Securing a mortgage is often the most significant financial transaction an individual will undertake in their lifetime. It is a complex blend of personal finance management, long-term investment strategy, and rigorous bureaucratic navigation. While the prospect of owning a home is a cornerstone of financial stability, the path to obtaining a loan can appear daunting to the uninitiated.

Understanding how to get a mortgage requires more than just a healthy bank account; it demands a strategic approach to your financial profile, an understanding of the lending landscape, and meticulous preparation. This guide breaks down the essential components of the mortgage process, transforming a complex financial hurdle into a manageable, step-by-step journey toward property ownership.

Understanding the Fundamentals of Mortgage Eligibility

Before a lender entrusts you with hundreds of thousands of dollars, they must conduct a deep dive into your financial “character” and capacity. This assessment is primarily built upon three pillars: your creditworthiness, your debt-to-income ratio, and your history of professional stability.

Credit Scores: The Foundation of Your Application

Your FICO score is perhaps the most critical number in the mortgage process. It acts as a shorthand for your reliability as a borrower. Lenders use this score to determine not only whether you qualify for a loan but also the interest rate you will pay. A higher score translates to lower interest rates, which can save you tens of thousands of dollars over the life of a 30-year loan.

To optimize your score before applying, it is essential to review your credit reports for errors, keep your credit utilization below 30%, and avoid opening any new lines of credit in the six months leading up to your application. Even a 20-point difference in your score can move you from a “prime” to a “subprime” category, significantly impacting your monthly premium.

Debt-to-Income Ratio (DTI) and Financial Stability

Lenders use the Debt-to-Income (DTI) ratio to measure your ability to manage monthly payments. This is calculated by dividing your total monthly debt obligations (including the projected mortgage payment, student loans, car payments, and credit card minimums) by your gross monthly income.

Most conventional lenders prefer a DTI ratio of 36% or lower, though some programs, such as FHA loans, may allow for ratios as high as 43% or even 50% in specific circumstances. Understanding your DTI helps you determine “how much house” you can actually afford, rather than just what the bank is willing to lend you.

Employment History and Verifiable Income

Consistency is key in the eyes of a mortgage underwriter. Generally, lenders look for a steady two-year employment history within the same industry. If you are a W-2 employee, this process is straightforward, requiring recent pay stubs and W-2 forms.

However, for the self-employed or those with “gig economy” income, the scrutiny is higher. You will likely need to provide at least two years of federal tax returns. Lenders will look at your net income after business deductions, which can sometimes make it harder for entrepreneurs to qualify for the amount they need if they have aggressively utilized tax write-offs.

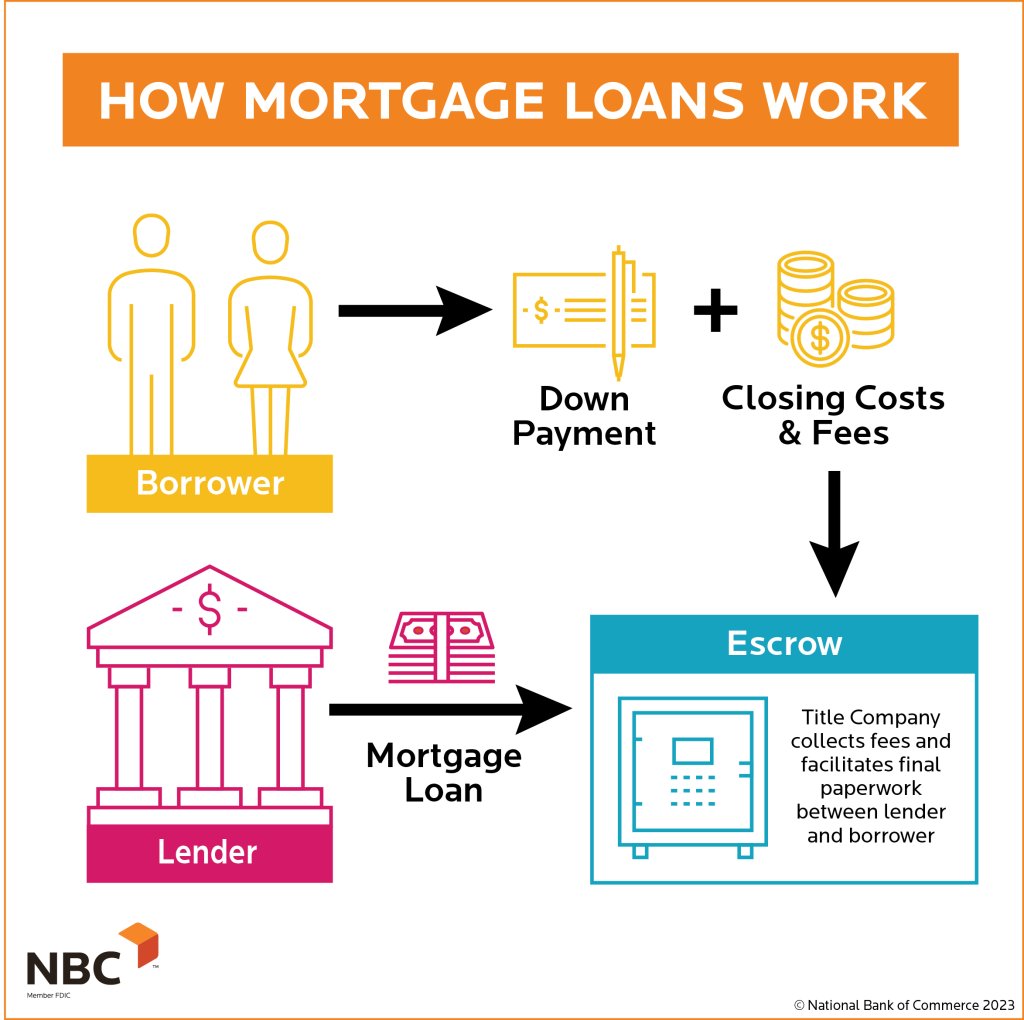

The Financial Preparation Phase: Saving for More Than Just a Down Payment

A common misconception is that the down payment is the only upfront cost of a mortgage. In reality, a successful mortgage application requires a broader “cash-to-close” strategy that includes several different financial buckets.

The 20% Myth vs. Reality: Down Payment Options

While the “20% down” rule is the gold standard for avoiding Private Mortgage Insurance (PMI) and securing the best rates, it is by no means a strict requirement. Many first-time homebuyer programs allow for down payments as low as 3% for conventional loans or 3.5% for FHA loans. VA loans and USDA loans even offer 0% down options for eligible service members or rural buyers.

The trade-off for a lower down payment is usually a higher monthly cost, either through a slightly higher interest rate or the addition of mortgage insurance. When deciding on your down payment, consider your “opportunity cost”—would that extra cash be better served in an emergency fund or a diversified investment portfolio?

Factoring in Closing Costs and Cash Reserves

Closing costs typically range from 2% to 5% of the home’s purchase price. These fees cover appraisals, title insurance, attorney fees, and loan origination charges. Many buyers are caught off guard by these costs at the final hour.

Furthermore, many lenders require “reserves”—liquid assets left in your account after the down payment and closing costs are paid. These reserves act as a safety net, proving to the lender that you can continue to make payments if you were to lose your job or face an unexpected medical expense. Typically, lenders look for two to six months of mortgage payments in liquid savings.

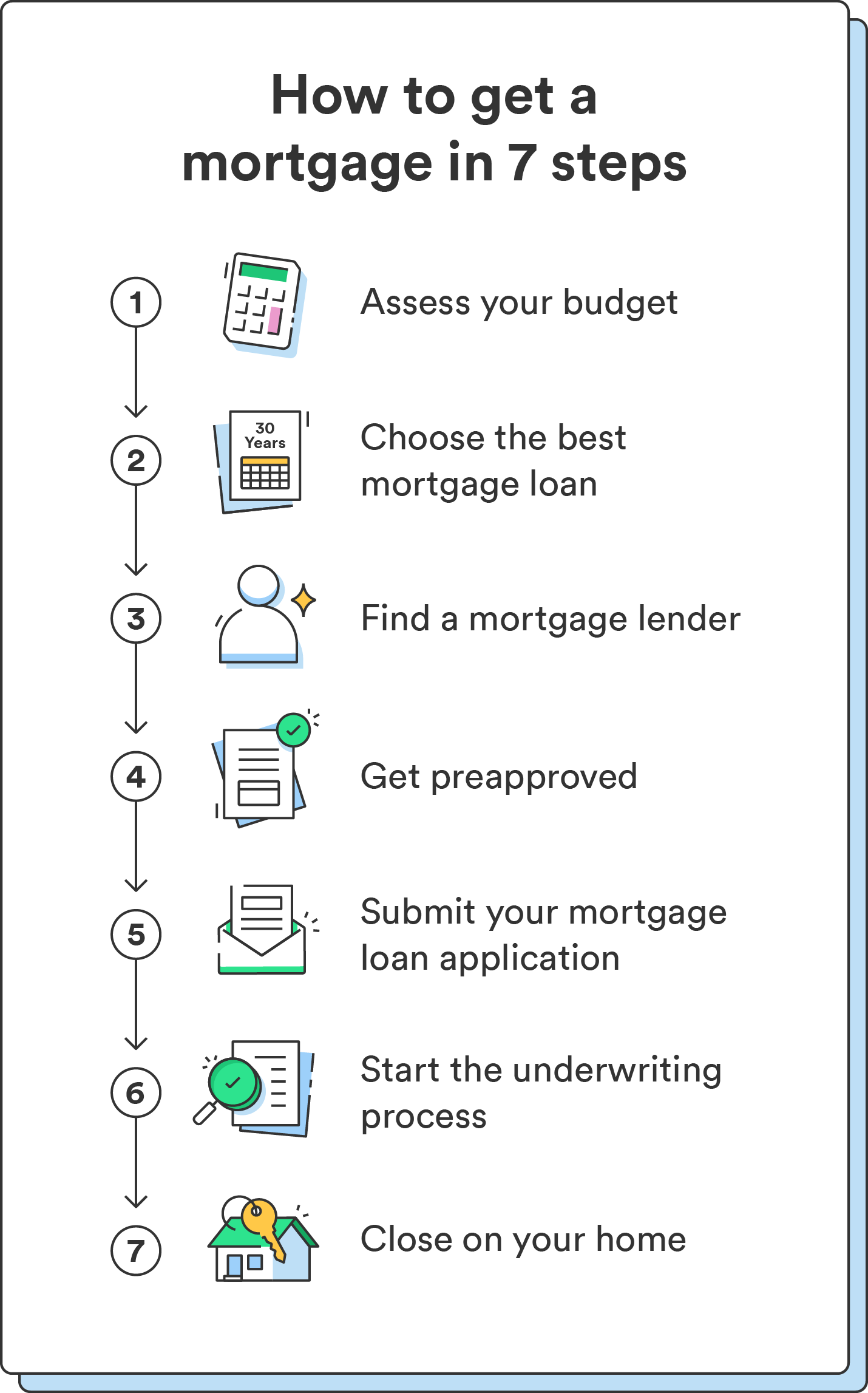

The Role of Pre-Approval in a Competitive Market

A pre-approval is not the same as a pre-qualification. A pre-qualification is a surface-level estimate based on unverified data. A pre-approval, however, involves a lender actually pulling your credit and reviewing your financial documents.

In a competitive real estate market, a pre-approval letter is your “hunting license.” It signals to sellers that you are a serious, qualified buyer whose financing is unlikely to fall through. It also gives you a clear boundary for your house hunt, ensuring you don’t waste time looking at properties that are financially out of reach.

Choosing the Right Mortgage Product for Your Financial Strategy

Not all mortgages are created equal. The “right” loan depends on your long-term financial goals, how long you plan to stay in the home, and your tolerance for interest rate fluctuations.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The 30-year fixed-rate mortgage is the most popular choice because it offers predictability; your principal and interest payments remain the same for the entire duration of the loan. For those looking for a shorter path to equity, 15-year fixed-rate mortgages offer lower interest rates but significantly higher monthly payments.

Adjustable-Rate Mortgages (ARMs) typically offer a lower “teaser” rate for an initial period (e.g., 5, 7, or 10 years). After that, the rate adjusts based on market indices. ARMs can be a strategic choice if you know you will sell the home or refinance before the introductory period ends, but they carry the risk of significantly higher payments in the future.

Government-Backed Loans: FHA, VA, and USDA

The federal government insures several types of loans to make homeownership more accessible:

- FHA Loans: Ideal for those with lower credit scores or smaller down payments.

- VA Loans: Reserved for veterans and active-duty service members, offering 0% down and no mortgage insurance.

- USDA Loans: Targeted at low-to-moderate-income buyers in designated rural areas, also offering 0% down options.

Conventional Loans and Jumbo Financing

Conventional loans are not insured by the government and typically follow the guidelines set by Fannie Mae and Freddie Mac. They often have stricter credit requirements but offer more flexibility regarding property types and insurance cancellation.

If you are looking to purchase a high-end property that exceeds the “conforming loan limits” set by the Federal Housing Finance Agency (FHFA), you will need a Jumbo Loan. These require much larger down payments (often 20% or more) and exceptionally high credit scores.

The Mortgage Application and Approval Process Step-by-Step

Once you have identified a property and had an offer accepted, the formal mortgage process begins. This stage is a marathon of documentation and verification.

Documentation: Organizing Your Financial Life

Efficiency is your best friend during the application process. You will need to provide:

- The last two years of W-2s and tax returns.

- The last 60 days of bank statements for all accounts.

- Proof of any additional assets (401ks, IRAs, brokerage accounts).

- Identification and Social Security verification.

- A “gift letter” if any part of your down payment is being provided by a family member.

The Underwriting Phase: What Happens Behind the Scenes

Underwriting is the “black box” of the mortgage world. An underwriter reviews every detail of your application to ensure it meets the lender’s guidelines and that the property itself is a sound investment. During this time, the lender will order an appraisal to ensure the home is worth what you are paying for it.

The most important rule during underwriting is: Do not change your financial situation. Do not quit your job, do not finance a new car, and do not make large, unexplained deposits into your bank accounts. Any of these actions can trigger a re-evaluation of your file and lead to a loan denial at the eleventh hour.

Final Walkthrough and Closing the Deal

Once the underwriter gives the “Clear to Close,” you are in the home stretch. You will receive a Closing Disclosure (CD) at least three days before your closing date. This document outlines the final terms of your loan and the exact amount of money you need to bring to the table.

At the closing table, you will sign a mountain of paperwork, including the Promissory Note (your promise to repay the loan) and the Deed of Trust (which puts the property up as collateral). Once the funds are wired and the deed is recorded, you are officially a homeowner.

Conclusion

Getting a mortgage is a rigorous exercise in financial discipline and patience. By focusing on your credit health, saving strategically for both the down payment and the “hidden” costs of closing, and selecting a loan product that aligns with your broader financial plan, you can navigate the process with confidence. While the paperwork may be extensive, the result—a tangible asset that builds equity over time—remains one of the most effective ways to build long-term wealth in the modern economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.