In the contemporary digital economy, the ability to move capital seamlessly across borders and between individuals is a cornerstone of personal and business finance. PayPal has long stood as the vanguard of this revolution, transforming the way we perceive liquidity and transaction speed. While “paying PayPal to PayPal” might seem like a rudimentary task, the financial nuances—ranging from fee optimization to tax implications and currency conversion—require a sophisticated understanding to manage one’s money effectively.

This guide explores the financial architecture of PayPal-to-PayPal transfers, providing a professional roadmap for users who wish to maximize their financial efficiency while minimizing unnecessary costs.

1. Navigating the Financial Architecture of PayPal Transfers

At its core, a PayPal-to-PayPal transfer is a ledger adjustment within a centralized financial ecosystem. However, from a personal finance perspective, not all transfers are created equal. The platform distinguishes between two primary transaction types, each with distinct financial consequences.

Understanding the “Friends and Family” Designation

For many users, the “Friends and Family” option is the preferred method for personal transfers. From a money management standpoint, this is a non-commercial transaction. When funded by a bank account or a PayPal balance, these transfers are typically free of service charges within the same country. This makes it an ideal tool for splitting bills, gifting money, or settling small debts without eroding the principal amount through fees.

However, users must be aware that this “fee-free” status comes at a cost: the forfeiture of Purchase Protection. From a risk management perspective, this should never be used for commercial purposes, as the lack of recourse can lead to a total loss of capital in the event of a dispute.

The “Goods and Services” Model for Commercial Clarity

When paying a freelancer, a vendor, or a seller, the “Goods and Services” designation is mandatory for sound financial practice. In this model, the sender usually pays the face value, while the recipient incurs a percentage-based fee (often 2.9% plus a fixed fee in the US).

While the recipient loses a portion of the inflow, this model provides “Purchase Protection,” which acts as a form of financial insurance. For the payer, using this method ensures that their capital is protected against non-delivery or fraud, an essential component of professional financial conduct.

Impact on Tax Reporting and Compliance

In recent years, tax authorities (such as the IRS in the United States) have increased scrutiny on digital payments. Transfers marked as “Goods and Services” that exceed certain annual thresholds (like the $600 threshold in the US) trigger a 1099-K form. Understanding this distinction is vital for accurate tax planning. Treating a commercial payment as a personal one to avoid fees is not only a violation of terms but can lead to significant financial audits and penalties.

2. Optimizing Transaction Costs and Fee Structures

Efficiency in personal finance is often defined by the ability to minimize “leakage”—the small, recurring costs that diminish your net worth over time. When sending money via PayPal, the method of funding is the primary determinant of the transaction’s cost.

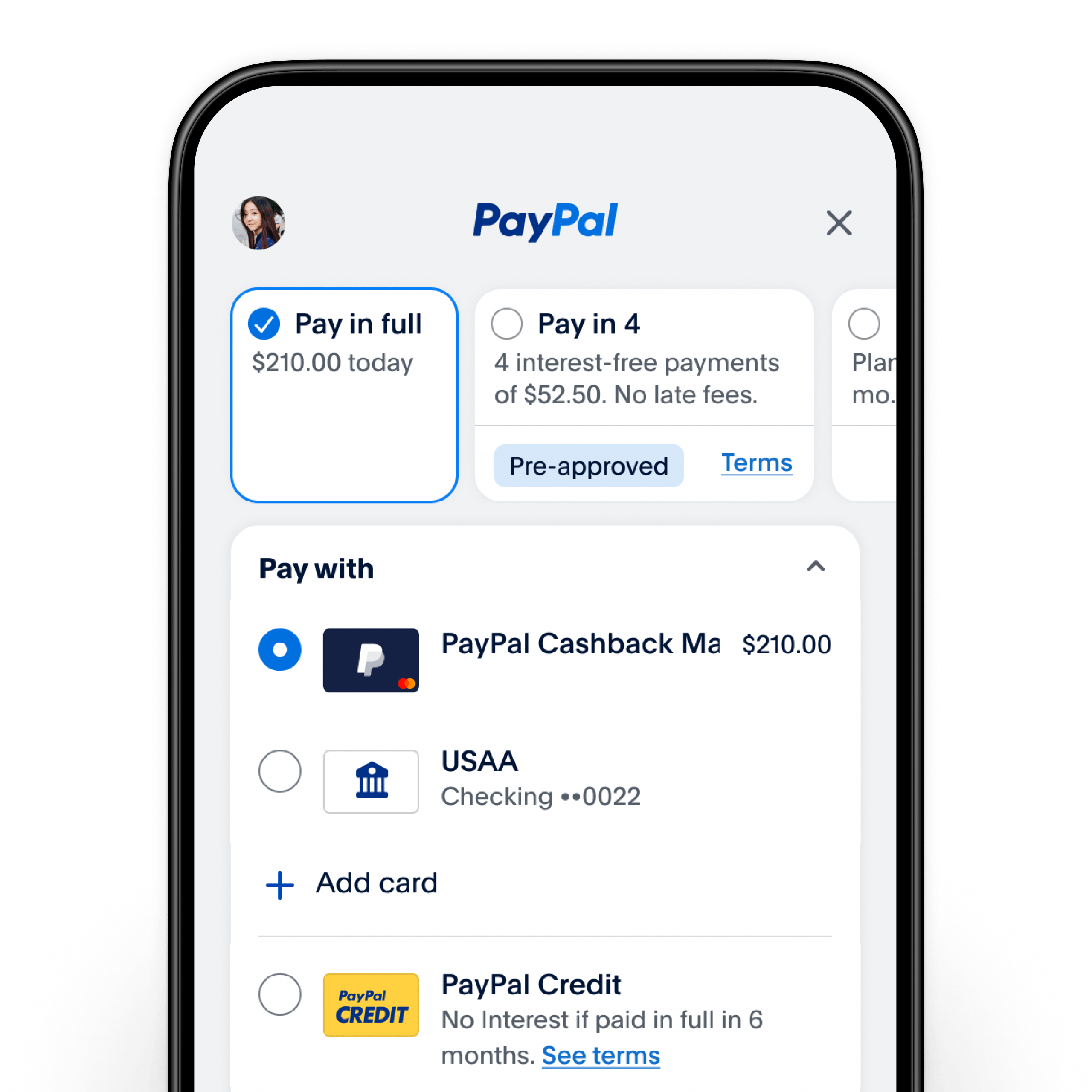

Bank Transfers vs. Credit Card Funding

One of the most critical decisions a user makes is choosing the funding source.

- PayPal Balance/Linked Bank Account: This is generally the most cost-effective method. For domestic personal transfers, there is usually no fee.

- Credit or Debit Cards: Using a card to fund a PayPal-to-PayPal transfer incurs a significant surcharge (typically around 2.9% plus a fixed fee).

From a wealth-building perspective, funding through a credit card is rarely advisable unless the user is strategically chasing credit card rewards or requires short-term liquidity. Even then, the 2.9% fee often outweighs the value of any cash-back or points earned, resulting in a net financial loss.

Strategies for Minimizing Domestic Fees

To maintain financial efficiency, users should maintain a “settlement” balance within their PayPal account or link a dedicated high-yield checking account. By ensuring the account is pre-funded or linked directly to a bank, you bypass the interchange fees associated with card networks. Furthermore, always ensure the transaction is denominated in the local currency to avoid the hidden costs of immediate conversion.

The Hidden Cost of Instant Transfers

While a standard transfer from a bank to PayPal (or vice versa) is free, PayPal offers an “Instant Transfer” feature to debit cards for a fee (often 1.75% of the amount, capped at a certain maximum). For a professional managing cash flow, this fee is an unnecessary expense. Planning transactions 1–3 business days in advance allows for standard transfers, preserving that 1.75% within your investment or savings pool.

3. Cross-Border Payments and Currency Management

In an increasingly globalized world, paying someone in a different country via PayPal is a common occurrence. However, international finance introduces two major costs: cross-border transaction fees and currency conversion spreads.

Managing the International Transaction Surcharge

When sending money to a PayPal account in a different country, a “cross-border” fee is applied. This is often a fixed percentage (e.g., 5%) added to the transaction. For individuals looking to optimize their international spending, it is important to calculate whether PayPal is the most efficient vehicle or if a dedicated foreign exchange (FX) service might offer better rates for larger sums.

The Reality of Currency Conversion Spreads

When you pay someone in a different currency, PayPal performs the conversion. It is a common misconception that this is done at the “mid-market” rate. In reality, PayPal adds a “spread” or margin—usually around 3% to 4%—above the wholesale exchange rate.

To manage this, savvy users often choose to pay in their own local currency and let the recipient’s bank handle the conversion, or use a multi-currency account (like a linked digital wallet) that offers lower spreads. Understanding these “hidden” percentages is key to preventing significant financial erosion in international transfers.

Strategic Use of Multi-Currency Balances

PayPal allows users to hold balances in multiple currencies. If you frequently pay vendors in Euros, for example, it may be financially prudent to hold a Euro balance within your account. This allows you to time your currency purchases when exchange rates are favorable, rather than being forced into a high-spread conversion at the moment of payment.

4. Security, Risk Management, and Capital Protection

A core tenet of financial literacy is the protection of assets. When sending money via PayPal, the “security” isn’t just about encryption; it’s about the financial protocols that protect your money from fraud and error.

The Role of PayPal Purchase Protection

For any transaction involving the exchange of value for goods or services, Purchase Protection is a vital financial tool. It allows the payer to dispute a transaction if the item is not received or is significantly different from the description. This acts as a decentralized escrow service. For the payer, this eliminates the risk of “capital forfeiture” in a bad-faith transaction, making it a cornerstone of safe online business finance.

Implementing Two-Factor Authentication (2FA) for Asset Security

From a digital security standpoint, your PayPal account is a gateway to your liquid assets. Utilizing hardware keys or authenticator apps (rather than SMS-based codes) is a professional-grade necessity. Protecting the “point of exit” for your money is just as important as the investment strategy used to grow that money.

Identifying and Avoiding Financial Phishing

The “Money” niche is rife with bad actors attempting to intercept transfers. Professional users must be adept at identifying “spoof” emails or fake payment confirmations. A common scam involves a buyer sending a fake “payment received” email to a seller, hoping the seller will ship the item before checking their actual PayPal balance. Always verify the “Available Balance” within the official PayPal interface before considering a transaction settled.

5. Integrating PayPal into a Professional Financial Ecosystem

To truly master PayPal-to-PayPal payments, one must look beyond the individual transaction and consider how these movements of capital fit into a broader financial strategy.

Cash Flow Management for Freelancers and Solopreneurs

For those using PayPal as a primary revenue stream, the platform serves as a “clearinghouse.” Efficient cash flow management involves regularly sweeping funds from PayPal into a high-yield savings account (HYSA) or a business brokerage account. Keeping large sums in a PayPal balance is often sub-optimal, as that capital is not earning interest.

Automated Accounting and Bookkeeping

Modern financial tools allow for the direct integration of PayPal transaction history into accounting software like QuickBooks or Xero. This automation is essential for accurate financial reporting. By categorizing PayPal-to-PayPal payments correctly in real-time, individuals can ensure they are maximizing their deductible business expenses and maintaining a clear picture of their net cash flow.

The Future of Digital Liquidity

As digital wallets evolve, PayPal is increasingly integrating with other financial instruments, including cryptocurrency and “Buy Now, Pay Later” (BNPL) options. While these offer convenience, they also introduce new layers of interest rates and volatility. A professional approach to “paying PayPal to PayPal” involves staying informed about these shifts in the financial landscape, ensuring that every dollar moved is done so with a clear understanding of its cost, its protection, and its destination.

By viewing PayPal not just as an app, but as a sophisticated financial tool, users can ensure their peer-to-peer payments are secure, cost-effective, and fully integrated into their long-term wealth management strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.