For veterans, active-duty service members, and eligible surviving spouses, the VA home loan program stands as one of the most significant financial benefits earned through military service. However, in a volatile economic environment, the question of “what is the current VA mortgage rate” is rarely met with a single, static number. Instead, the answer is a moving target influenced by global bond markets, federal monetary policy, and individual financial profiles.

Understanding the nuances of VA mortgage rates is essential for any eligible borrower looking to maximize their purchasing power. Unlike conventional loans, VA loans offer unique advantages—such as zero down payment requirements and no private mortgage insurance (PMI)—but they are still subject to the ebbs and flows of the broader financial sector. This article explores the current state of VA mortgage rates, the factors that drive them, and strategies to secure the most competitive terms possible.

Understanding VA Mortgage Rates in Today’s Economy

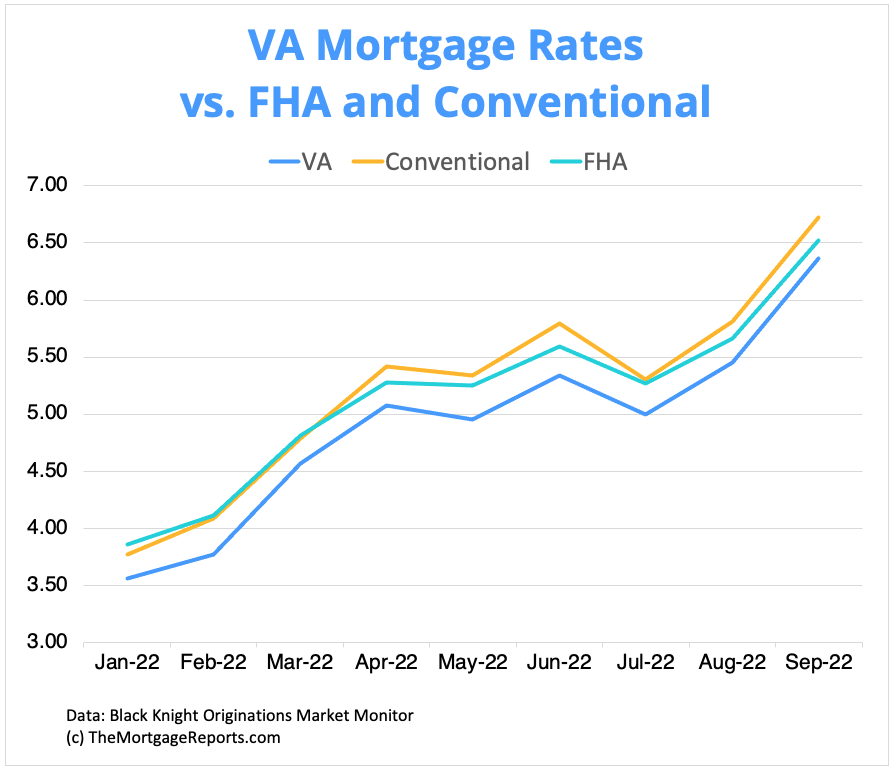

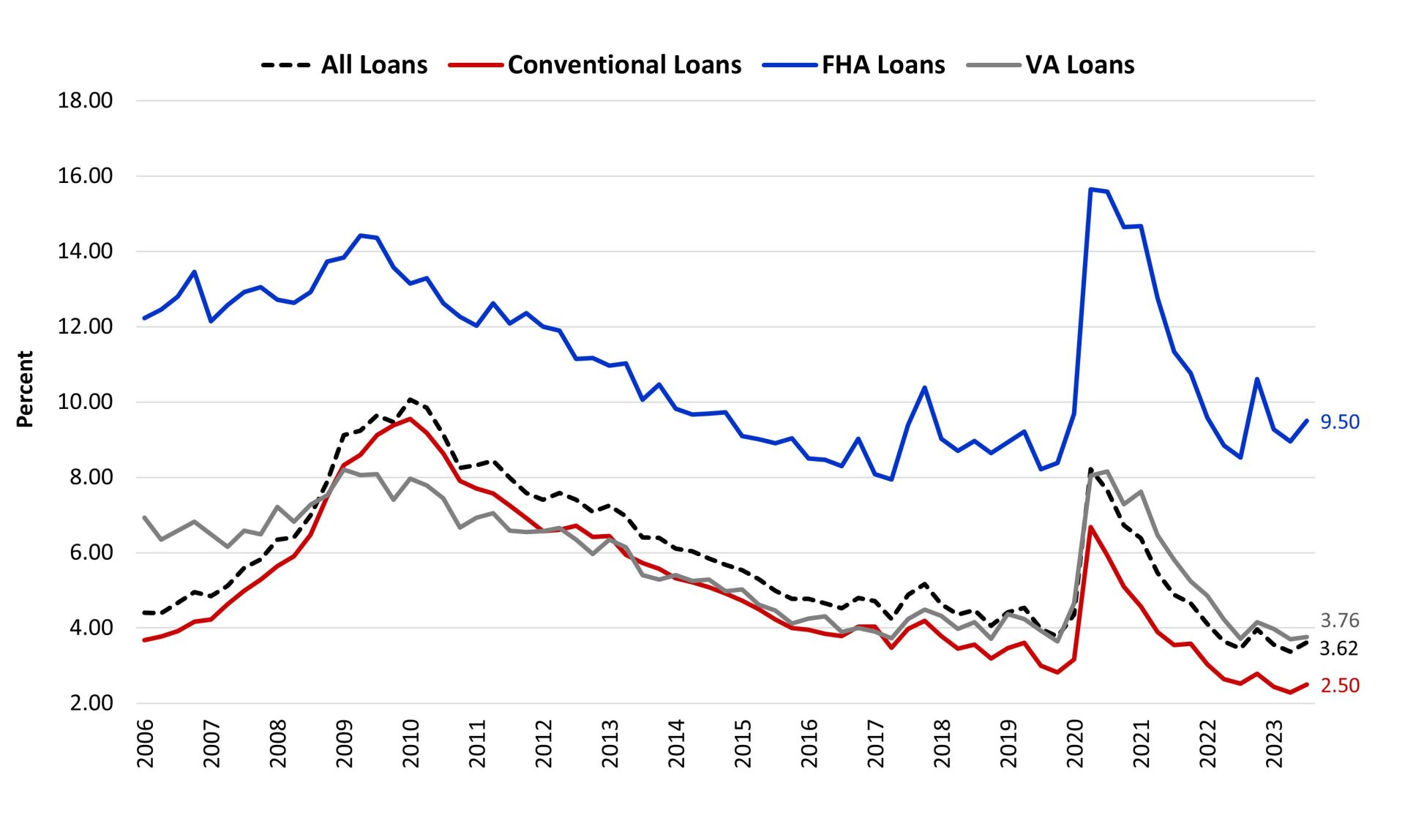

To understand where VA mortgage rates sit today, one must first understand that the Department of Veterans Affairs does not set the interest rates. Instead, private lenders—banks, credit unions, and mortgage companies—set these rates based on the secondary market. VA rates are typically lower than conventional mortgage rates, often by 0.25% to 0.50%, because the government guarantees a portion of the loan, reducing the risk for the lender.

How VA Rates Differ from Conventional Rates

The inherent “safety” of the VA guarantee allows lenders to offer more aggressive pricing. In a market where conventional 30-year fixed rates might hover around 7%, it is common to see VA rates in the mid-to-high 6% range. This spread exists because the VA’s backing acts as a safety net; if a borrower defaults, the government compensates the lender for a portion of the loss. This structural advantage makes the VA loan one of the most cost-effective “Money” tools available to the military community.

The Role of the Federal Reserve and Bond Markets

While the Federal Reserve does not directly set mortgage rates, its influence is absolute. When the Fed adjusts the federal funds rate to combat inflation, it ripples through the economy. Mortgage rates are more closely tied to the yield on the 10-Year Treasury Note. When investors are confident in the economy, they move money into stocks, causing bond yields (and mortgage rates) to rise. Conversely, in times of economic uncertainty, investors flock to the safety of bonds, which can drive rates down. Currently, as the market balances inflation concerns with growth projections, VA mortgage rates remain sensitive to every Consumer Price Index (CPI) report.

Factors That Influence Your Personal VA Interest Rate

Even when “market rates” are quoted in the news, your specific offer will vary. Lenders use a process called “risk-based pricing” to determine the exact rate they are willing to offer you. While the VA program is more lenient than conventional programs, your financial health still dictates the final percentage on your Closing Disclosure.

Credit Score and Debt-to-Income (DTI) Ratios

The VA does not technically require a minimum credit score, but most lenders do. This is known as a “lender overlay.” Typically, a score of 620 or higher is required to access the most competitive rates. Borrowers with scores above 740 often see the lowest possible rates. Similarly, your Debt-to-Income (DTI) ratio—the percentage of your monthly income that goes toward debt—affects your perceived risk. While the VA is flexible with high DTI ratios (often allowing up to 41% or even higher with compensating factors), a lower DTI can sometimes help in securing a better rate or a larger loan amount.

Loan Term and Down Payment Options

The duration of your loan significantly impacts the interest rate. A 15-year fixed-rate VA loan will almost always carry a lower interest rate than a 30-year fixed-rate loan because the lender is exposed to interest-rate risk for a shorter period. Additionally, although the VA loan allows for 0% down, putting money down can occasionally lower your rate or, at the very least, reduce the total amount of interest you will pay over the life of the loan.

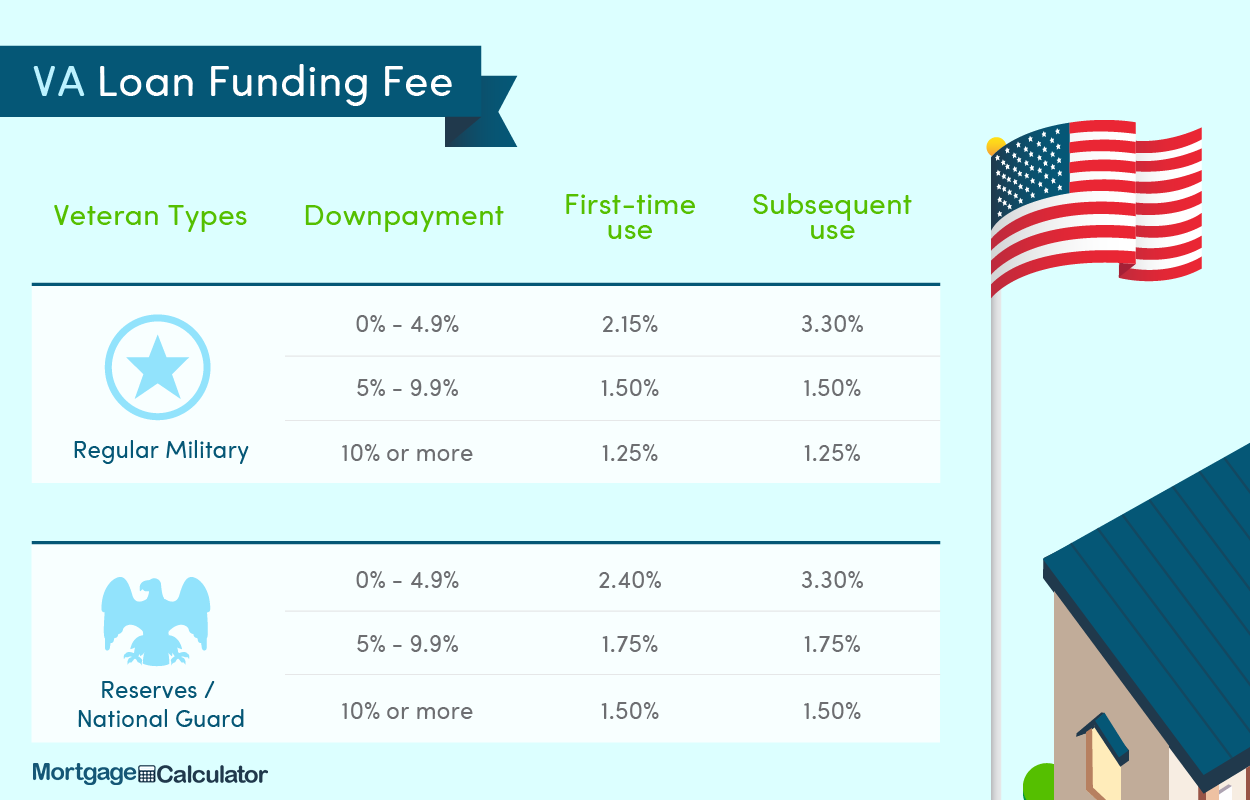

The Impact of the VA Funding Fee

While not an interest rate per se, the VA Funding Fee is a critical “Money” component of the transaction. This is a one-time fee paid to the VA to support the program. The fee varies based on your down payment amount and whether it is your first time using the benefit. For first-time users with zero down, the fee is currently 2.15% of the loan amount. While this can be rolled into the loan, doing so increases your principal balance, which in turn increases the total interest paid over time.

Comparing VA Rates: Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

When researching current rates, borrowers must decide between the predictability of a fixed rate and the potential short-term savings of an Adjustable-Rate Mortgage (ARM).

The Stability of 15-year and 30-year Fixed Rates

The 30-year fixed-rate VA loan is the gold standard for veteran homeownership. It offers a set monthly payment that never changes, providing a hedge against future inflation. In an environment where rates are expected to remain “higher for longer,” locking in a fixed rate provides psychological and financial security. The 15-year fixed rate, while requiring higher monthly payments due to the shorter amortization schedule, allows the borrower to build equity twice as fast and usually saves tens of thousands of dollars in interest.

When Does a VA ARM Make Sense?

A VA ARM typically offers a lower initial interest rate for a set period (usually 3, 5, or 7 years). After this period, the rate adjusts annually based on market indices. In a high-rate environment, an ARM can be a strategic move if the borrower plans to sell the home or refinance before the introductory period ends. However, this carries the risk of the rate adjusting upward if market conditions worsen. For those prioritizing “Money” management and liquidity, an ARM requires a careful exit strategy.

Strategies to Secure the Best VA Mortgage Rate

Securing the best rate is not a passive process; it requires active financial management and a willingness to shop around. Because VA loans are a specialized product, not all lenders offer the same terms.

Shopping Around: The Importance of Lender Comparisons

Many veterans make the mistake of going with the first lender that sends them a mailer. However, “par rates” (the base interest rate before points) can vary significantly between a local credit union, a national bank, and a specialized online VA lender. By obtaining at least three Loan Estimates, a borrower can leverage competition to drive down the rate or the lender’s origination fees. Even a 0.125% difference in interest rate can save thousands of dollars over the life of a $400,000 mortgage.

Buying Down the Rate with Discount Points

In the mortgage world, you can “buy” a lower interest rate by paying “points” at closing. One point is equal to 1% of the loan amount. For example, on a $300,000 loan, one point costs $3,000. Paying this upfront might lower your interest rate by 0.25%. The key is calculating the “break-even point”—the amount of time it takes for the monthly savings to exceed the upfront cost. If you plan to stay in the home for a decade or more, buying points is often a wise investment of capital.

Improving Your Financial Profile Before Applying

In the months leading up to a home purchase, prospective borrowers should focus on “financial grooming.” This includes avoiding new credit inquiries, paying down revolving credit card balances to lower utilization, and ensuring all bills are paid on time. A modest 20-point increase in a credit score can sometimes move a borrower into a different pricing tier, resulting in a lower interest rate and lower monthly payments.

The Future Outlook for VA Mortgage Rates

As we look toward the remainder of the fiscal year, the trajectory of VA mortgage rates will be dictated by the tug-of-war between economic growth and inflationary pressures.

Inflationary Pressures and Housing Market Trends

If inflation continues to cool, the market anticipates that the Federal Reserve may eventually pivot toward cutting interest rates. This would likely lead to a gradual decline in VA mortgage rates. However, if the labor market remains overheated and inflation stays “sticky,” rates could plateau or even see minor increases. For the “Money”-conscious veteran, staying informed on the monthly CPI and jobs reports is vital for timing a purchase or a refinance.

Long-term Planning for Veteran Homeowners

Ultimately, the “current” rate is only one part of the equation. Homeownership is a long-term wealth-building strategy. Even if rates are higher today than they were during the historic lows of 2020 and 2021, the VA loan remains a powerful tool for building equity and securing a primary residence. For those who buy now at a higher rate, the VA Interest Rate Reduction Refinance Loan (IRRRL)—often called a “VA Streamline”—provides a simplified way to lower the rate in the future if market conditions improve.

In conclusion, while the current VA mortgage rate is influenced by complex macroeconomic factors, the eligible borrower has significant control over their final terms. By maintaining a strong credit profile, shopping across multiple lenders, and understanding the mechanics of the VA loan program, veterans can ensure they are getting the maximum value from the benefits they have earned. Homeownership is a cornerstone of personal finance, and the VA loan remains one of the most effective vehicles to achieve it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.