For the modern consumer, the question “How much does a new Tesla cost?” is rarely answered by a single sticker price. In the realm of personal finance and strategic investing, a Tesla represents more than just a vehicle; it is a complex financial asset with a fluctuating entry price, significant tax implications, and a unique total cost of ownership (TCO) profile. As Tesla continues to utilize a dynamic pricing model—shifting MSRPs more frequently than any other major automaker—potential buyers must approach the purchase through the lens of financial planning.

Understanding the financial footprint of a Tesla requires looking beyond the “Order Now” button on the website. To truly grasp the cost, one must account for federal incentives, state-level rebates, charging infrastructure investments, insurance premiums, and the projected resale value in an increasingly volatile used EV market.

1. Analyzing the Current Price Matrix: From Entry-Level to High-End Assets

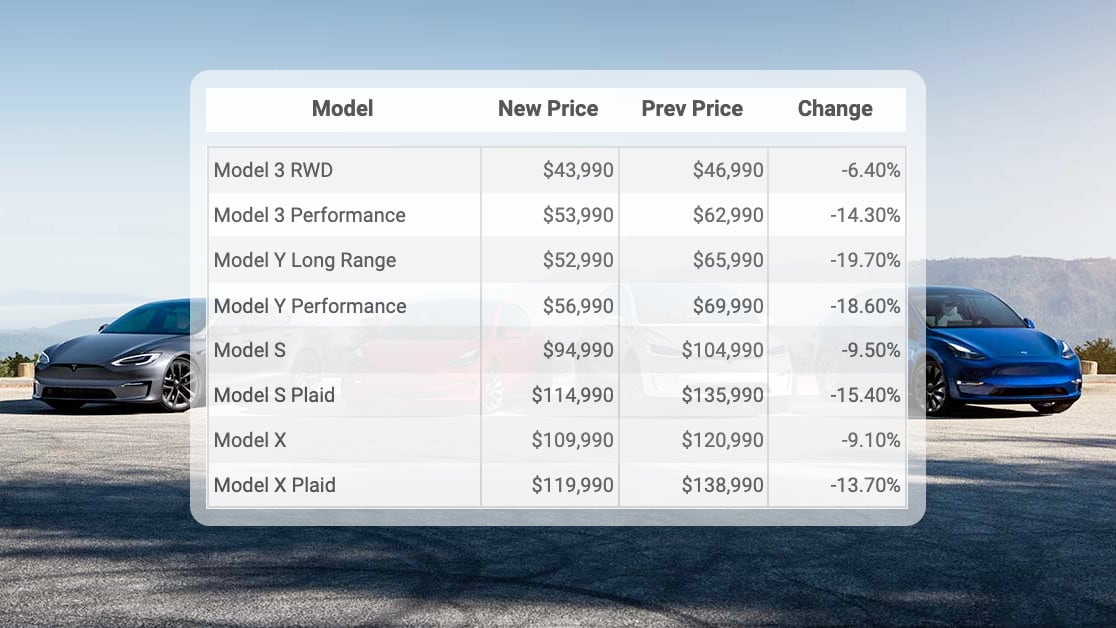

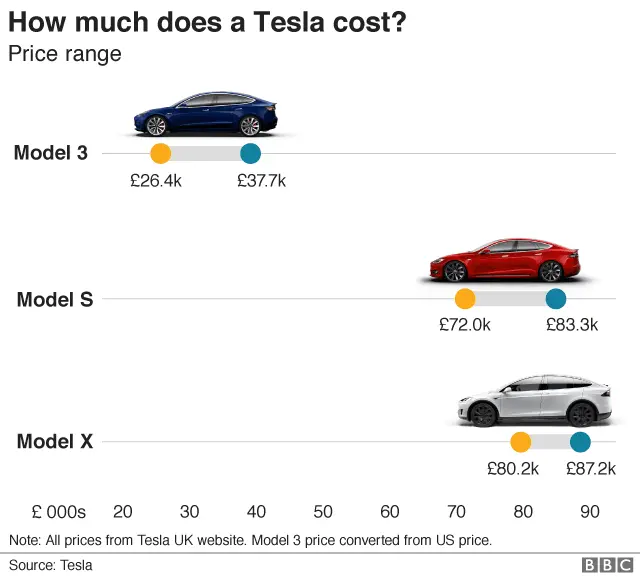

The entry point into the Tesla ecosystem is defined by four primary models, each serving a different segment of the market and requiring a different level of capital allocation. Because Tesla does not use a traditional dealership model, the price you see online is the price you pay, but these figures are subject to change based on market demand and production efficiencies.

The Model 3 and Model Y: High-Volume Financial Entry Points

The Model 3 serves as the “gateway” asset. Currently, the Rear-Wheel Drive (RWD) variant represents the lowest capital requirement for a new Tesla, often hovering in the high $30,000 to low $40,000 range. For many, this is the most logical “Side Hustle” or commuter vehicle due to its high efficiency-to-cost ratio.

The Model Y, which has recently held the title of the world’s best-selling vehicle, commands a premium over the Model 3, usually starting in the mid-to-high $40,000s. From a financial perspective, the Model Y often retains its value better than the Model 3 due to the high market demand for crossovers, making it a potentially safer place to park capital for those concerned about depreciation.

The Model S and Model X: Luxury Capital Outlay

For high-net-worth individuals or those utilizing the vehicle for business purposes under specific tax codes (such as Section 179 for heavier vehicles), the Model S and Model X represent a significant jump in investment. These models start in the $75,000 to $80,000 range and can quickly exceed $100,000 for “Plaid” performance variants. These vehicles are less about “saving money on gas” and more about luxury asset acquisition, often involving complex financing or leasing structures.

The Cybertruck and the Future of Niche Asset Value

The Cybertruck introduces a new variable into the Tesla financial equation. With its “Foundation Series” pricing reaching into the six figures, it currently acts as a high-cost, high-visibility asset. For business owners, the Cybertruck’s gross vehicle weight rating (GVWR) offers unique tax advantages that smaller EVs do not, potentially allowing for accelerated depreciation strategies.

2. Navigating the Federal and State Incentive Landscape

When calculating the cost of a Tesla, the MSRP is only the “gross” price. The “net” price is often significantly lower thanks to the Inflation Reduction Act (IRA) and various local government subsidies. Mastering these incentives is a crucial part of personal finance for any prospective EV owner.

The $7,500 Federal Tax Credit (Point of Sale)

Under current regulations, many Tesla models qualify for a $7,500 federal tax credit. The financial brilliance of the updated 2024 regulations is that this credit can now be applied as a “point-of-sale” discount. This effectively lowers your loan principal or cash outlay immediately, rather than forcing you to wait until tax season to see the benefit. However, this is subject to income caps ($150,000 for individuals, $300,000 for joint filers) and MSRP limits ($55,000 for sedans and $80,000 for SUVs).

State Rebates and Local Incentives

Beyond federal help, states like California, Colorado, and New York offer additional rebates that can range from $500 to $5,000. Some utility companies also offer financial incentives for installing home charging stations. When these are stacked, the “cost” of a $45,000 Model Y can drop into the mid-$30,000s, making the financial argument for the vehicle much more compelling compared to internal combustion engine (ICE) competitors.

Business Tax Credits and Section 179

For entrepreneurs and business owners, the financial math changes entirely. If a Tesla is used for more than 50% business use, it may qualify for various depreciation schedules. Heavier models like the Model X or Cybertruck may allow for significant first-year write-offs under Section 179, potentially saving the business owner tens of thousands of dollars in taxable income.

3. Total Cost of Ownership: Fuel Savings vs. Operational Expenses

A fundamental rule of business finance is to distinguish between “upfront cost” and “operating cost.” A Tesla typically carries a higher upfront cost than a comparable gas car but offers a significantly lower operational expense profile.

The “Gas Savings” Fallacy and Reality

Tesla’s website often lists a “price after probable savings.” While this can be misleading, the underlying math is sound. On average, charging a Tesla at home costs about 1/3rd to 1/4th the price of fueling a gasoline vehicle per mile. For a driver covering 15,000 miles a year, this can result in $1,000 to $2,000 in annual cash flow improvements. However, if a driver relies solely on the Tesla Supercharger network, these savings diminish, as Supercharging rates are often double or triple home electricity rates.

Maintenance and the Elimination of the “Mechanical Liability”

One of the strongest financial arguments for a Tesla is the reduction in maintenance liabilities. With no oil changes, spark plugs, timing belts, or smog checks, the long-term maintenance schedule is stripped down to tires, cabin air filters, and brake fluid checks. Over a five-year period, this can save the owner several thousand dollars in “sunk costs” that would have been required to keep a gas vehicle operational.

The Insurance Premium Variable

While you save on gas and oil, you may pay more in insurance. Tesla vehicles are often more expensive to insure due to high repair costs and the specialized nature of their aluminum bodies and sensor suites. From a personal finance perspective, it is essential to get an insurance quote before purchasing, as a $50/month increase in insurance premiums can eat into a significant portion of your “gas savings.”

4. Financing, Depreciation, and Resale Value Strategy

The final pillar of the Tesla cost equation is the exit strategy. How much will the vehicle be worth in three to five years? This is where the financial complexity of Tesla ownership is most apparent.

The Impact of Dynamic Pricing on Resale

In early 2023, Tesla aggressively cut prices on new models. While this was great for new buyers, it caused an immediate drop in the resale value of existing Teslas. Investors in the brand must realize that Tesla operates more like a tech company than a traditional car manufacturer; they will lower prices to move volume, which can hurt your “equity” in the car. Unlike a Porsche or a Toyota, which have predictable depreciation curves, a Tesla’s value is tethered to the current price of a new one.

Financing vs. Leasing: Which Makes More Financial Sense?

Because the EV market is evolving so rapidly—with battery tech improving every year—leasing has become an attractive financial tool for those who want to avoid “obsolescence risk.” Leasing allows you to walk away after three years, shielding you from any unexpected drops in resale value. However, for those looking to build equity and keep the vehicle for 10+ years, financing at a competitive rate (often through credit unions, which offer “green vehicle” discounts) remains the superior wealth-building move.

Full Self-Driving (FSD) as a Sunk Cost

Tesla offers “Full Self-Driving” as a software add-on, often costing between $8,000 and $12,000 (or a monthly subscription). From a strict financial standpoint, FSD is currently a poor investment. Historical data shows that the used market does not value FSD at its full MSRP. If you are looking to minimize your total investment, the subscription model is often the more fiscally responsible choice, as it prevents you from “over-capitalizing” an asset that might not return that value upon resale.

Final Economic Summary: Is a Tesla a Sound Financial Decision?

To answer “how much does a new Tesla cost,” one must conclude that the price is a moving target influenced by tax brackets, local utility rates, and market timing. For a buyer who qualifies for the $7,500 tax credit, has low home electricity rates, and drives more than 12,000 miles a year, a Tesla is often a superior financial instrument compared to a gas-powered vehicle. It represents a shift from high variable costs (gas and maintenance) to a higher fixed cost (loan payment) that eventually nets a positive return in the form of lower monthly outlays.

However, for those who cannot charge at home or do not qualify for incentives, the “true cost” can remain high. In the modern economy, buying a Tesla is not just a lifestyle choice—it is a sophisticated exercise in cash flow management and tax optimization. By calculating the net entry price, leveraging all available subsidies, and accounting for the insurance-to-fuel-savings ratio, an informed buyer can ensure that their Tesla is not just a high-tech gadget, but a well-integrated component of their broader financial portfolio.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.