Navigating the landscape of personal finance requires a keen eye for fixed costs, and for the average American household, car insurance represents one of the most significant recurring expenses. When consumers ask, “How much is Progressive car insurance?” the answer is rarely a single figure. Instead, it is a dynamic calculation based on risk assessment, regional economic factors, and individual financial goals. As one of the largest auto insurers in the United States, Progressive has built its reputation on price transparency and data-driven premiums. Understanding the financial mechanics behind their quotes is essential for any savvy consumer looking to optimize their monthly budget while maintaining robust asset protection.

Understanding the Variables: What Drives Your Progressive Premium?

The cost of a Progressive policy is not arbitrary; it is the result of complex actuarial math designed to predict the financial risk a driver poses to the company’s capital reserves. For the policyholder, these variables dictate whether the monthly premium is a manageable $80 or a burdensome $300.

Demographics and Personal Risk Profiles

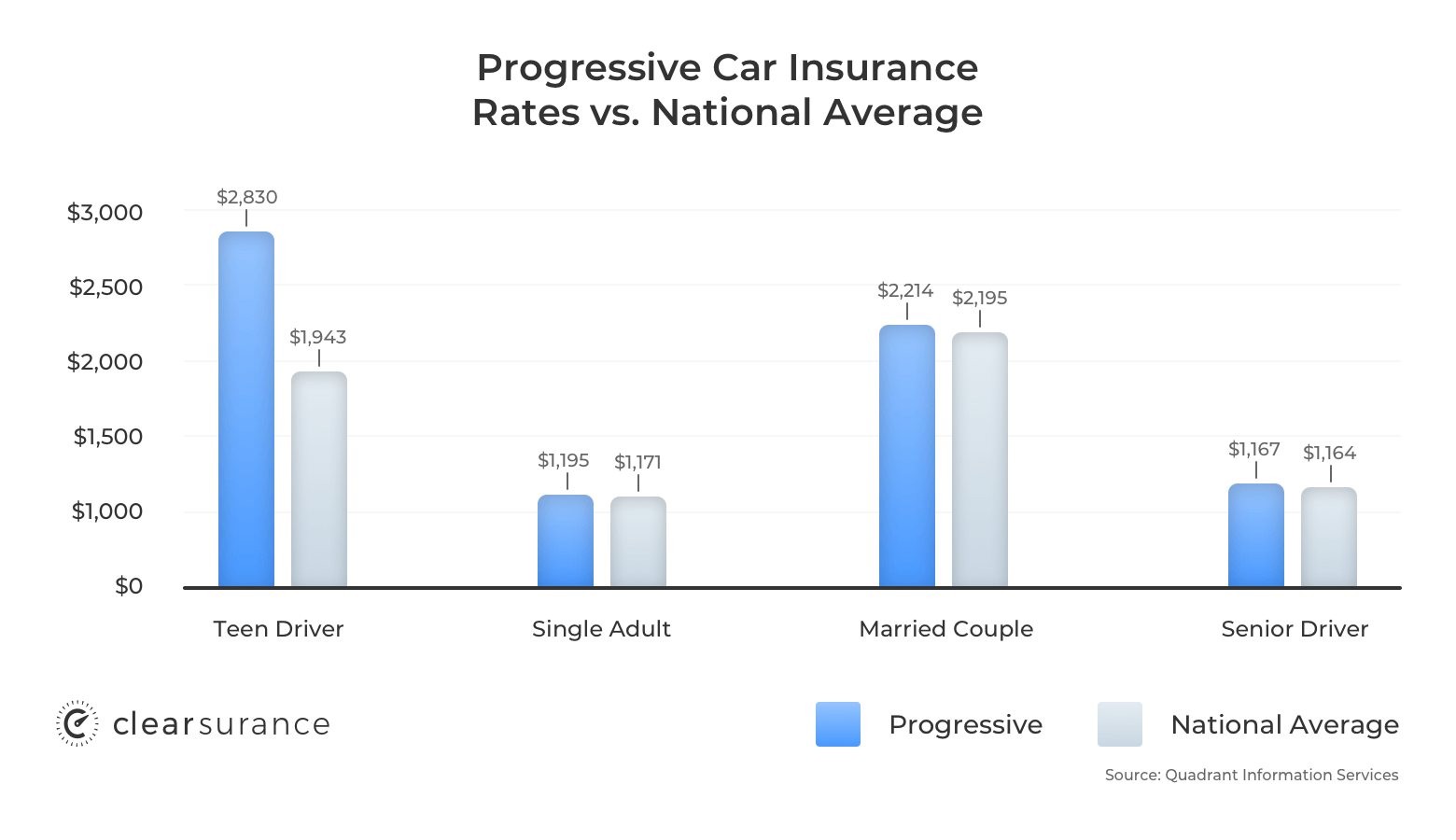

From a financial perspective, your demographic data serves as a proxy for risk. Progressive, like most major insurers, looks closely at age, marital status, and gender. Statistically, younger drivers—particularly those under 25—face higher premiums because they represent a higher probability of total loss claims, which are costly for the insurer. Conversely, married drivers or those in their 40s and 50s often see lower rates, reflecting a historical trend of lower risk. Your driving record is perhaps the most significant “money-saver” or “money-drainer” in this category; a single at-fault accident can increase premiums by 20% to 40% annually, making defensive driving a core strategy for personal wealth preservation.

Vehicle Type and Replacement Costs

The asset you are insuring is the second pillar of cost determination. Progressive evaluates the Year, Make, and Model of your vehicle to determine potential payout requirements. A high-end luxury vehicle or an electric vehicle (EV) with specialized components will naturally command a higher premium due to the increased cost of parts and labor. Financial planning dictates that when purchasing a new car, one must factor in the “total cost of ownership,” which includes the spike in insurance premiums. Progressive’s rates will fluctuate based on the vehicle’s safety ratings and its historical susceptibility to theft, both of which impact the insurer’s bottom line.

Geographic Location and Local Economic Factors

Your zip code acts as a micro-economic environment for insurance pricing. Progressive analyzes local crime rates, the frequency of litigation in your state, and even weather patterns. If you live in an area prone to hail storms or flooding, your comprehensive coverage costs will rise to offset the likelihood of a natural disaster claim. Furthermore, urban areas with high traffic density see more frequent “fender benders,” leading to higher liability costs compared to rural settings. Understanding these geographic pressures is vital for individuals considering a move, as insurance costs can vary by hundreds of dollars just by crossing a county line.

Financial Tools and Savings Programs: Maximizing Your Value

Progressive has distinguished itself in the “Money” niche by providing consumers with specific tools to lower their premiums through behavioral changes and strategic bundling. These programs allow proactive individuals to take control of their financial outlays rather than remaining passive recipients of a quote.

The Snapshot Program: Telematics and Usage-Based Savings

In the age of big data, Progressive’s Snapshot program is a premier financial tool for safe drivers. By utilizing a plug-in device or a mobile app, the company monitors driving habits—such as hard braking, rapid acceleration, and late-night driving. From a personal finance standpoint, this is a “pay-how-you-drive” model. Drivers who exhibit low-risk behavior can see significant discounts, sometimes averaging $145 or more in annual savings. For the budget-conscious consumer, Snapshot offers a way to decouple their premium from general demographic averages and tie it directly to their own disciplined behavior.

Bundling and Multi-Policy Discounts

One of the most effective strategies for reducing insurance overhead is the “bundle.” Progressive offers substantial discounts to customers who combine auto insurance with homeowners, renters, or boat insurance. This is a classic example of corporate cross-selling that benefits the consumer’s net worth. By consolidating policies, you not only simplify your financial management but also unlock “multi-policy” and “multi-car” discounts that can shave 5% to 12% off the total bill. This holistic approach to insurance ensures that your various assets are protected under one umbrella at a bulk-rate price.

Deductible Savings and Long-Term Loyalty Benefits

Progressive offers a “Deductible Savings Bank,” which rewards claim-free periods by reducing your deductible by a set amount (often $50) for every six months you go without an accident. This program essentially builds “insurance equity.” Furthermore, loyalty programs and “Continuous Insurance” discounts reward those who maintain coverage without lapses. From a wealth-building perspective, avoiding lapses is crucial; even a 30-day break in coverage can lead to “high-risk” classification by Progressive’s algorithms, resulting in significantly higher costs when you eventually seek a new policy.

Comparative Analysis: How Progressive Fits into Your Personal Finance Strategy

Deciding whether Progressive is the right financial choice requires more than just looking at the bottom-line number. It requires an analysis of coverage limits versus the cost of premiums and an understanding of how insurance acts as a hedge against financial ruin.

Weighing Cost vs. Coverage Limits

While the cheapest “state minimum” coverage might seem attractive for monthly cash flow, it often represents poor financial planning. If you are involved in a major accident and your liability limits are exhausted, your personal assets—savings, home equity, and future earnings—could be at risk. Progressive allows users to customize these limits. A sound financial strategy involves choosing limits that cover your total net worth, ensuring that a single incident does not derail your long-term investment goals.

Managing Deductibles for Better Cash Flow

The relationship between your deductible and your premium is an inverse one: a higher deductible leads to a lower monthly premium. For individuals with a healthy emergency fund, opting for a $1,000 deductible instead of $250 can save hundreds of dollars annually in premiums. This is a strategic move for those who are “self-insured” for small losses but want Progressive to cover the catastrophic ones. By reallocating the money saved on premiums into a high-yield savings account or an index fund, the consumer turns an insurance expense into an investment opportunity.

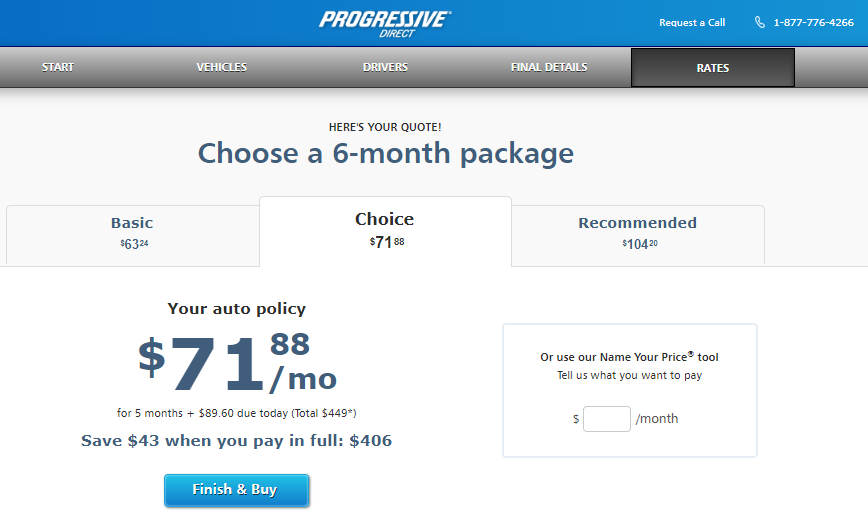

The Name Your Price Tool and Budget Integration

Progressive’s “Name Your Price” tool is a unique financial planning asset. It allows users to input their desired monthly budget, and the system adjusts coverage options to meet that figure. While this requires careful attention to ensure you aren’t sacrificing essential protection, it is an excellent way for families on a strict budget to see exactly what their money buys. It forces a transparent conversation about which “financial risks” you are willing to keep and which you want to transfer to the insurance company.

Long-Term Financial Impact of Choosing the Right Policy

Car insurance is not just a monthly bill; it is a component of your broader financial health. Choosing a provider like Progressive involves considering how they handle claims and how those claims affect your future insurability and credit-like standing within the industry.

Incident Forgiveness and Protecting Your Rates

Progressive offers varying levels of “Accident Forgiveness.” For many, the greatest fear in car insurance is the “rate spike” following a minor error. Small Accident Forgiveness (for claims under $500) and Large Accident Forgiveness (for long-term customers) act as a financial buffer. By paying a slightly higher premium or maintaining loyalty, you are essentially purchasing “price stability.” In the volatile world of personal finance, predictable costs are often more valuable than the lowest possible price, as they allow for more accurate long-term forecasting.

Impact on Credit Score and Financial Health

In most states, insurance companies use a “credit-based insurance score” to help determine premiums. Progressive views a high credit score as an indicator of financial responsibility, which often correlates with lower risk on the road. Therefore, improving your credit score is one of the most effective ways to lower your Progressive insurance costs over time. This creates a virtuous cycle: better financial management leads to lower insurance costs, which leaves more disposable income to pay down debt or invest, further improving your financial standing.

Inflation and the Future of Insurance Costs

Finally, one must consider the macro-economic environment. Inflation in the cost of auto parts and medical care has forced insurance premiums upward across the industry. Progressive’s focus on tech-driven efficiency helps mitigate some of these rises, but consumers must remain vigilant. Regularly reviewing your Progressive policy—at least once a year—ensures that you are still receiving the best value for your dollar in a changing economy. By treating car insurance as a dynamic financial instrument rather than a “set it and forget it” utility, you ensure that your money is always working as hard as possible to protect your lifestyle.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.