United Services Automobile Association (USAA) has long stood as a paragon of financial stability and service excellence within the American financial landscape. For nearly a century, it has provided a suite of insurance, banking, and investment products tailored specifically to the needs of the military community. However, unlike many of its competitors in the open market, USAA operates on a membership-based model. This exclusivity often leads to a central question for those seeking high-quality personal finance solutions: Who exactly qualifies for USAA insurance?

Understanding the eligibility requirements is more than just a hurdle to cross; it is the gateway to a financial ecosystem designed to support the unique lifestyle and challenges of those who serve. In this guide, we will explore the nuances of USAA membership, the specific categories of individuals who qualify, and the long-term financial advantages of securing coverage through this specialized institution.

Understanding USAA’s Unique Membership Model

USAA is not a publicly traded corporation in the traditional sense; it is a diversified financial services group that incorporates a reciprocal inter-insurance exchange. This structure is fundamental to its “Money” niche, as it influences how the company handles premiums, dividends, and capital.

The History and Mission of USAA

Founded in 1922 by a group of 25 Army officers who were unable to secure auto insurance due to the perceived high risk of their profession, USAA was built on a foundation of mutual trust. The mission was simple: to provide financial security to those who serve. Today, that mission has expanded to include a wide array of financial tools, but the core focus remains on the military community. This historical context is vital because it explains why the eligibility rules are strictly enforced—they are designed to preserve the integrity and financial health of the pool for its members.

Why Membership Matters in Personal Finance

From a personal finance perspective, a USAA membership is a valuable asset. Because the organization focuses on a specific demographic, it can offer rates and benefits that are often more competitive than “big box” insurers. Furthermore, USAA frequently returns a portion of its profits to members in the form of dividends or distributions to Subscriber’s Savings Accounts, a feature rarely found in standard commercial insurance models.

Who Qualifies for USAA Insurance? (The Core Eligibility Rules)

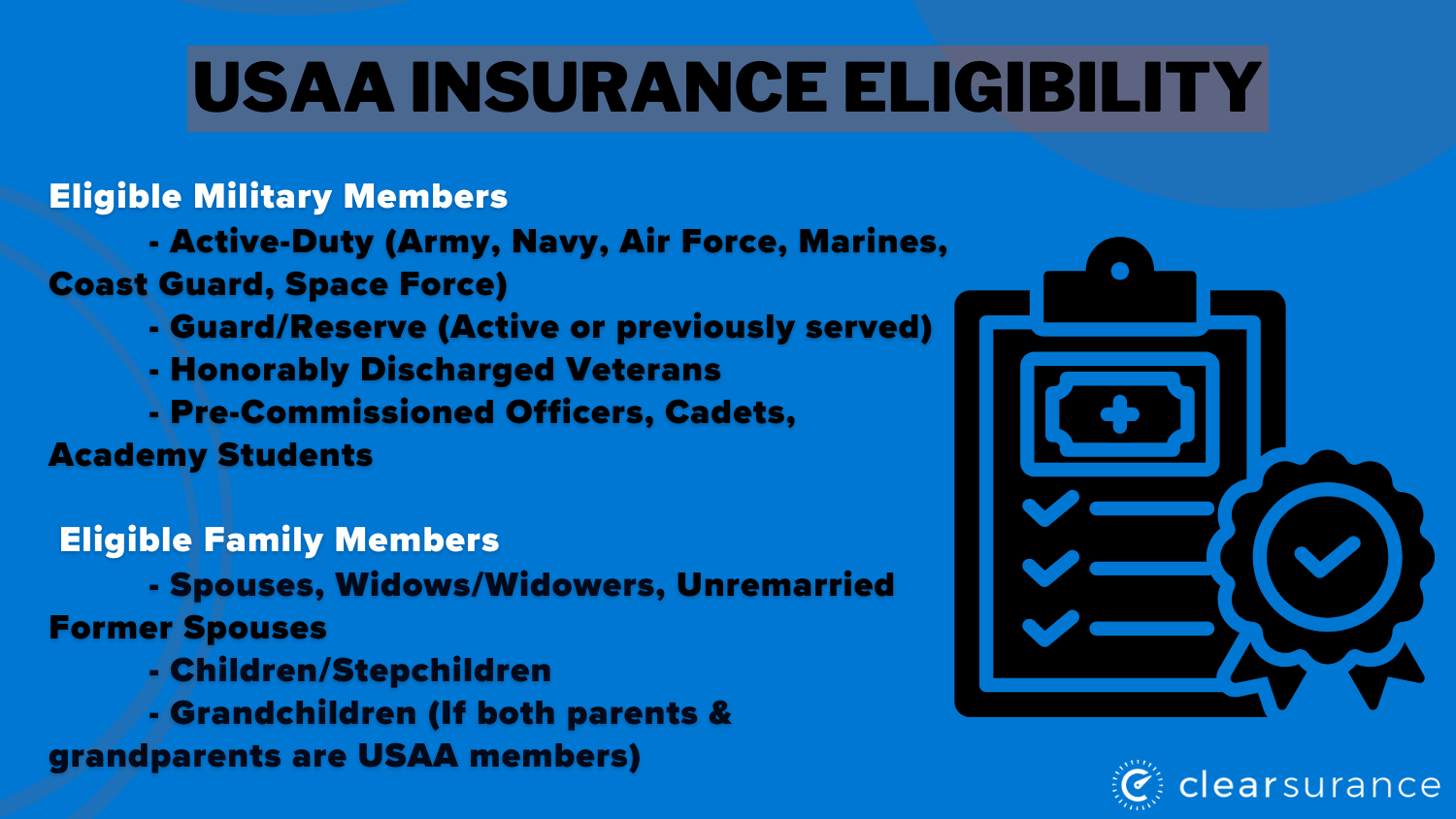

The primary question of eligibility is governed by federal law and USAA’s own internal bylaws. Generally, eligibility is extended to those who have a direct connection to the U.S. Uniformed Services.

Active Duty, Guard, and Reserve Members

The most straightforward path to eligibility is current service. Individuals currently serving in the U.S. Army, Navy, Air Force, Marine Corps, Coast Guard, or the recently established Space Force are eligible to join. This includes:

- Active Duty: Those serving full-time in their respective branches.

- National Guard and Reserve: Those serving in a part-time capacity who are subject to activation.

For these individuals, joining USAA early in their careers can set a strong foundation for lifetime financial management, especially given the various deployment protections the company offers.

Veterans and Retirees

Eligibility is not revoked once a member leaves the service, provided they were discharged under honorable conditions. This includes:

- Retirees: Those who have completed the requisite years of service to earn a military pension.

- Veterans: Those who served and were honorably discharged. It is a common misconception that one must be a “retiree” to qualify; even those who served a single term of enlistment are eligible to apply for USAA insurance products.

Family Members and Legacies

One of the most powerful aspects of USAA is its “legacy” eligibility. Once an individual establishes a USAA membership and purchases a property or casualty insurance policy (such as auto or renters insurance), their eligibility can be passed down to their children.

- Spouses: Widows, widowers, and un-remarried former spouses of USAA members who joined USAA prior to or during the marriage are generally eligible.

- Children: Children and step-children of USAA members can establish their own memberships, allowing the benefits of USAA to span generations. This makes USAA a cornerstone of intergenerational wealth and protection planning.

Cadets and Midshipmen

Students at U.S. service academies (West Point, Annapolis, Air Force Academy, Coast Guard Academy) or those in advanced ROTC programs on a scholarship are also eligible to join. USAA recognizes that these individuals are the future leaders of the military and offers them early access to financial tools and low-interest “commissioning loans” to help them transition into active duty.

Navigating the Application and Verification Process

While the eligibility categories are clear, the process of becoming a member requires formal verification to ensure the security and exclusivity of the group.

Required Documentation

To apply for USAA insurance, you will need to provide specific information to verify your service or your relationship to a service member. This typically includes:

- Social Security Number: Used for identity verification and credit checks (standard for insurance underwriting).

- Service Details: Dates of service, branch, and rank.

- Discharge Status: For veterans, a DD214 (Certificate of Release or Discharge from Active Duty) may be required to prove an honorable discharge.

Joining as a Spouse or Child

If you are joining based on a parent’s or spouse’s membership, you will need their USAA number or enough identifying information for the system to link your records. It is important to note that the “primary” member (the one with the military service) must usually have established a P&C (Property and Casualty) policy at some point for the eligibility to flow down to the next generation.

The Financial Advantages of USAA Insurance

Once eligibility is confirmed, the focus shifts to why USAA is a preferred choice for personal finance enthusiasts. The benefits extend far beyond just “having insurance.”

Competitive Pricing and Dividend Potential

In the world of personal finance, minimizing recurring expenses is key to long-term wealth building. USAA consistently ranks as one of the most affordable insurers in the United States. Furthermore, because USAA is a reciprocal exchange, it is owned by its members. When the company performs well and has excess capital after paying claims and maintaining reserves, it may return money to members. These “Subscriber’s Account” distributions can significantly lower the effective cost of insurance over many years.

Specialized Coverage for Military Life

Standard insurance companies often struggle to accommodate the complexities of military life, such as frequent Permanent Change of Station (PCS) moves or long-term deployments. USAA provides specific financial protections, such as:

- Deployment Discounts: Significant reductions in auto insurance premiums when a vehicle is stored during a deployment.

- Personal Property Coverage: Enhanced coverage for military uniforms and equipment, which can be expensive to replace.

- Global Reach: The ability to maintain coverage and financial services while stationed overseas, a logistical hurdle that many domestic banks and insurers cannot easily clear.

Beyond Insurance: The Full USAA Financial Ecosystem

While insurance is the “hook” for many, the true power of USAA membership lies in its comprehensive financial ecosystem. Eligibility for insurance usually opens the door to their banking and investment arms.

Banking and Investment Services

USAA Bank is renowned for its member-centric policies, such as early direct deposit (receiving a military paycheck up to two days early) and an extensive network of ATM fee reimbursements. For the savvy investor, USAA offers specialized tools for retirement planning and wealth management that take into account the unique structure of military pensions and the Thrift Savings Plan (TSP).

Long-term Financial Planning

Successful personal finance is about the integration of all moving parts: protection (insurance), growth (investments), and liquidity (banking). USAA provides a “one-stop-shop” where these elements are coordinated. For instance, their homeowners insurance is designed to work seamlessly with their VA mortgage lending products, ensuring that members are not only getting into a home with favorable terms but are also protecting that asset correctly from day one.

Conclusion

Determining who qualifies for USAA insurance is the first step in accessing one of the most robust financial platforms in the United States. By limiting its membership to the military community and their families, USAA maintains a risk pool and a service model that prioritizes the financial well-being of those who have sacrificed for the nation.

Whether you are an active-duty service member looking for your first auto policy, a veteran seeking to consolidate your finances, or the child of a member looking to carry on the legacy, understanding the nuances of USAA eligibility is crucial. In the realm of personal finance, few decisions are as impactful as choosing an institution that aligns its success with your own. For those who qualify, USAA offers more than just insurance; it offers a lifetime of financial partnership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.