Determining the answer to “how much is a car” is a far more complex calculation than simply looking at a sticker in a dealership window. For the majority of households, a vehicle represents the second-largest financial commitment they will ever make, trailing only the purchase of a home. However, unlike a home, a car is a rapidly depreciating asset that demands constant capital infusion to remain functional.

To navigate this purchase through a financial lens, one must move beyond the initial transaction price and analyze the Total Cost of Ownership (TCO). This involves a deep dive into financing structures, depreciation curves, and the recurring operational expenses that can quietly erode a monthly budget. Whether you are looking at a budget-friendly sedan or a high-end luxury SUV, understanding the fiscal mechanics behind the purchase is essential for maintaining long-term financial health.

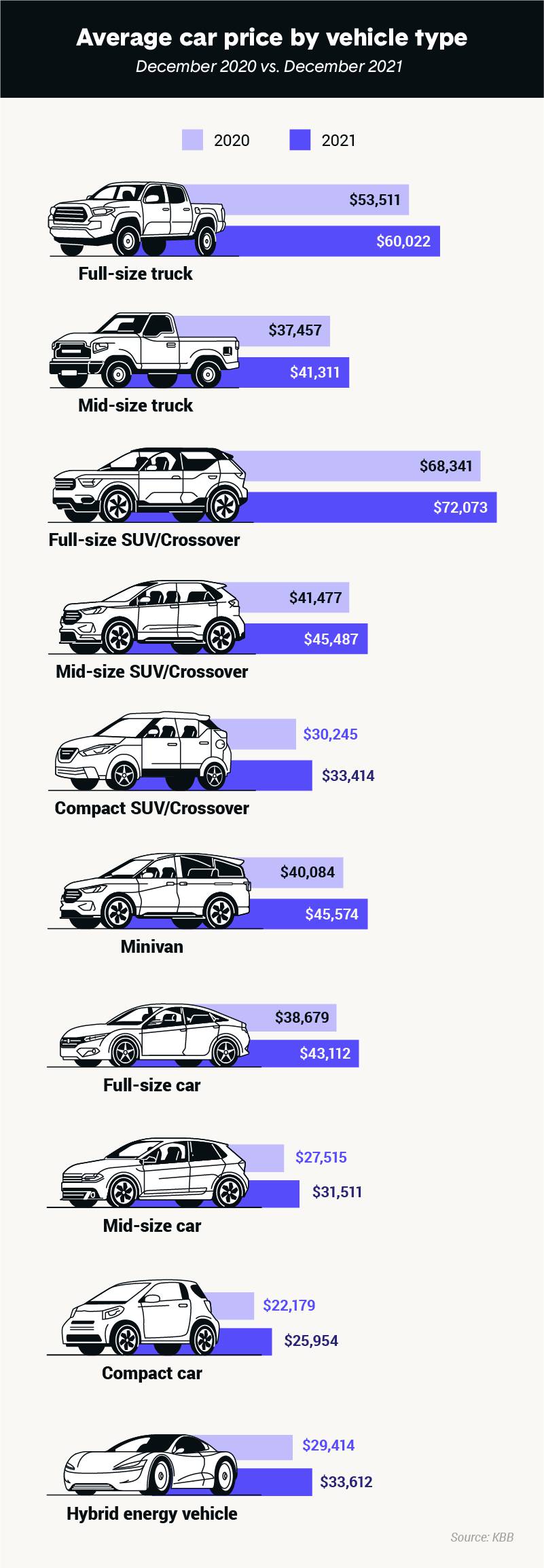

1. Decoding the Purchase Price: Beyond the Sticker

The Manufacturer’s Suggested Retail Price (MSRP) is often the starting point for negotiations, but it rarely represents the final “out-the-door” cost. From a financial perspective, the purchase price is a multifaceted figure influenced by market demand, inventory levels, and local regulatory fees.

The New vs. Used Financial Dilemma

Historically, the smartest financial move was to purchase a two-to-three-year-old vehicle to avoid the “drive-off-the-lot” depreciation hit, which can be as high as 20% in the first twelve months. However, recent shifts in the global supply chain have narrowed the price gap between new and used vehicles.

When analyzing the cost of a used car, you must factor in the “remaining useful life” of the asset. A $20,000 used car that requires $5,000 in immediate repairs is more expensive than a $24,000 new car with a comprehensive five-year warranty. From a personal finance standpoint, the goal is to find the “sweet spot” where the lower purchase price of a used vehicle outweighs the potential for increased maintenance costs and higher interest rates often associated with used car loans.

Taxes, Registration, and Hidden Dealer Fees

Many buyers fail to budget for the 8% to 12% in additional costs that are added to the sales price. These include:

- Sales Tax: Depending on your jurisdiction, this can add thousands to the total.

- Registration and Titling: State-mandated fees that vary significantly by region.

- Documentation Fees: The “doc fee” is essentially a processing fee charged by the dealer. While some states cap this at $100, others allow dealers to charge upwards of $800.

- Destination Charges: This is the cost of transporting the vehicle to the dealership, which is almost always passed on to the consumer.

2. The Ongoing Cost of Ownership: Budgeting for the Long Haul

Once the car is in your driveway, the true financial journey begins. The purchase price is a one-time hurdle, but the ownership costs are a marathon. To accurately answer “how much is for a car,” you must account for the monthly “burn rate” of the asset.

The Silent Killer of Wealth: Depreciation

Depreciation is arguably the most significant cost of car ownership, yet it is the one most often ignored because it isn’t a line item in a monthly budget. It is a “phantom cost” that only realizes itself when you go to sell or trade in the vehicle.

High-end luxury vehicles and certain electric vehicles (EVs) often suffer from steeper depreciation curves compared to reliable, high-demand economy brands. If you buy a $50,000 car and it is worth $25,000 three years later, that car cost you $8,333 per year in lost value alone—even before you paid for a single gallon of gas. Strategic buyers prioritize vehicles with high resale value to mitigate this wealth erosion.

Fuel, Maintenance, and the Variable Expense Trap

Operational costs are highly volatile. Fuel prices fluctuate with global markets, and maintenance costs tend to scale with the age and complexity of the vehicle.

- Predictive Maintenance: A modern vehicle requires oil changes, tire rotations, and brake replacements. Budgeting approximately $100–$150 per month for a “sinking fund” to cover these items can prevent financial shocks.

- Insurance Premiums: Insurance is a non-negotiable expense. For younger drivers or those in high-traffic urban areas, insurance can represent 20–30% of the total monthly cost of the vehicle. Before signing a purchase agreement, it is prudent to get an insurance quote to ensure the premium fits within your debt-to-income ratio.

3. Financing Strategies: Interest Rates and Loan Structures

In the current economic climate, the cost of borrowing capital is a major component of the car’s total price. A $35,000 car can easily become a $45,000 car once interest is factored in over a five-year term.

Leasing vs. Buying: Which Financial Path Fits Your Lifestyle?

Leasing is often marketed as a way to “get more car for less money,” but it is essentially a long-term rental where you pay for the vehicle’s depreciation during the most expensive years of its life.

- Leasing: Ideal for business owners who can utilize tax deductions or individuals who prioritize driving a new vehicle every three years and have a predictable, low-mileage lifestyle.

- Buying: Generally the superior wealth-building choice. Once the loan is paid off, the “monthly payment” disappears, allowing that capital to be redirected into investments or savings. The most cost-effective way to own a car is to buy a reliable model and drive it for ten years or more.

The Impact of Loan Terms and Credit Scores

The duration of the loan (the term) has a massive impact on the total interest paid. We are currently seeing a rise in 72-month and even 84-month auto loans. While these long terms lower the monthly payment, they often lead to “negative equity”—a situation where you owe more on the car than it is worth.

From a financial health perspective, any loan longer than 60 months should be approached with extreme caution. Furthermore, a credit score difference of 100 points can result in an interest rate spread of 5% or more, potentially saving or costing the buyer thousands of dollars over the life of the loan.

4. Smart Financial Planning for Your Next Vehicle

To ensure a car purchase doesn’t derail your broader financial goals, such as retirement or home ownership, you need a disciplined framework for budgeting.

The 20/4/10 Rule for Car Budgeting

Personal finance experts often suggest the “20/4/10” rule as a benchmark for affordability:

- 20% Down Payment: Putting at least 20% down ensures you have immediate equity in the vehicle and protects you from the initial depreciation hit.

- 4-Year Loan Term: Limiting the loan to 48 months keeps interest costs down and ensures the car is paid off while it still has significant value.

- 10% of Income: Your total transportation costs (loan payment, insurance, fuel, and maintenance) should not exceed 10% of your gross monthly income.

Exceeding these parameters often leads to “lifestyle creep,” where a disproportionate amount of your income is tied up in a depreciating machine rather than working for you in the market.

Calculating Opportunity Cost

The final consideration is the opportunity cost. If you choose a $600-a-month car payment over a $300-a-month payment, that extra $300, if invested in a diversified index fund over five years, could grow significantly. Over a 30-year period, the difference between driving a modest car and a luxury car every five years can equate to hundreds of thousands of dollars in lost retirement savings.

When asking “how much is for a car,” the answer isn’t just the number on the check you write today. It is the sum of the purchase price, the interest on the debt, the cost of maintenance, and the lost potential of that money had it been invested elsewhere. By applying these financial principles, you can transform a car from a potential liability into a manageable tool that supports your lifestyle without compromising your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.