In the rapidly evolving landscape of global finance, few digital assets have sparked as much debate, institutional interest, and strategic speculation as XRP. Often misunderstood by the general public as “just another cryptocurrency,” XRP was designed with a specific, high-stakes financial purpose: to revolutionize the way value moves across borders. While Bitcoin was envisioned as “digital gold” or a decentralized peer-to-peer cash system, XRP was built to serve as a bridge currency for the world’s banking infrastructure.

To understand how XRP works from a financial and investment perspective, one must look beyond the code and examine its role as a tool for liquidity. It is a digital asset designed to solve a multi-trillion-dollar problem in the global banking system—the inefficiency of cross-border settlements.

The Role of XRP in the Modern Financial Ecosystem

At its core, XRP is the native digital asset of the XRP Ledger (XRPL), an open-source, permissionless, and decentralized blockchain technology. However, its primary “Money” application lies in its utility for financial institutions. In the current global financial system, sending money from one country to another is surprisingly slow and expensive.

Bridging the Gap Between Traditional Banking and Blockchain

Most international transfers today rely on the SWIFT network, a system established in the 1970s. While SWIFT is reliable, it is essentially a messaging system, not a settlement system. When a bank in the United States wants to send funds to a bank in Southeast Asia, the actual movement of money involves a complex web of intermediary banks. This process can take three to five days and incurs significant fees at every step.

XRP works as a “bridge asset.” Because it can be settled in three to five seconds, it allows financial institutions to exchange value directly without needing a central intermediary or a series of correspondent banks. In this context, XRP acts as a universal translator for value, capable of sitting between two different fiat currencies (such as the USD and the Philippine Peso) and facilitating an instantaneous swap.

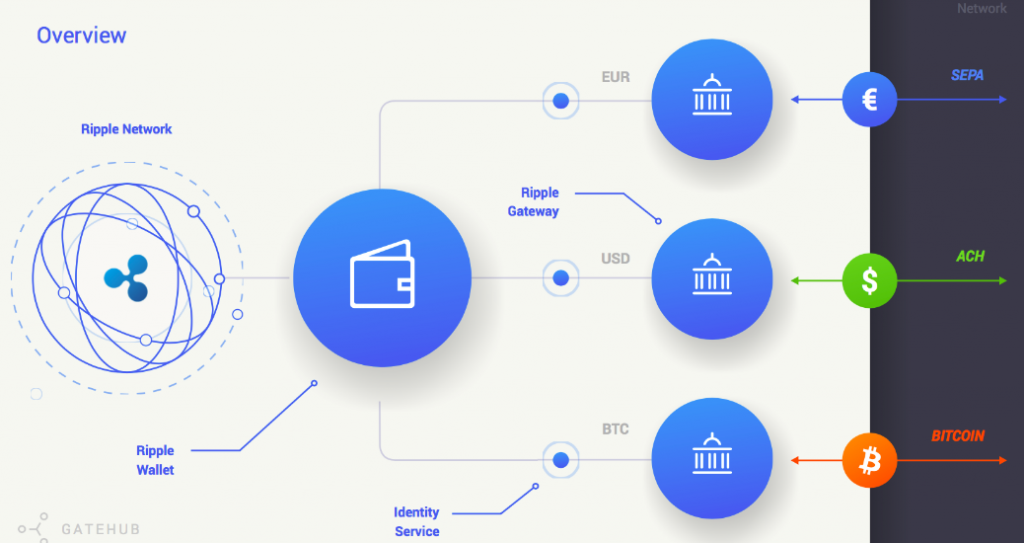

The Liquidity Problem and Nostro/Vostro Accounts

One of the most significant “hidden” costs in global finance is the requirement for “pre-funding.” To ensure smooth international transactions, large banks must maintain pre-funded accounts (known as Nostro/Vostro accounts) in various currencies around the world. Trillions of dollars of capital sit dormant in these accounts just to facilitate potential trades.

XRP offers a solution to this liquidity trap. By using XRP, banks do not need to keep pre-funded accounts in every destination currency. Instead, they can hold their native currency and buy XRP only at the moment of the transaction, which is then instantly converted into the destination currency. This “On-Demand Liquidity” (ODL) frees up vast amounts of capital, allowing banks to put that money to work in other areas, such as lending or investment.

The XRP Ledger (XRPL) as a Financial Settlement Tool

While the financial utility of XRP is clear, the mechanism that allows it to function as money is the XRP Ledger. Unlike Bitcoin, which uses a “Proof of Work” mining system that requires massive energy consumption and leads to slower transaction times, the XRPL uses a unique consensus protocol.

Consensus Over Mining: Speed and Efficiency

The XRP Ledger does not rely on miners to validate transactions. Instead, it uses a consensus mechanism where designated servers (validators) agree on which transactions are valid every few seconds. From an investment standpoint, this efficiency is a competitive advantage. The ability to process 1,500 transactions per second—compared to Bitcoin’s five or Ethereum’s fifteen—makes XRP a viable candidate for high-volume institutional use.

For a financial tool to be successful, it must be scalable and cost-effective. The XRPL’s consensus model ensures that transactions are not only fast but also incredibly cheap, usually costing less than a penny. This low friction is essential for “micropayments” and high-frequency settlement, areas where traditional banking systems and slower blockchains struggle to compete.

Transaction Costs and the Deflationary Burning Mechanism

A unique aspect of XRP’s monetary policy is its “burn” mechanism. Every transaction on the XRP Ledger requires a small amount of XRP to be paid as a fee. However, unlike traditional bank fees or even mining rewards in other blockchains, this fee is not paid to any party. Instead, the XRP used for the fee is permanently destroyed, or “burned.”

From a supply-and-demand perspective, this makes XRP a deflationary asset. While the total supply is capped at 100 billion tokens, the actual circulating supply slowly decreases over time as more transactions occur on the network. While the burn rate is currently very low, the architectural choice highlights a commitment to preventing spam on the network while theoretically adding long-term value for holders as the asset becomes scarcer.

Investing in XRP: Risks, Rewards, and Market Dynamics

For the individual investor or the corporate treasurer, XRP represents a unique asset class. It sits at the intersection of “FinTech” and “DeFi” (Decentralized Finance), but its price movements are often driven by factors different from those affecting retail-focused coins.

XRP vs. Bitcoin: Different Roles in a Portfolio

Investors often compare XRP to Bitcoin, but their roles in a financial portfolio are distinct. Bitcoin is frequently viewed as a “Store of Value”—a hedge against inflation and currency debasement. XRP, conversely, is a “Utility Token.” Its value is intrinsically linked to its adoption as a settlement tool.

If the global volume of cross-border payments moving through the XRPL increases, the demand for XRP as a liquidity bridge naturally rises. Therefore, an investment in XRP is essentially a bet on the modernization of the global financial infrastructure. It is a play on the “Internet of Value,” where money moves as easily and instantly as information moves today.

Regulatory Clarity and Institutional Adoption

One cannot discuss the financial landscape of XRP without mentioning the regulatory environment. For several years, XRP was at the center of a landmark legal battle between Ripple (the company most closely associated with its development) and the U.S. Securities and Exchange Commission (SEC). The core of the debate was whether XRP should be classified as a security (like a stock) or a commodity/currency.

In 2023, a pivotal court ruling provided significant clarity, stating that XRP itself is not necessarily a security when sold on public exchanges. For the “Money” niche, this clarity is paramount. Institutional investors—pension funds, hedge funds, and banks—are generally risk-averse and require clear legal frameworks before they can allocate capital to digital assets. The resolution of these regulatory hurdles positions XRP as one of the few digital assets with a recognized legal status in the United States, potentially opening the floodgates for institutional liquidity.

The Ripple Connection: How Corporate Use Cases Drive Value

It is vital to distinguish between XRP, the digital asset, and Ripple, the private American technology company. While Ripple did not “create” XRP (the ledger was developed by independent developers), Ripple is the most significant stakeholder and user of the asset.

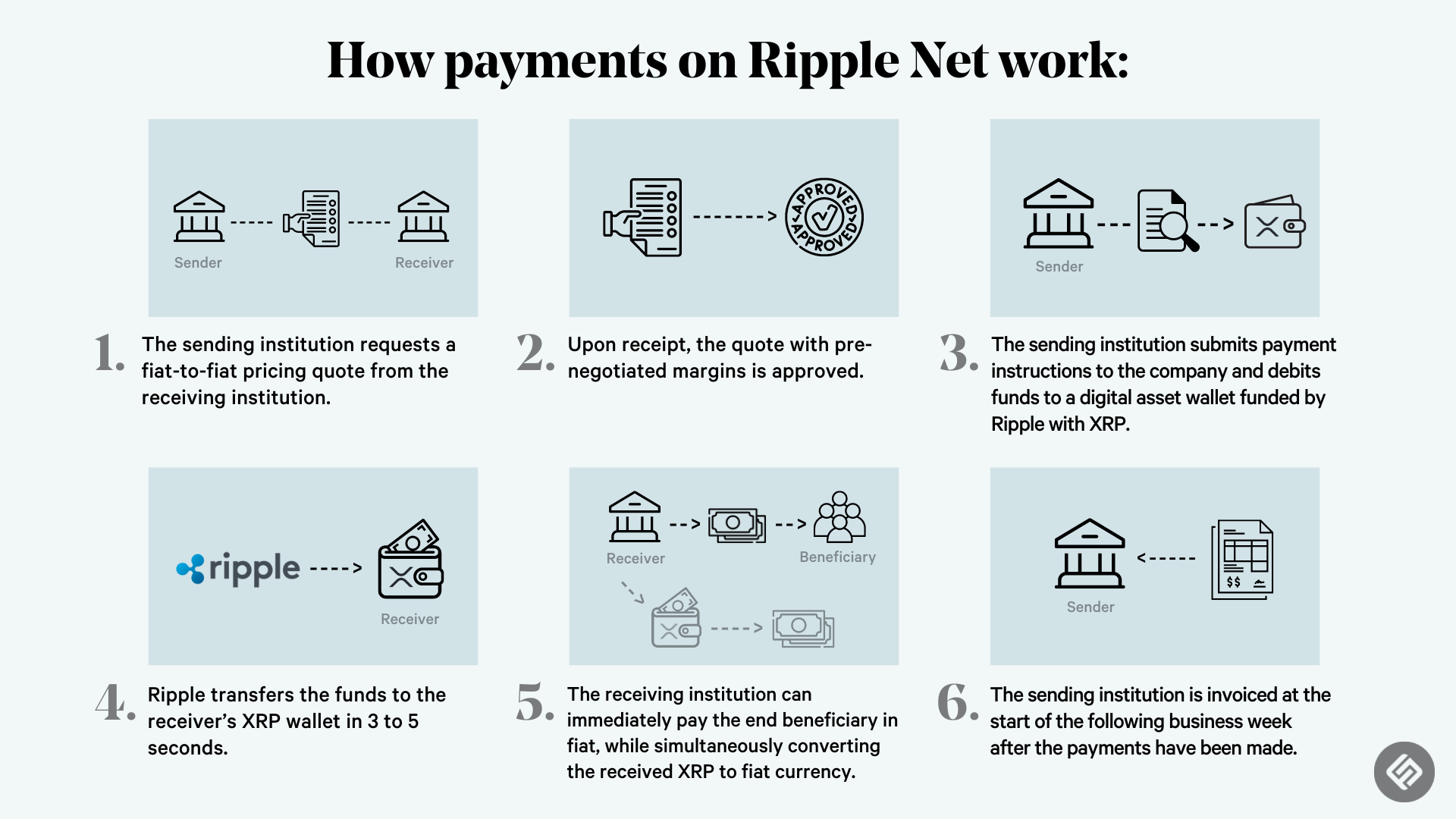

On-Demand Liquidity (ODL) and the Transformation of Remittances

Ripple’s flagship financial product, RippleNet, utilizes XRP via On-Demand Liquidity (ODL). This service is particularly transformative for the remittance market—the money sent home by migrant workers. In corridors like the U.S. to Mexico or the UAE to India, ODL allows remittance providers to settle transactions instantly.

By removing the need for intermediaries, these providers can lower their costs and pass those savings on to the consumer. For the investor, this creates a “real-world” use case that generates constant, non-speculative demand for the asset. Unlike many digital assets that rely on “hype” to maintain price, XRP’s value proposition is tied to the actual volume of money flowing through these corridors.

Strategic Partnerships with Central Banks and Financial Institutions

Beyond private remittances, the technology behind XRP is being explored for Central Bank Digital Currencies (CBDCs). Many nations are looking for “interoperability”—the ability for their future digital currencies to talk to one another. Because the XRP Ledger is neutral and decentralized, it is being tested as a potential “bridge” for CBDCs.

When a central bank considers using a ledger, they look for stability, speed, and cost. The track record of the XRPL, which has operated without downtime for over a decade, makes it a premier candidate for national-level financial projects. Any such adoption would fundamentally change the market cap and liquidity profile of XRP, moving it from a speculative asset to a core component of the global monetary system.

Conclusion: The Long-Term Outlook for XRP

Understanding “how XRP works” requires looking at it through the lens of capital efficiency. It is a financial instrument designed to move value across the globe in seconds, for a fraction of a cent, without the need for trillions of dollars in stagnant pre-funded accounts.

For those in the world of personal finance and investing, XRP represents a shift from the “speculative era” of crypto to the “utility era.” Its success is not dependent on being a digital currency for buying coffee, but rather on being the “plumbing” of the global financial system. As the world moves toward a 24/7, instantaneous economy, the demand for rapid liquidity will only grow. If XRP continues to secure its position as the preferred bridge for banks and central entities, its role in the future of money will be not just influential, but foundational.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.