Gift cards, ubiquitous in modern commerce, represent a powerful yet often underutilized financial tool. While seemingly simple, managing these pre-paid instruments effectively is a critical aspect of sound personal finance, ensuring you extract maximum value and avoid unnecessary loss. This article delves into the practical methods for checking your gift card balance and, more importantly, frames this seemingly basic task within the broader context of intelligent money management. By understanding and consistently applying these strategies, you can transform a simple piece of plastic or a digital code into a genuine asset, rather than a forgotten liability.

The Financial Prudence of Tracking Gift Card Balances

In the landscape of personal finance, every dollar counts, whether it’s in your bank account, invested, or stored on a gift card. Neglecting to track gift card balances is akin to leaving cash lying around—it’s prone to being forgotten, misplaced, or expiring without being utilized. Proactive management of gift cards is not just about convenience; it’s a strategic move that directly impacts your spending power and overall financial health.

Preventing Lost Value and Maximizing Utility

One of the most compelling reasons to regularly check your gift card balance is to prevent the loss of value. Gift cards, unlike cash, often come with expiration dates, dormancy fees, or specific usage restrictions. An unknown balance is an unspent balance, making it vulnerable to these financial traps. By staying informed, you ensure that every cent loaded onto a card is available for your use, effectively extending your budget and reducing potential waste. This vigilance turns a potential liability into a valuable asset, allowing you to strategically deploy these funds for planned purchases or unexpected needs.

Furthermore, knowing your balance empowers you to maximize the utility of the card. A small remaining balance on one card might not be enough for a significant purchase, but when combined with another card or a small cash addition, it can cover a desired item. This micro-management of smaller sums contributes to a larger picture of efficient resource allocation, preventing those awkward moments at the checkout where you realize you don’t quite have enough, and the card is then set aside and forgotten.

Budgeting, Planning, and Financial Awareness

Integrating gift card balances into your financial planning enhances your overall budgeting capabilities. If you have a gift card for a grocery store, that’s effectively pre-paid grocery money. Knowing its exact balance allows you to factor it into your weekly or monthly food budget, freeing up cash for other expenses or savings goals. Similarly, a gift card for a specific retailer can offset discretionary spending, making your overall budget more robust and flexible.

This level of awareness fosters better financial habits. It encourages you to think about all your available resources, not just the liquid cash in your bank account. It trains you to be more deliberate about spending and to account for all forms of currency at your disposal. This disciplined approach is a cornerstone of effective personal finance, leading to greater control and less financial stress. It’s about seeing the full picture of your purchasing power and planning accordingly, rather than being surprised by forgotten funds or expired cards.

Avoiding Expiry Traps and Dormancy Fees

Gift card terms and conditions can be complex and vary significantly between issuers and retailers. Expiration dates are a common pitfall, especially for cards received months ago. Many state laws provide some protection, but federal law only mandates that funds on retail gift cards cannot expire for five years, and even then, dormancy fees can begin after one year of inactivity.

Dormancy fees, often deducted monthly after a period of non-use, are another insidious way gift card value erodes. A forgotten $20 card can quickly diminish to nothing if not used. Regularly checking your balance is your primary defense against these charges. It prompts you to use the card before fees kick in or before the entire value is lost to an expiration date. This proactive approach saves you money that would otherwise be forfeited, keeping more of your hard-earned (or gifted) funds in your pocket. It’s a fundamental aspect of protecting your financial assets, no matter how small they may seem individually.

Common Methods for Checking Gift Card Balances

While the precise steps may vary slightly depending on the issuer, there are several universally accepted and accessible methods for checking a gift card’s balance. Understanding these options ensures you can always access your financial information promptly and efficiently, regardless of the card type or retailer.

Online Portals and Retailer Websites

The most prevalent and often most convenient method for checking a gift card balance is through the retailer’s dedicated website. Most major retailers and gift card issuers provide an online portal specifically for this purpose.

Step-by-Step Online Verification

- Locate the Website: Typically, the back of the physical gift card or the digital email will direct you to the appropriate URL (e.g., “visit [retailer].com/giftcard”).

- Find the Balance Check Feature: Look for a section labeled “Check Balance,” “Gift Card Balance,” or similar. This is often found in the footer of the website, under “Customer Service,” or within a dedicated gift card section.

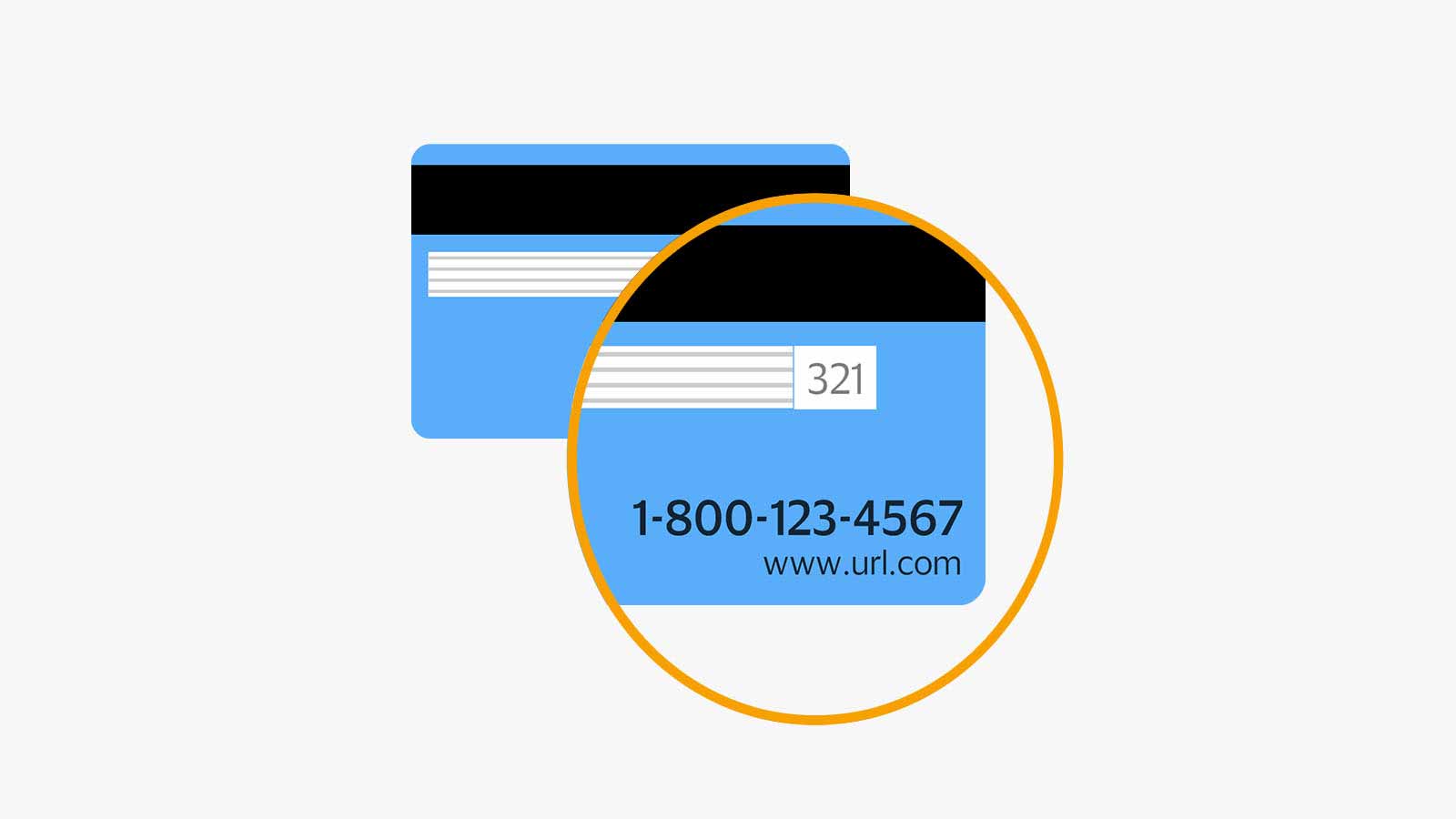

- Enter Card Details: You will usually need to input the gift card number (typically 12-19 digits) and a PIN (Personal Identification Number). The PIN is usually a shorter 3-4 digit code, often found under a scratch-off strip on physical cards for security.

- Submit and View: After entering the required information, the current balance will be displayed on the screen.

This method offers real-time updates and is accessible 24/7, making it ideal for pre-shopping checks or quick verification. It minimizes the need for direct interaction and provides instant financial clarity.

Customer Service Hotlines

For those who prefer verbal interaction or face challenges with online portals, calling the customer service hotline is a reliable alternative. Most gift cards have a toll-free number printed on the back.

Interacting with Customer Support

- Locate the Number: The 1-800 or 1-888 number is usually clearly printed on the reverse side of the gift card.

- Prepare Card Information: Have your gift card number and PIN ready before you call. This speeds up the process significantly.

- Follow Prompts: Upon calling, you will likely encounter an automated system. Listen carefully for options related to “gift card balance,” “account information,” or “customer service.”

- Speak to Representative (if needed): If the automated system doesn’t provide a direct balance check option, or if you encounter issues, you can usually opt to speak with a customer service representative who can assist you after verifying your card details.

While it might take slightly longer than an online check, customer service lines are invaluable for resolving more complex issues or getting clarification on terms and conditions, thereby safeguarding your financial interests.

In-Store Inquiries

Visiting a physical store location is another straightforward way to ascertain your gift card balance, particularly useful if you are already planning a trip to that retailer.

Point-of-Sale Verification

- Approach Customer Service/Cashier: Present your gift card to a cashier or customer service representative at any eligible store location.

- Request Balance Check: Simply ask them to check the balance on the card.

- Swipe or Scan: The employee will typically swipe the card through their point-of-sale (POS) system or manually enter the number.

- Confirm Balance: The balance will usually appear on their screen, and they can inform you verbally or print a receipt showing the amount.

This method is quick and requires no prior preparation beyond having the card itself. It’s particularly helpful if you’re unsure about the exact retailer or have multiple cards for the same brand. It also offers the immediate opportunity to use the balance for a purchase, seamlessly integrating financial checking with spending.

Mobile Apps and Digital Wallets

Many major retailers and gift card platforms now offer mobile apps that streamline the balance checking process, often integrating it with their loyalty programs or digital wallet features.

App-Based Management

- Download the App: Install the official app for the retailer or the gift card issuer on your smartphone.

- Add Gift Card: Look for a “Gift Card” or “Wallet” section within the app. You’ll typically have an option to “Add Gift Card” by scanning the barcode or manually entering the card number and PIN.

- View Balance: Once added, the balance will be displayed within the app, often alongside other stored payment methods. Some apps even allow you to manage multiple gift cards from various retailers.

Digital wallets like Apple Wallet, Google Pay, or specific retailer apps can store your gift card information, making it incredibly easy to track balances and use cards directly from your phone. This method enhances convenience, security, and integration with modern payment systems, offering a cutting-edge approach to managing your financial resources.

Maximizing the Value and Security of Your Gift Cards

Beyond simply knowing the balance, truly prudent financial management of gift cards involves strategic utilization and robust security practices. These measures ensure you not only use the cards but do so effectively, protecting your funds from loss or fraud.

Strategic Spending and Combination Strategies

Having a gift card balance is an opportunity to be strategic with your spending. Don’t rush to spend it on the first available item; instead, integrate it into your existing budget and financial goals.

Leveraging Gift Cards for Budgetary Advantage

- Planned Purchases: If you have a gift card for a store where you regularly shop for essentials (e.g., groceries, fuel), plan to use it for those specific budget categories. This effectively frees up cash in your regular bank account for savings, investments, or other discretionary spending.

- Offsetting Discretionary Spending: For non-essential retailers (e.g., clothing, electronics), use the gift card to cover items you might have otherwise purchased with cash or credit. This reduces your out-of-pocket expenses and helps maintain your spending discipline.

- Combining Cards: If you have multiple gift cards for the same retailer, or a small balance remaining on one, check if the retailer allows combining balances onto a single card or using multiple cards for a single transaction. This consolidates small, easily forgotten amounts into a more usable sum.

- Waiting for Sales: Unless there’s an impending expiration date, consider holding onto gift cards for upcoming sales or promotions at the respective store. This allows your gift card funds to stretch further, maximizing their purchasing power.

This strategic mindset transforms gift cards from mere payment methods into active components of your financial planning, helping you achieve your budgetary objectives more efficiently.

Safeguarding Your Gift Card Funds from Loss and Fraud

Gift cards, much like cash, are susceptible to theft and fraud, and once spent by an unauthorized party, they are often difficult to recover. Implementing simple security measures can provide significant protection for your financial asset.

Essential Security Practices

- Record Information: Immediately after receiving a gift card, make a record of the full card number, the PIN, the issuer’s customer service number, and the initial balance. Taking a photo of the front and back of the card and storing it securely (e.g., in a password-protected note, a secure digital wallet, or a dedicated spreadsheet) is an excellent practice. This information is crucial for reporting theft or loss.

- Treat Like Cash: Carry gift cards with the same care you would carry cash or a debit card. Avoid leaving them in easily accessible places, and don’t share their details with untrustworthy sources.

- Beware of Scams: Be vigilant against phishing emails, unsolicited calls, or online requests asking for your gift card numbers or PINs. Legitimate companies will rarely ask for this information outside of a direct transaction initiated by you. Gift cards are frequently targeted by scammers, who convert them into untraceable funds.

- Prompt Usage: The best way to secure your gift card funds is to use them promptly. The longer a card goes unused, the higher the risk of it being lost, stolen, or expiring. If you don’t plan to use it soon, consider spending it on a common necessity or consolidating it if possible.

By being proactive in documenting and securing your gift cards, you significantly reduce the risk of financial loss and ensure that the value remains available for your intended use.

Utilizing Remainder Balances and Secondary Markets

It’s common to have a small, awkward balance left on a gift card after a purchase—too little to buy much, but too much to simply discard. Smart financial management extends to these residual amounts.

Maximizing Every Last Penny

- Small Purchases: Use small remaining balances for low-cost items like a coffee, a snack, or a portion of a larger purchase. Every dollar used is a dollar saved from your liquid funds.

- Consolidation: Some retailers allow you to transfer a small remaining balance from one gift card to another, or even convert it into store credit, making it easier to manage. In some U.S. states, cash-out laws allow you to request a cash refund for small remaining balances, typically under $5 or $10, if the card was purchased in that state. Check local regulations.

- Secondary Marketplaces: For larger, unwanted gift cards, or those with significant remaining balances, consider selling them on reputable secondary gift card marketplaces (e.g., Raise, CardCash). While you won’t get the full face value, you’ll recover a significant percentage of the funds, converting an unwanted gift into usable cash, which is a financially savvy move. Ensure you use established and secure platforms to avoid fraud.

Every penny on a gift card represents potential purchasing power. By employing these strategies, you ensure that no value is left behind, contributing to your overall financial efficiency and helping you capture every possible saving.

Understanding Gift Card Terms and Conditions: The Financial Small Print

The fine print on a gift card is not just legalese; it’s a critical financial document outlining the parameters of its use. Overlooking these terms can lead to unexpected fees, denied transactions, or even the complete loss of the card’s value. A diligent approach to understanding these conditions is paramount to protecting your financial investment.

Expiration Policies and State-Specific Protections

While federal law mandates that funds on retail gift cards cannot expire for five years from the date of activation, individual state laws can offer additional, more protective clauses. It’s crucial to distinguish between the card itself expiring and the funds expiring. Often, the plastic card might have an “valid through” date, but the underlying funds remain accessible.

Navigating Expiry and Dormancy

- Federal vs. State Law: Be aware that the five-year federal minimum only applies to “retail gift cards.” Other types, like promotional cards, often have shorter lifespans. Check your specific state’s consumer protection laws, as many states (e.g., California, New York) have even stricter rules, sometimes prohibiting expiration dates entirely or allowing much longer periods.

- “Valid Through” Dates: If a physical card has a “valid through” date, it usually means the card itself needs to be replaced after that date, but the funds can often be transferred to a new card by contacting customer service. This is a crucial distinction that can save your balance.

- Promotional Cards: Be especially wary of promotional gift cards (e.g., “receive a $10 gift card with purchase”). These often have much shorter expiry windows (e.g., 30-90 days) and are not subject to the same federal protections. Use these immediately.

Understanding these nuances is key to preventing the premature loss of your gift card’s value. Always prioritize using cards with shorter or ambiguous expiry terms first.

Dormancy Fees and Activation Charges

Beyond expiration, dormancy fees pose another significant threat to your gift card balance. These are charges deducted from the card’s value if it remains unused for a certain period.

Mitigating Fee-Related Losses

- Dormancy Fee Triggers: Federal law allows dormancy fees to be charged only after 12 months of inactivity, and only if the fees and their conditions are clearly disclosed. Check your card’s terms for when these fees begin and how much they are. Some state laws prohibit dormancy fees altogether or impose longer grace periods.

- Activation Fees: Some gift cards, particularly those purchased from third-party retailers (e.g., grocery stores selling multi-brand cards), may have a small activation fee at the time of purchase. While usually paid by the purchaser, it’s good to be aware of how the initial balance is impacted.

- Service Fees: Less common but still possible, some cards might have other service fees (e.g., for balance inquiries via phone after a certain number of calls). Review the fine print for any such charges.

Regular balance checks are your best defense against dormancy fees, prompting you to use the card before its value is eroded. This proactive approach is a simple yet powerful financial habit.

Usage Restrictions and Retailer-Specific Limitations

Not all gift cards are created equal in terms of where and how they can be used. Understanding these restrictions prevents frustrating surprises at the checkout.

Navigating Usage Limitations

- In-Store vs. Online: Some gift cards are restricted to in-store purchases only, while others are primarily for online use. Confirm this before attempting a transaction.

- Specific Departments/Services: Occasionally, a gift card might be valid only for certain departments (e.g., not valid at the pharmacy within a grocery store) or specific services (e.g., not valid for salon services within a department store).

- Return Policies: If an item purchased with a gift card is returned, the refund typically goes back onto a gift card or store credit, not cash. Understand the retailer’s return policy for gift card purchases.

- International Use: Most store-specific gift cards are restricted to the country of purchase. If you received a card from an international relative, verify its usability in your region.

- Reloading Options: Some gift cards are reloadable, which can be a convenient feature for budgeting or as a recurring gift. Check if your card offers this option and if there are any associated fees.

Taking the time to review these terms upfront empowers you to use your gift card effectively and avoids unexpected financial complications. It’s an investment of minutes that can save you frustration and potential loss of value.

In conclusion, managing gift card balances is a straightforward yet essential component of comprehensive personal finance. By consistently employing the methods for checking balances, strategically utilizing your cards, safeguarding them against loss, and understanding their underlying terms, you transform these seemingly minor financial instruments into valuable assets that contribute positively to your overall financial well-being. It’s a testament to the fact that astute money management often begins with attention to the smallest details.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.