The acquisition of a Tesla is no longer just a statement of technological affinity; it is a significant financial decision that requires a nuanced understanding of modern automotive economics. When a prospective buyer asks, “How much is a Tesla new?” the answer is far more complex than a single sticker price. It involves a calculation of base MSRP, fluctuating market adjustments, federal tax implications, and the long-term total cost of ownership (TCO).

In the current economic climate, Tesla has transitioned from a niche luxury manufacturer to a high-volume automaker, utilizing a dynamic pricing model that more closely resembles a tech company’s software updates than a traditional dealership’s fixed pricing. For the financially conscious consumer, navigating this landscape requires an analytical approach to capital outlay and projected savings.

Understanding the Base MSRP: A Breakdown by Model

Tesla’s lineup is strategically tiered to capture different segments of the market, from the “mass-market” entry points to high-performance luxury vessels. Because Tesla operates on a direct-to-consumer model, the price you see on their website is the price you pay, devoid of the traditional dealer markups that often plague other brands.

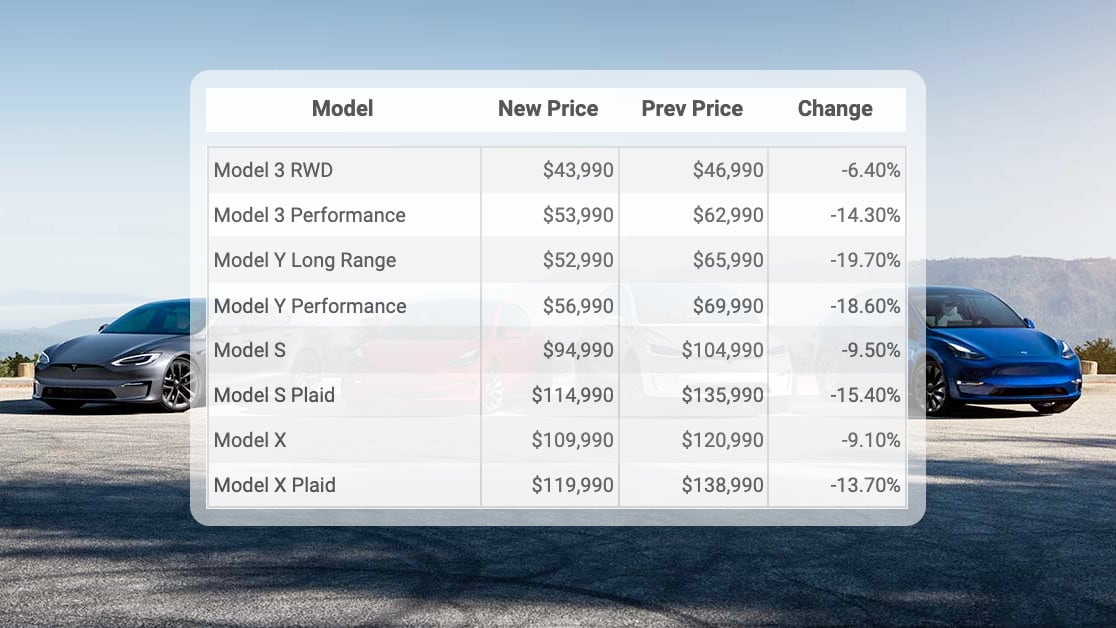

The Model 3: Entry-Level Accessibility

The Model 3 remains the gateway into the Tesla ecosystem. Currently, the Rear-Wheel Drive (RWD) variant represents the lowest point of entry, often hovering between $39,000 and $43,000 depending on the current quarter’s pricing strategy. For the investor or professional looking for a daily commuter with a high ROI in terms of fuel displacement, the Model 3 Long Range and Performance tiers offer higher utility at a price point typically ranging from $47,000 to $55,000.

The Model Y: The Mid-Range Investment

As the best-selling vehicle globally in recent years, the Model Y represents the “sweet spot” for many families and business owners. Its pricing is slightly higher than the Model 3, reflecting its crossover utility. The Long Range and Performance variants typically sit between $48,000 and $53,000. From a financial perspective, the Model Y often holds its value better than the Model 3 due to the high market demand for SUVs, making it a potentially safer asset in terms of depreciation.

Premium Tiers: Model S and Model X

For those in a higher wealth bracket, the Model S (sedan) and Model X (SUV) represent the flagship investments. These vehicles have seen the most dramatic price fluctuations over the last 24 months. The Model S usually starts around $75,000, while the Model X begins closer to $80,000. These vehicles are less about “saving money on gas” and more about luxury asset acquisition, though they still benefit from significantly lower operational costs than their internal combustion engine (ICE) counterparts in the same class, such as the Mercedes S-Class or BMW X7.

Navigating Federal and State Financial Incentives

One cannot accurately calculate the cost of a new Tesla without factoring in the aggressive subsidies provided by the government. These incentives can transform an upper-mid-range purchase into a budget-friendly one, provided the buyer understands the eligibility requirements.

The Federal EV Tax Credit (Section 30D)

Under the Inflation Reduction Act, many Tesla models qualify for a federal tax credit of up to $7,500. However, this is not a universal discount. From a financial planning perspective, buyers must account for two primary constraints: Adjusted Gross Income (AGI) limits and vehicle MSRP caps.

- Income Limits: For the 2024 tax year, individuals earning over $150,000 (or $300,000 for joint filers) do not qualify.

- Price Caps: Vans, SUVs, and trucks (like the Model Y and Model X) must have an MSRP under $80,000. Sedans (like the Model 3) must stay under $55,000.

A critical recent update allows this credit to be applied as a “point-of-sale” discount. This effectively lowers the amount financed, reducing monthly interest payments and the total debt-to-income ratio of the buyer.

Point-of-Sale Rebates and State-Level Savings

Beyond federal help, states like California, Colorado, and New Jersey offer additional rebates or tax exemptions. For example, some states waive sales tax on electric vehicles, which on a $50,000 purchase can save the buyer upwards of $3,000 to $4,000 immediately. When these are stacked with federal credits, the “effective price” of a new Tesla can drop by over $10,000, making the initial capital requirement significantly more palatable.

Beyond the Sticker Price: Long-Term Financial Implications

In personal finance, the “sticker price” is often a distraction from the Total Cost of Ownership (TCO). A Tesla requires a higher upfront investment than a comparable Toyota or Honda, but the financial narrative changes when looking at a five-to-seven-year horizon.

Fuel Savings vs. Electricity Costs

The most immediate financial benefit of a Tesla is the decoupling from volatile oil prices. On average, charging a Tesla costs approximately 30% to 50% of what it costs to fuel a gasoline vehicle for the same distance. For a driver covering 15,000 miles per year, this can result in an annual cash-flow surplus of $1,200 to $2,000. Over a five-year period, this $10,000 in “found money” effectively offsets the higher initial purchase price of the EV.

Maintenance and Insurance Premiums

Tesla vehicles lack many of the “failure points” found in ICE vehicles—there are no oil changes, spark plugs, timing belts, or smog checks. However, the financial profile is not entirely without risk.

- Tires: Teslas are heavy due to their batteries and deliver instant torque, which leads to faster tire wear. Owners should budget for more frequent tire replacements.

- Insurance: This is perhaps the largest “hidden” cost. Because Teslas are high-tech machines with specialized repair requirements, insurance premiums are often 20% to 30% higher than average. Prospective owners should secure an insurance quote before finalizing the purchase to ensure it fits within their monthly budget.

Financing vs. Leasing: Optimizing Your Cash Flow

Choosing how to pay for a Tesla is as important as the price itself. Tesla offers internal financing and leasing, but savvy investors often look toward credit unions or secondary markets for better rates.

Tesla Lending and Traditional Financing

Tesla’s in-house financing is streamlined and integrated into their app, but it is rarely the cheapest option. In a high-interest-rate environment, securing a loan through a local credit union can often save 1% to 2% on the APR. For a $50,000 loan, a 2% difference in interest rates over 72 months can save approximately $3,500. Furthermore, because Tesla’s price cuts can happen at any time, financing a large portion of the car carries the risk of “going underwater” (owing more than the car is worth) if a sudden price drop occurs.

The Depreciation Factor and Resale Value

Historically, Teslas held their value exceptionally well. However, as production has scaled and price cuts have become more frequent, the depreciation curve has normalized. When evaluating a Tesla as a financial asset, it should be viewed as a depreciating tool rather than a value-store.

- Leasing: Leasing a Tesla is often an attractive option for business owners who can deduct the payments as a business expense. However, it is important to note that Tesla traditionally does not allow lessees to buy out the car at the end of the term (though this policy has fluctuated with certain models).

- Cash Purchase: For those with high liquidity, a cash purchase avoids interest entirely, maximizing the “fuel savings” ROI. However, given the current yield on high-interest savings accounts or index funds, one must weigh the opportunity cost of tying up $50,000 in a depreciating asset versus financing at a competitive rate and keeping the cash invested.

Conclusion: Is a New Tesla a Sound Financial Move?

Answering “how much is a tesla new” requires looking through the lens of a financial analyst. While the base price may start in the low $40,000s, the true cost is a moving target influenced by tax credits, state incentives, and operational savings.

From a money management perspective, a Tesla is a high-upfront-cost asset that pays dividends through low operational overhead. For the individual with the right tax profile (to maximize credits) and a high-mileage lifestyle (to maximize fuel savings), a new Tesla can be one of the most financially efficient vehicle purchases available today. However, one must remain vigilant regarding insurance costs and the potential for rapid depreciation. By treating the purchase as a multi-year financial plan rather than a simple transaction, buyers can ensure that their move into the world of sustainable transport is as profitable as it is environmentally conscious.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.