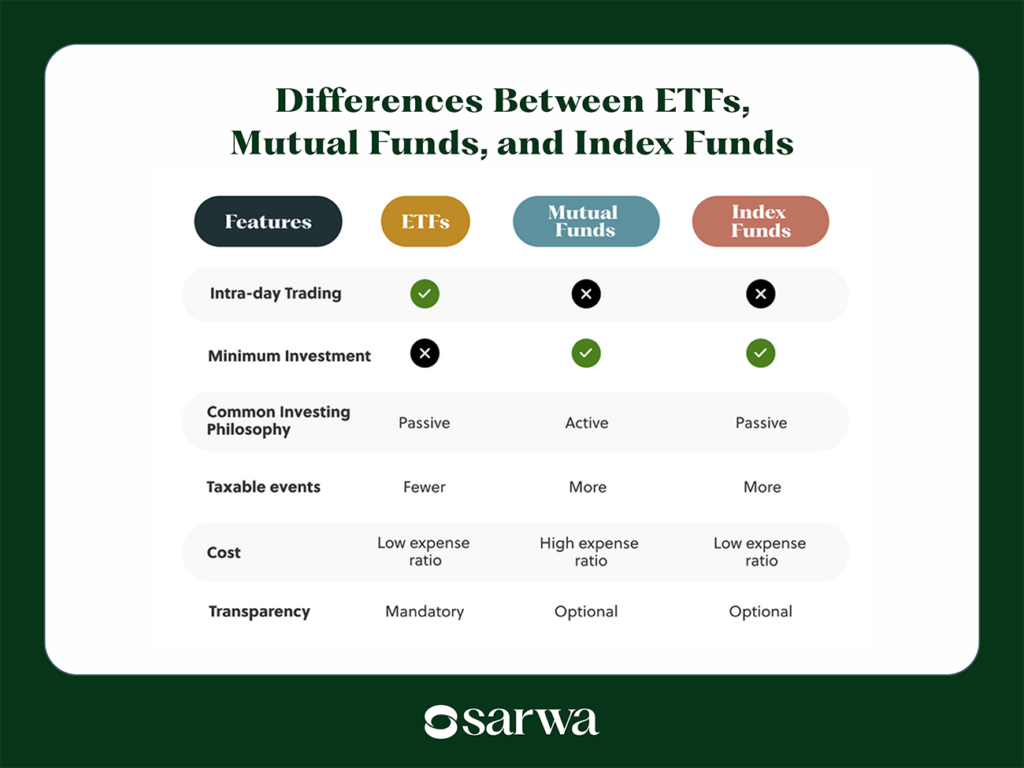

Deciding Between Index Funds and ETFs

There are two primary ways to track the S&P 500: Exchange-Traded Funds (ETFs) and Index Mutual Funds.

- ETFs (e.g., VOO, SPY, IVV): These trade on an exchange just like a stock. You can buy or sell them throughout the trading day at the current market price. ETFs are often more tax-efficient and have no minimum investment requirement beyond the price of one share (or less with fractional shares).

- Index Mutual Funds (e.g., VFIAX, FXAIX): These are priced once at the end of the trading day. They are excellent for automated investing, as you can set up a recurring “buy” for a fixed dollar amount every month. Some mutual funds require a minimum initial investment (e.g., $3,000 for Vanguard’s Admiral Shares).

Analyzing Expense Ratios and Tracking Errors

The cost of owning an S&P 500 fund is expressed as an “expense ratio.” This is the annual fee the fund manager charges to maintain the portfolio. For a standard S&P 500 fund, you should never pay a high fee. Top-tier funds like the Vanguard S&P 500 ETF (VOO) or the Fidelity 500 Index Fund (FXAIX) have expense ratios as low as 0.03% or even 0.015%. This means for every $10,000 invested, you only pay $1.50 to $3.00 per year. Avoiding high-fee “closet indexers” is crucial for maximizing your long-term returns.

Strategic Approaches to Building Your Position

Once you have selected your fund, the next question is how to deploy your capital. Timing the market is notoriously difficult, even for professionals, so adopting a disciplined strategy is key.

Dollar-Cost Averaging (DCA) vs. Lump Sum

Dollar-cost averaging involves investing a fixed amount of money at regular intervals, regardless of whether the market is up or down. This strategy reduces the risk of investing a large amount right before a market downturn. For example, if you have $12,000 to invest, you might invest $1,000 every month for a year. Conversely, a “lump sum” investment involves putting all the money in at once. While historical data suggests that lump-sum investing outperforms DCA about 66% of the time (because the market trends upward), DCA provides a psychological safety net that helps investors stay the course during volatility.

The Role of Dividends and Reinvestment (DRIP)

The S&P 500 doesn’t just grow through share price appreciation; it also pays dividends. Most S&P 500 funds pay a quarterly dividend based on the earnings of the underlying companies. To maximize wealth, investors should utilize a Dividend Reinvestment Plan (DRIP). By automatically using your dividend payouts to buy more shares of the fund, you harness the power of compounding. Over 20 or 30 years, a significant portion of your total returns will come not from the initial investment, but from the “dividends on dividends” generated by this process.

Managing Your Portfolio for Long-Term Growth

Investing in the S&P 500 is not a “set it and forget it” endeavor in the sense that you should ignore it, but rather a commitment to a long-term philosophy.

Tax-Advantaged vs. Taxable Accounts

Where you hold your S&P 500 investment matters for your bottom line.

- 401(k) and IRAs: If you are investing for retirement, using these accounts allows your S&P 500 gains to grow tax-deferred or tax-free (in the case of a Roth IRA). This prevents the “tax drag” that occurs when you have to pay capital gains taxes every year.

- Taxable Brokerage Accounts: These offer more flexibility, allowing you to withdraw money at any time without age-related penalties. However, you will owe taxes on dividends and any realized capital gains when you sell shares.

When to Hold and When to Rebalance

The S&P 500 is inherently diversified across sectors (Tech, Healthcare, Finance, etc.), but it is 100% equities. This means it can be volatile. During a market crash, the index can drop 20%, 30%, or even 50%. The most successful S&P 500 investors are those who can stomach this volatility without selling. Furthermore, as you age, you may want to “rebalance” by selling some of your S&P 500 holdings to buy bonds or cash equivalents to protect your capital as you approach retirement.

Navigating Market Volatility and the “Long Game”

The biggest threat to an S&P 500 investor isn’t market performance; it’s investor behavior. The S&P 500 has survived the Great Depression, World War II, the Dot-com bubble, the 2008 Financial Crisis, and the COVID-19 pandemic. In every instance, it eventually recovered and reached new highs.

The Dangers of Market Timing

Many investors make the mistake of trying to “sell high” and “buy low.” In reality, they often end up selling low out of fear and buying back in high after the recovery has already happened. Missing just a few of the market’s best-performing days can catastrophically reduce your lifetime returns. By staying invested in an S&P 500 index fund through thick and thin, you ensure that you are present for the inevitable rallies that follow downturns.

Conclusion: The Simplicity of Success

Investing in the S&P 500 is perhaps the most efficient way to build wealth in the history of finance. It requires no specialized knowledge of balance sheets, no “inside tips,” and very little time maintenance. By selecting a low-cost ETF or mutual fund, choosing a tax-efficient account, and committing to a strategy of regular contributions and dividend reinvestment, you are positioning yourself to benefit from the future growth of the global economy. The key is not to find the “next big thing,” but to remain disciplined enough to let the 500 best things work for you over time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.