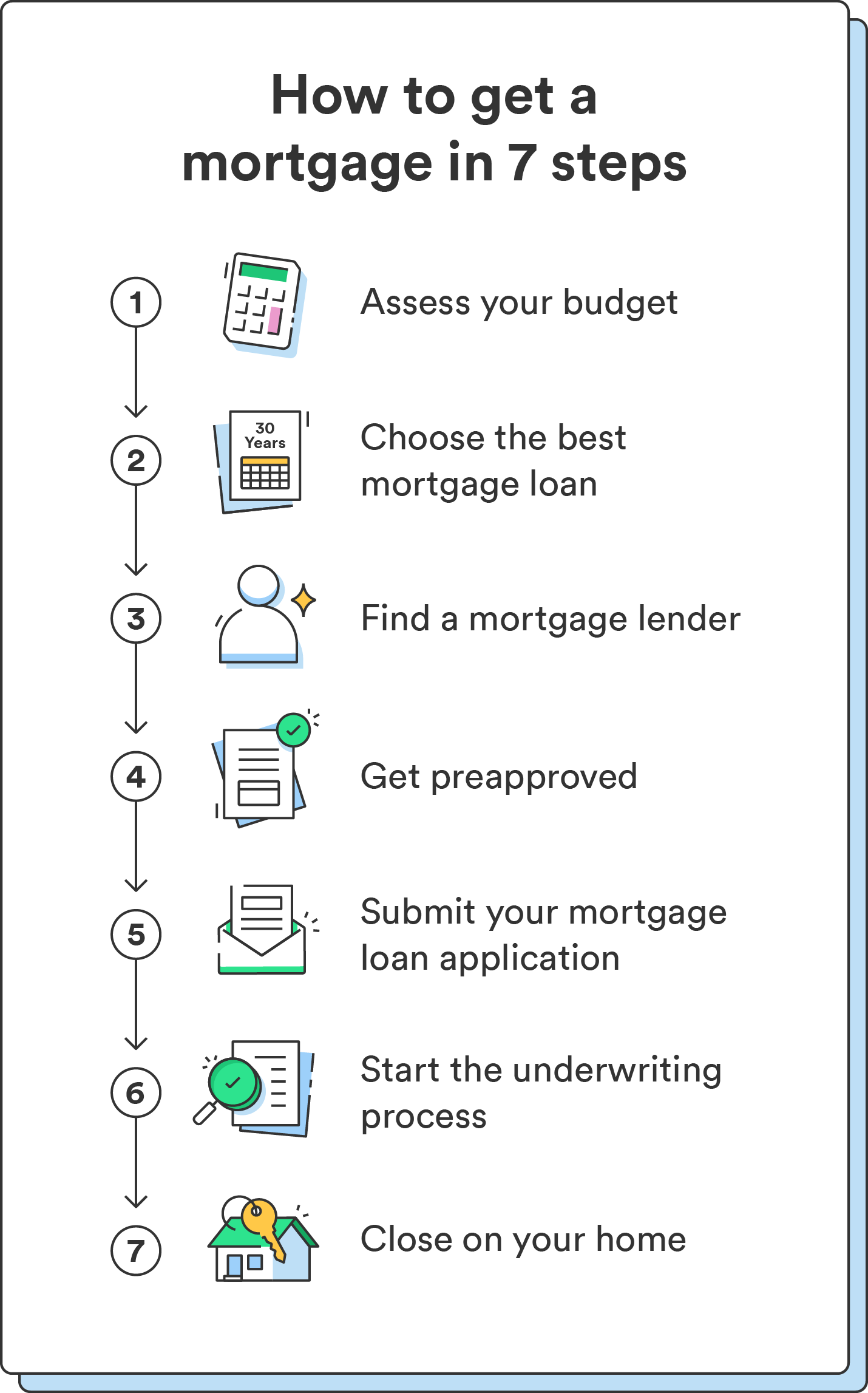

Securing a mortgage is arguably the most significant financial commitment the average person will make in their lifetime. It is a long-term contract that dictates your monthly cash flow, your tax obligations, and your ability to build equity in an asset. However, the modern financial market is no longer a monolithic entity where your only option is the brick-and-mortar bank on the corner.

Today, the “where” of getting a mortgage is just as important as the “how much.” The landscape has diversified into a complex ecosystem of traditional banks, member-owned credit unions, specialized online lenders, and independent brokers. Each of these avenues offers distinct advantages and potential drawbacks depending on your credit profile, your financial goals, and your preference for digital versus personal interaction. This guide explores the primary categories of mortgage providers to help you determine which financial partner is best suited for your homeownership journey.

Traditional Banking Institutions: The Reliability of Established Lenders

For many borrowers, the first thought when considering a mortgage is their primary checking or savings account provider. Traditional banks, ranging from global giants to regional players, remain a cornerstone of the mortgage industry. They offer a sense of security and a “one-stop-shop” convenience that is highly appealing to those who prefer to keep their financial life centralized.

National Banks: Convenience and Integrated Services

Large-scale national banks often have robust mortgage departments capable of handling a high volume of loans. The primary advantage here is integration. If you already have your salary deposited and your bills paid through a major bank, applying for a mortgage there can be streamlined. These institutions often offer “relationship discounts,” such as a reduction in origination fees or a slightly lower interest rate for existing customers with significant assets.

However, the downside of national banks can be their rigidity. Because they handle thousands of applications, their underwriting processes are often highly automated and strictly governed by “boxes.” If your financial situation is non-traditional—perhaps you are a high-net-worth individual with complex tax returns or a freelancer with fluctuating income—you might find the “big bank” bureaucracy difficult to navigate.

Community Banks and Local Institutions: Personalized Service

If the cold automation of a national bank feels unappealing, community banks offer a compelling alternative. These institutions are often more invested in the local economy and may have a more nuanced understanding of the local real estate market.

Community banks often provide a more personalized underwriting experience. In some cases, they may practice “portfolio lending,” meaning they keep the mortgage on their own books rather than selling it to the secondary market. This gives them more flexibility to approve borrowers who might fall slightly outside the standard lending criteria but are otherwise financially sound.

Credit Unions: The Member-Centric Alternative

Credit unions are non-profit financial cooperatives owned by their members. Because they do not have to answer to external shareholders demanding quarterly profits, they can often return value to their members in the form of better rates and lower fees. This makes them one of the most cost-effective places to get a mortgage.

Lower Interest Rates and Fees

In the realm of personal finance, even a 0.25% difference in an interest rate can equate to tens of thousands of dollars saved over the life of a 30-year loan. Credit unions are frequently able to undercut traditional banks on interest rates. Additionally, because their goal is member service rather than profit maximization, their closing costs and origination fees are often significantly lower.

Many credit unions also offer specialized programs for first-time homebuyers, such as low-down-payment options that do not require private mortgage insurance (PMI). These products are designed to build community wealth rather than maximize lender revenue.

Localized Lending Decisions and Membership Requirements

The trade-off for these benefits is the membership requirement. To get a mortgage from a credit union, you must be a member, which usually requires living in a certain geographic area, working in a specific industry, or belonging to a particular organization.

While their technology might not always be as flashy as a Silicon Valley-backed fintech firm, credit unions excel in human interaction. When you call a credit union about your mortgage, you are often speaking to a person in your own community who has a vested interest in your financial success.

Non-Bank Mortgage Lenders and Online Platforms

In the last decade, non-bank lenders have revolutionized the mortgage industry. These are companies that focus exclusively on lending, without the traditional deposit and checking services of a bank. Many of these operate primarily or exclusively online, leveraging technology to speed up the approval process.

The Rise of Direct Lenders

Direct lenders like Rocket Mortgage or Better.com have captured a massive share of the market by focusing on the “frictionless” experience. For a tech-savvy borrower who wants to upload documents at 2:00 AM and receive a pre-approval letter within minutes, these platforms are ideal. They use sophisticated algorithms to verify income, employment, and assets almost instantaneously.

These lenders are often very competitive on pricing because they do not have the overhead costs of maintaining physical branches. They are also highly efficient at closing loans quickly, which can be a significant advantage in a competitive “seller’s market” where a fast closing period can make your offer more attractive.

Digital Speed and Specialized Technology

The primary benefit of an online-only lender is transparency and speed. Most offer dashboards where you can see exactly where your application stands in the pipeline. However, the lack of a physical presence can be a drawback for complex transactions. If a problem arises during the appraisal or title search, you may find yourself stuck in a call-center loop rather than being able to sit down with a loan officer to resolve the issue.

Furthermore, some online lenders may lure borrowers with low “headline” rates but make up the difference with higher administrative fees. It is crucial to look at the Loan Estimate (LE) document carefully to compare the total cost of credit.

Mortgage Brokers: Your Personal Intermediary

While banks and direct lenders are “retail” outlets for mortgages, a mortgage broker acts as a “wholesale” intermediary. A broker does not lend their own money; instead, they have access to a network of dozens of different lenders and “shop” your application to find the best deal.

Access to a Wider Product Range

The greatest strength of a mortgage broker is variety. While a single bank can only offer you the products they have in-house, a broker can look at products from 20 different sources. This is particularly beneficial for:

- Self-employed borrowers: Brokers know which lenders are “freelancer-friendly.”

- Investors: They can find lenders who specialize in multi-family or rental properties.

- Borrowers with lower credit scores: Brokers know which niche lenders are willing to take on more risk for a higher price.

Saving Time and Reducing Stress

Navigating the mortgage market is a full-time job. A good broker handles the heavy lifting—they collect your paperwork once and then use it to apply to multiple lenders. They understand the nuances of various loan programs (FHA, VA, Conventional, USDA) and can advise you on which one aligns with your five-year or ten-year financial plan.

The caveat is that brokers are paid via commissions, usually by the lender. While this means the service is often “free” to the borrower, you should ensure that the broker is incentivized by your best interest rather than the lender offering the highest kickback. Always ask for a breakdown of how they are compensated.

Making the Choice: How to Evaluate Your Mortgage Options

Identifying “where” to get a mortgage is only the first step; the final step is performing a rigorous financial analysis of the offers you receive. To choose the right lender, you must look beyond the monthly payment and examine the total cost of the debt.

Interest Rates vs. Annual Percentage Rates (APR)

When comparing lenders, always look at the APR rather than just the interest rate. The interest rate is the cost of borrowing the principal, but the APR includes the interest rate plus other costs such as points, mortgage insurance, and loan origination fees. The APR provides a more “apples-to-apples” comparison of what you are actually paying for the loan.

If Lender A offers a 6.0% rate with $5,000 in fees and Lender B offers a 6.2% rate with $0 in fees, Lender B might actually be the better financial choice if you plan to move in five years, whereas Lender A might be better if you stay for thirty.

Customer Support and Closing Timelines

In personal finance, time is often money. If a lender offers a slightly lower rate but has a reputation for missing closing dates, it could cost you the house entirely or result in expensive “lock-in” extensions. Research the lender’s reputation for communication and reliability.

Before committing, ask three key questions:

- What is your average “time to close” for this type of loan?

- Will my loan be serviced in-house, or will it be sold to another company? (Knowing who you will be making payments to for the next 30 years is vital).

- Can you provide a detailed breakdown of all third-party fees?

By carefully weighing the stability of traditional banks, the cost-savings of credit unions, the speed of online lenders, and the variety offered by brokers, you can secure a mortgage that doesn’t just put a roof over your head, but serves as a solid foundation for your overall financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.