Understanding how to calculate loan payments is one of the most vital skills in personal finance. Whether you are considering a mortgage for a new home, a car loan, or a personal loan to consolidate debt, the ability to work out the math behind your monthly obligations empowers you to make informed decisions. Far too often, consumers focus solely on the monthly “sticker price” provided by a lender without understanding how interest, principal, and time interact to determine the total cost of credit.

By mastering the mechanics of loan payments, you move from being a passive borrower to an active financial strategist. This guide explores the foundational components of a loan, the mathematical formulas used to derive payments, and the strategic tools available to help you manage your debt effectively.

The Core Components of a Loan Payment

Before you can calculate a payment, you must understand the variables that influence the final number. Every standard installment loan is comprised of several moving parts that dictate how much you pay each month and how much you will pay over the life of the loan.

The Principal Balance

The principal is the original amount of money you borrow. If you take out a $30,000 car loan, your initial principal is $30,000. As you make payments, a portion of that money goes toward reducing this balance. The speed at which you reduce the principal directly affects how much interest is charged in subsequent periods, as interest is usually calculated based on the remaining balance.

Interest Rates and APR

The interest rate is the cost of borrowing the principal, expressed as a percentage. However, it is crucial to distinguish between the nominal interest rate and the Annual Percentage Rate (APR). While the interest rate covers the cost of the money itself, the APR includes the interest rate plus any lender fees or closing costs. When working out payments, the APR provides a more accurate picture of your actual monthly commitment and the total cost of the loan.

The Loan Term or Tenure

The term is the length of time you have to repay the loan, usually expressed in months or years. A shorter term, such as a 36-month auto loan, will result in higher monthly payments but lower total interest costs. Conversely, a 72-month loan will lower your monthly burden but significantly increase the amount of interest you pay over time. Understanding the trade-off between monthly affordability and long-term cost is the cornerstone of debt management.

The Mathematical Formula for Loan Amortization

While most people use digital calculators, understanding the underlying math provides a deeper insight into how loans work. Most consumer loans—such as mortgages and auto loans—are “amortized.” This means the payment is calculated so that the loan is paid off in full at the end of the term through equal periodic installments.

The Standard Amortization Equation

The formula to calculate a fixed monthly payment (M) is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]

In this formula:

- P = The principal loan amount.

- i = The monthly interest rate (annual rate divided by 12).

- n = The total number of months (loan term).

By looking at this equation, you can see that the monthly payment is highly sensitive to the interest rate (i) and the number of periods (n). Even a small increase in the interest rate can significantly inflate the monthly payment when applied over a long period.

Breaking Down a Sample Calculation

Let’s look at a practical example. Imagine you borrow $10,000 at a 6% annual interest rate for 5 years (60 months).

- Principal (P): $10,000

- Monthly Interest (i): 0.06 / 12 = 0.005

- Number of Months (n): 60

Plugging these into the formula, you would find that the monthly payment is approximately $193.33. In the early months of this loan, a larger portion of that $193.33 goes toward interest. As the principal balance decreases, the interest portion of the payment shrinks, and the amount applied to the principal grows. This shifting balance is what defines an amortization schedule.

Interest-Only vs. Fully Amortizing Payments

It is important to note that some loans, particularly in business or specific real estate contexts, may offer “interest-only” periods. In these cases, the calculation is simpler: (Principal × Annual Interest Rate) / 12. However, because you are not paying down the principal, the balance remains the same, and you will eventually face a “balloon payment” or a significant jump in monthly costs when the amortization phase begins.

Utilizing Digital Tools and Financial Software

In the modern era, you do not need to perform complex algebra by hand to work out your loan payments. A variety of high-powered tools can do the heavy lifting, allowing you to run multiple “what-if” scenarios in seconds.

The Power of Online Loan Calculators

Most financial institutions and independent financial education websites offer free loan calculators. These tools are invaluable because they allow you to adjust variables—like the down payment amount or the interest rate—to see how they impact your monthly budget. Sophisticated calculators also provide a full amortization table, showing you exactly how much of each payment goes toward interest versus principal over the entire life of the loan.

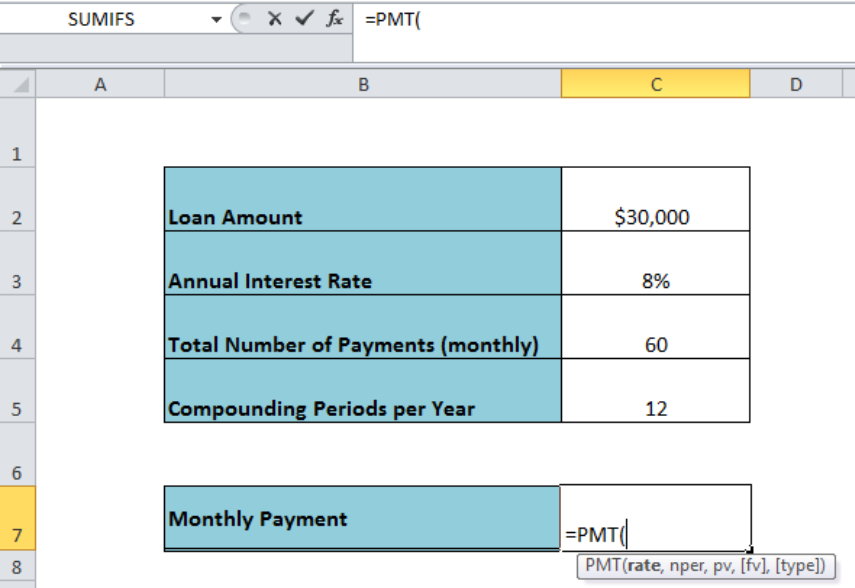

Using Spreadsheet Software (Excel and Google Sheets)

For those who want more control over their financial planning, spreadsheet software is the gold standard. Functions like =PMT(rate, nper, pv) in Excel can calculate payments instantly.

- rate: The interest rate for the period (e.g., 5%/12).

- nper: The total number of payment periods.

- pv: The present value, or the total principal.

Using spreadsheets allows you to build custom debt-reduction models. You can create a column for “Extra Payments” to see how adding an additional $50 or $100 a month can shave years off your loan term and save thousands in interest.

Mobile Financial Apps

There are numerous mobile apps designed specifically for debt management. These apps can sync with your bank accounts, track your current balances, and project your “debt-free date” based on your current payment trajectory. These tools are excellent for visual learners who benefit from charts and graphs showing their progress over time.

Understanding Different Loan Structures

Not all loans are created equal. Depending on the type of debt you are taking on, the way payments are calculated and applied may vary.

Fixed-Rate vs. Variable-Rate Loans

A fixed-rate loan maintains the same interest rate for the duration of the term, providing predictable monthly payments. This is the standard for most auto loans and many mortgages. A variable-rate (or adjustable-rate) loan, however, has an interest rate that can fluctuate based on market benchmarks like the Prime Rate. When working out payments for a variable loan, you must account for the “worst-case scenario” to ensure you can still afford the debt if rates rise.

The Reducing Balance Method

Most consumer loans use the reducing balance method, where interest is calculated on the remaining principal each month. This is the most consumer-friendly method because it rewards you for making extra payments. Every dollar you pay above the minimum reduces the principal, which in turn reduces the interest charged the following month.

Flat Rate Loans

Occasionally, usually in less regulated or short-term lending environments, you may encounter “flat rate” interest. Here, interest is calculated on the original principal for the entire term, regardless of how much you have paid back. This results in a much higher effective interest rate than a reducing balance loan. When working out payments for these, you simply take (Principal + Total Interest) and divide by the number of months. It is vital to recognize this structure, as it is often much more expensive for the borrower.

Strategic Planning and Debt Optimization

Working out your loan payment is only the first step. The ultimate goal of financial literacy is to use this information to minimize your costs and build wealth.

The Impact of Extra Principal Payments

One of the most effective ways to build equity and save money is to pay more than the minimum. By understanding your amortization schedule, you can see that even small, consistent extra payments in the early years of a loan have a massive compounding effect. Because you are bypassing the interest that would have been charged on that principal, you effectively “earn” a return on your money equal to the loan’s interest rate.

Refinancing Opportunities

By regularly recalculating your loan payments based on current market conditions, you can identify when it makes sense to refinance. If market interest rates drop or your credit score improves significantly, you may find that a new loan with a lower rate can reduce your monthly payment or allow you to shorten your term without increasing your monthly outlay.

The Importance of the Amortization Schedule

Always request or generate an amortization schedule before signing a loan agreement. This document is a roadmap of your debt journey. It shows you the “tipping point”—the moment when more of your payment goes toward principal than interest. For a 30-year mortgage, this point often doesn’t occur until mid-way through the loan. Knowing this helps you stay motivated and focused on long-term financial health.

In conclusion, working out payments on a loan is not merely an exercise in arithmetic; it is a fundamental component of strategic personal finance. By understanding the roles of principal, interest, and time, and by utilizing the tools available to model your debt, you gain the clarity needed to navigate the financial world with confidence. Whether you are paying off a small personal loan or managing a multi-decade mortgage, the math remains your most powerful ally in the pursuit of financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.