In the landscape of American personal finance, few institutions command as much respect and brand loyalty as USAA (United Services Automobile Association). Founded in 1922 by a group of Army officers who were unable to secure auto insurance due to the perceived high-risk nature of their profession, USAA has evolved from a niche insurance provider into a full-service financial powerhouse. For many, a USAA membership is considered a “gold standard” in financial management, offering competitive rates, exceptional customer service, and specialized tools tailored to the unique lifestyles of military families. However, despite its popularity, there remains significant confusion regarding who can actually walk through its digital doors.

Understanding USAA eligibility is not just about identifying who can buy a policy; it is about recognizing a specific ecosystem of financial tools designed to optimize wealth for those who serve. Because USAA is a member-owned association rather than a publicly traded corporation, its eligibility requirements are strict, ensuring that the benefits remain concentrated within the community it was built to serve.

Understanding the Core Eligibility Requirements: The Military Connection

The foundation of USAA eligibility is built upon a direct connection to the United States Armed Forces. Because the organization operates under a reciprocal inter-insurance exchange model, the “risk pool” is intentionally limited to individuals who share the discipline and demographic profile of the military community.

Active Duty and Retired Military Personnel

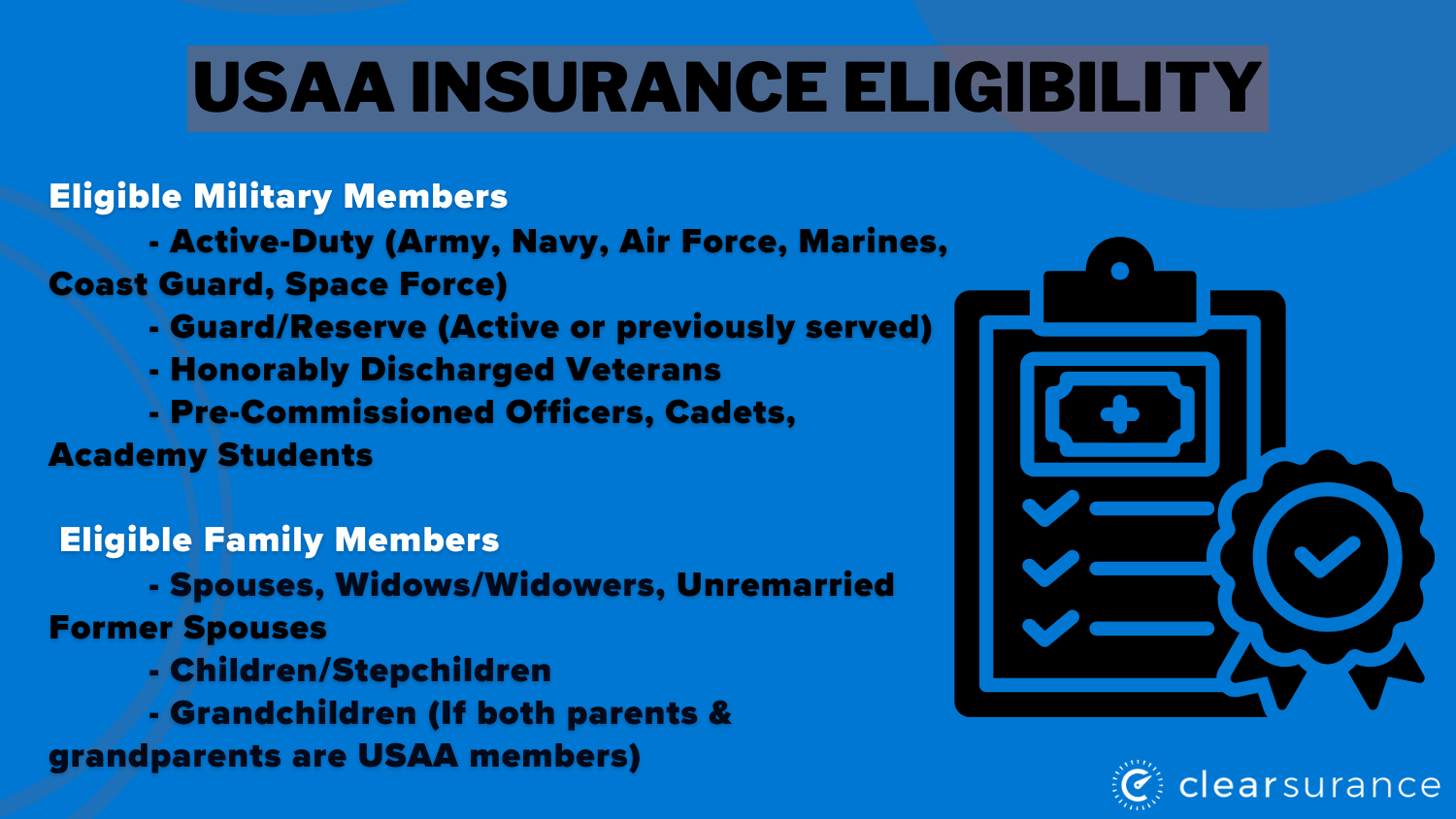

The most straightforward path to membership is through current or former service. This includes individuals currently serving in the U.S. Air Force, Army, Coast Guard, Marine Corps, Navy, and the newly established Space Force. Whether you are an enlisted member or a commissioned officer, active duty status grants full access to the suite of USAA products. Furthermore, those who have completed their service and retired with full benefits are eligible to maintain their membership for life.

Veterans and the Importance of Discharge Status

A common misconception is that you must have retired from the military (served 20+ years) to qualify for USAA. In reality, any veteran who has served honorably is eligible. This includes those who served in the National Guard and Reserves. The critical factor here is the characterization of service; an “Honorable” or “General Under Honorable Conditions” discharge is typically required. Those with “Other Than Honorable” or “Dishonorable” discharges are generally excluded from membership, as the organization seeks to maintain a specific risk profile within its membership base.

Cadets, Midshipmen, and Commissioning Programs

USAA recognizes that financial literacy and stability should begin at the start of a military career. Therefore, eligibility is extended to students at U.S. service academies (such as West Point or Annapolis), as well as those in the Reserve Officers’ Training Corps (ROTC) who are under contract. Additionally, candidates in Officer Candidate School (OCS) or Officer Training School (OTS) can establish their membership before they even receive their first set of bars.

The Multi-Generational Legacy: Family Member Eligibility

One of the most powerful aspects of USAA is its “hereditary” nature. Unlike many other financial institutions where benefits end with the account holder, USAA allows its members to pass down the privilege of eligibility to their descendants. This creates a multi-generational financial strategy that can benefit families for decades.

Spouses and Former Spouses

Widows, widowers, and un-remarried former spouses of USAA members who joined USAA prior to or during the marriage are generally eligible for membership. This provides a vital financial safety net for military families, ensuring that the surviving or divorced spouse retains access to high-quality insurance and banking services. It is important to note that if a former spouse remarries a non-eligible person, their ability to open new lines of insurance may be impacted, though existing accounts often remain active.

Children and Stepchildren: Passing Down the Benefit

The “chain of eligibility” is perhaps the most sought-after feature of USAA. If a parent is a USAA member and has established an insurance product (such as auto or property insurance), their children and stepchildren become eligible to join. Once a child establishes their own membership, they can then pass that eligibility down to their own children. This creates a perpetual cycle of financial access. However, the key caveat is that the parent must have joined and held a qualifying insurance policy for the eligibility to transfer. A parent who only uses USAA’s free banking tools may not be able to pass on full insurance eligibility to their children.

Limitations and Scenarios for Non-Military Relatives

It is a frequent point of frustration for many that siblings, cousins, and parents of military members do not automatically qualify for USAA based on that relationship. For example, if you are a veteran, your children can join, but your brother or your father cannot (unless they themselves served). This strict adherence to the direct line of descent and marriage is what allows USAA to manage its capital so effectively, focusing its “subscriber’s accounts” on a controlled demographic.

Why USAA Membership Matters for Your Personal Finance Strategy

While the question of “who can join” is technical, the question of “why join” is purely financial. In the realm of money management, USAA offers several distinct advantages that are difficult to replicate in the traditional retail banking or insurance markets.

Competitive Insurance Rates and Coverage

For the average consumer, insurance is a grudge purchase. For the USAA member, it is an asset. USAA consistently ranks at the top of J.D. Power surveys for customer satisfaction and claims processing. Because the organization understands the specific risks associated with military life—such as frequent moves (PCSing), deployments, and vehicle storage—their policies are written with unique protections that standard insurers might charge extra for or exclude entirely.

Banking and Lending Advantages

From a cash-flow perspective, USAA Federal Savings Bank offers several perks that optimize personal liquidity. This includes early direct deposit (receiving a military paycheck up to two days early) and a vast network of ATM fee reimbursements. In terms of lending, USAA’s competitive rates on auto loans and personal lines of credit are often lower than national averages, providing members with cheaper access to capital for major life purchases.

Investment and Retirement Planning Tools

Beyond daily banking, USAA provides a robust platform for long-term wealth building. While they have partnered with firms like Victory Capital and Charles Schwab for certain investment products, the integrated experience allows members to view their entire financial life—from their homeowners’ insurance to their Roth IRA—in a single dashboard. This “holistic” view is essential for effective asset allocation and retirement planning.

Maximizing Your Membership: Beyond Just Insurance

For those who do qualify, membership should be viewed as a comprehensive financial ecosystem rather than just a place to get a car insurance quote. To truly benefit from the “Money” aspect of USAA, members must engage with the organization’s deeper financial structures.

The Subscriber’s Savings Account

One of the most unique financial features of USAA is the Subscriber’s Savings Account (SSA). Because USAA is a reciprocal exchange, a portion of the organization’s capital is held in accounts designated for individual members. In years where USAA performs well financially (usually when claims are lower than projected), a portion of the profit may be allocated to these SSAs. Over decades, these accounts can grow into thousands of dollars, which are eventually paid out to the member upon retirement from the association or after a certain period of membership. This is essentially a form of “passive wealth” that no traditional insurance company offers.

Integration with Military Benefits

USAA excels at bridging the gap between civilian financial tools and Department of Defense (DoD) benefits. Their advisors are specifically trained to understand the Thrift Savings Plan (TSP), the Survivor Benefit Plan (SBP), and the nuances of VA Loans. For a member, this means receiving financial advice that factors in their military pension and healthcare (TRICARE), leading to a more accurate and efficient financial plan.

Financial Advice and Wealth Management

Managing money as a military professional involves unique challenges, such as combat pay tax exclusions and the tax implications of living in different states. USAA provides educational resources and professional advisory services that cater to these specific scenarios. By utilizing these tools, members can ensure they are not overpaying in taxes and are maximizing their ability to save for the future.

Conclusion: A Restricted Community with Boundless Value

The question of “who can get USAA insurance” is ultimately a question of heritage and service. While the restrictions may seem exclusionary, they are the very reason the institution remains a powerhouse in the financial sector. By limiting its membership to those who have served and their immediate families, USAA creates a stable, loyal, and lower-risk community that allows for higher dividends, lower rates, and superior service.

If you fall within the eligibility window—as a service member, a veteran, or the child/spouse of a member—failing to utilize USAA is often a missed opportunity in your personal finance journey. It represents more than just a brand; it represents a specialized toolset designed to help military families navigate the complexities of wealth management, risk mitigation, and long-term financial security. In the world of money, access is often the greatest asset of all, and for those who qualify, USAA is an asset that yields returns for a lifetime.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.