Determining exactly “how much Amazon is worth” is a task that requires looking beyond a single number. While a quick search might reveal a market capitalization hovering between $1.5 trillion and $2 trillion depending on the day’s trading, the true financial worth of Amazon.com, Inc. is a complex tapestry woven from diverse revenue streams, massive infrastructure investments, and aggressive future-leaning bets. For investors, financial analysts, and business enthusiasts, understanding Amazon’s valuation is an exercise in evaluating one of the most successful capital allocation stories in corporate history.

Understanding Amazon’s Market Capitalization

To answer the question of Amazon’s worth, one must first look at its market capitalization—the total dollar market value of a company’s outstanding shares of stock. Market cap is the most common metric used by the financial community to rank the size of public companies.

How Market Cap is Calculated and Tracked

Market capitalization is calculated by multiplying the current stock price by the total number of outstanding shares. Because Amazon (trading under the ticker AMZN on the NASDAQ) is a highly liquid stock, its valuation fluctuates every second during trading hours. Investors track these changes not just to see the daily price movement, but to understand how the market perceives the company’s long-term earnings potential. When the market cap rises, it signals investor confidence in Amazon’s ability to generate future cash flows; when it dips, it often reflects macroeconomic concerns like interest rate hikes or slowing consumer spending.

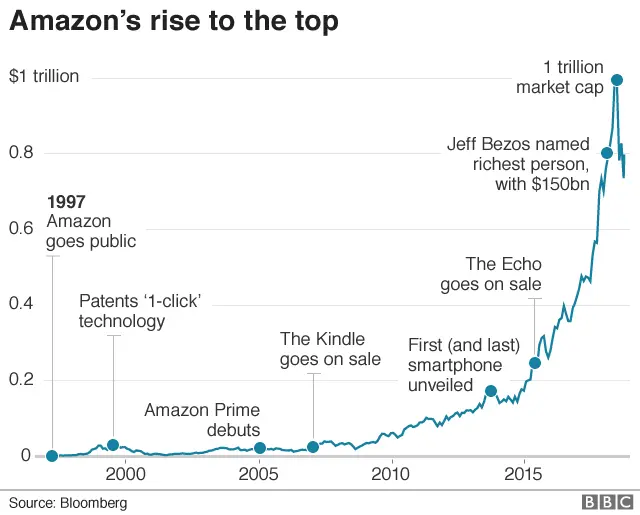

Historical Growth and the Trillion-Dollar Club

Amazon’s journey to its current valuation is a study in exponential growth. After going public in 1997 at a split-adjusted price of pennies, the company took over two decades to reach the $1 trillion market cap milestone in 2018. It was the second U.S. company ever to do so, following Apple. Since then, it has frequently traded in the “Big Tech” tier alongside Microsoft, Alphabet, and NVIDIA. This historical context is vital because it shows that Amazon’s worth is built on a foundation of “Day 1” philosophy—reinvesting nearly all profits back into the business to compound value over decades rather than quarters.

Factors Influencing Daily Stock Fluctuations

While the long-term trend has been upward, Amazon’s daily worth is sensitive to several variables. These include quarterly earnings reports, changes in consumer price indices (CPI), and shifts in Treasury yields. As a “growth stock,” Amazon’s valuation is heavily influenced by the “cost of money.” When interest rates are low, the future cash flows of a company like Amazon are discounted less severely, leading to a higher present valuation. Conversely, in high-interest environments, the market often reprices these stocks downward.

Revenue Streams and Profitability Drivers

To understand why Amazon is worth trillions, one must dissect the engines that drive its top and bottom lines. Amazon is no longer just “the everything store”; it is a conglomerate of high-margin services and capital-intensive logistics.

E-commerce vs. AWS: The Margin Disparity

The most significant distinction in Amazon’s valuation is the difference between its North American and International retail segments and Amazon Web Services (AWS). While the retail side generates the lion’s share of total revenue, it often operates on razor-thin margins due to the immense costs of shipping, fulfillment, and labor.

In contrast, AWS—the cloud computing arm—is the company’s profit engine. AWS consistently delivers operating margins in the 25% to 30% range. From a “Money” perspective, analysts often value AWS as a standalone entity that could be worth $500 billion to $1 trillion on its own. The cloud segment provides the reliable cash flow that allows Amazon to experiment in other sectors, such as satellite internet (Project Kuiper) or healthcare.

Advertising: The Secret Growth Engine

In recent years, a third pillar has emerged that significantly boosts Amazon’s valuation: digital advertising. Amazon has become the third-largest advertising platform in the world, behind only Google and Meta. Unlike the retail business, advertising has very low overhead and extremely high margins. By leveraging its vast trove of first-party consumer data, Amazon allows sellers to promote products directly at the point of purchase. This high-margin revenue stream has been a primary catalyst for the stock’s recent valuation premiums, as it adds a layer of profitability that traditional retail cannot match.

Subscription Services and Prime’s Recurring Revenue

Amazon Prime is a masterclass in building “sticky” revenue. With over 200 million members globally, the subscription fees provide a predictable, recurring income stream that helps stabilize the company’s balance sheet. More importantly, Prime members tend to spend significantly more on the platform than non-members. From a valuation standpoint, this creates a “moat”—a competitive advantage that protects the company’s market share and justifies a higher stock price multiple.

Key Financial Metrics for Investors

When assessing if Amazon is “worth” its current price, professional investors look past the headline numbers to specific financial ratios and health indicators.

Price-to-Earnings (P/E) and Forward P/E Ratios

Amazon has historically traded at a much higher P/E ratio than the broader market. This is because the company deliberately depresses its earnings by reinvesting heavily in R&D and infrastructure. Therefore, looking at a trailing P/E ratio can be misleading. Instead, many institutional investors look at “Forward P/E,” which estimates earnings over the next 12 months. If the Forward P/E is significantly lower than the trailing P/E, it suggests that the market expects Amazon’s profitability to catch up with its massive scale.

Free Cash Flow: The Metric Jeff Bezos Prized

For years, Amazon’s founder, Jeff Bezos, emphasized Free Cash Flow (FCF) per share as the ultimate measure of the company’s value. FCF is the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. Unlike “net income,” which can be manipulated by accounting practices, FCF provides a clear picture of the actual cash available to be returned to shareholders or reinvested. For an investor, a growing FCF is the strongest indicator that Amazon’s business model is sustainable and that its intrinsic worth is increasing.

Debt-to-Equity and Balance Sheet Strength

A company’s worth is also defined by what it owes. Amazon maintains a robust balance sheet with significant cash reserves, which allows it to weather economic downturns and make strategic acquisitions (like Whole Foods or MGM Studios). Its debt-to-equity ratio is generally kept at a level that maintains an investment-grade credit rating. This financial stability reduces the risk for shareholders and allows the company to borrow money at lower interest rates, further fueling its growth.

Future Valuation Drivers and Risks

The future “worth” of Amazon will be determined by its ability to capitalize on emerging technologies while navigating a complex regulatory environment.

The Impact of Artificial Intelligence on AWS Growth

The current frontier for Amazon’s valuation is Generative AI. As businesses look to integrate AI into their operations, they require the massive computing power that AWS provides. Amazon’s investment in its own AI chips (Trainium and Inferentia) and its partnership with companies like Anthropic are designed to ensure it remains the backbone of the AI era. If Amazon can successfully position AWS as the “AI utility” of the future, its valuation could see another massive leg up.

Regulatory Risks and Antitrust Concerns

One of the primary “bears” in the valuation story is the threat of government intervention. Antitrust regulators in the U.S. and Europe have frequently scrutinized Amazon’s market dominance. There is ongoing debate about whether Amazon should be forced to split its retail business from its logistics or cloud businesses. While a forced breakup sounds negative, some financial analysts argue that a “sum-of-the-parts” valuation would actually reveal that the individual pieces of Amazon are worth more separately than they are combined, potentially unlocking value for shareholders.

Expansion into Healthcare and Fintech

Amazon continues to look for “unsolved” markets to enter. Its acquisition of One Medical and the launch of Amazon Pharmacy signal a serious intent to disrupt the multi-trillion-dollar healthcare industry. Similarly, its expansion into payment processing and “buy now, pay later” services positions it as a growing force in fintech. Every successful foray into a new sector adds to the “optionality” of the stock—the idea that you are buying not just a retail company, but a call option on the future of several major global industries.

In summary, the question of “how much Amazon is worth” is answered by its $1.8 trillion market cap, but it is explained by its unparalleled dominance in cloud computing, its burgeoning advertising business, and its relentless focus on long-term cash flow. For the modern investor, Amazon represents more than just a company; it represents a diversified portfolio of high-growth businesses consolidated under a single ticker. As long as it continues to innovate and expand its margins, its financial worth is likely to remain on an upward trajectory, cementing its status as a cornerstone of the global economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.