For most individuals, a vehicle represents the second-largest financial investment they will make, surpassed only by the purchase of a home. Yet, unlike real estate, which historically appreciates, an automobile is a complex, depreciating asset. Understanding the precise value of your car is not merely a matter of curiosity; it is a fundamental component of proactive personal finance. Whether you are looking to sell, trade-in, refinance a loan, or simply assess your net worth, having an accurate grasp of your vehicle’s market value allows you to make data-driven decisions rather than emotional ones.

In the modern financial landscape, “value” is a fluid concept influenced by algorithmic data, regional supply and demand, and macroeconomic trends. This guide explores the sophisticated methodologies used to determine automotive value and how you can leverage this information to optimize your financial portfolio.

The Financial Importance of Accurate Vehicle Valuation

Before diving into the “how,” one must understand the “why.” Treating your car as a line item on a balance sheet requires a shift in perspective from viewing it as a mere mode of transportation to viewing it as a liquidatable asset.

Impact on Personal Net Worth

Your net worth is a calculation of everything you own (assets) minus everything you owe (liabilities). For many households, the equity in a vehicle—the difference between the car’s current market value and the remaining loan balance—is a significant portion of their liquid or semi-liquid wealth. An overestimation of your car’s value can lead to a distorted view of your financial health, while an underestimation might mean you are leaving money on the table during a transition.

Strategic Advantage in Negotiations

Knowledge is the ultimate leverage in any financial transaction. When you enter a dealership or a private sale discussion armed with a certified valuation, you shift the power dynamic. Dealerships often rely on “information asymmetry,” where they know more about the market than the consumer. By performing a rigorous valuation, you bridge this gap, ensuring that you receive a fair price for your trade-in or justify your asking price to a private buyer.

Insurance and Risk Management

In the event of a total loss (accident or theft), insurance companies offer a settlement based on the “Actual Cash Value” (ACV) of the vehicle. If you do not know what your car is worth, you cannot determine if an insurance payout is sufficient to replace the asset. Furthermore, for those with high-value or classic cars, understanding the current market allows you to adjust your policy to “Stated Value” or “Agreed Value,” protecting you against the rapid fluctuations of the used car market.

Primary Valuation Methodologies and Financial Tools

There is no single “true” price for a vehicle; instead, there are different values based on the context of the transaction. To find the value of your car, you must utilize various financial tools and understand the nuances between their outputs.

Book Value vs. Market Value

“Book value” refers to the pricing provided by industry aggregates like Kelley Blue Book (KBB), J.D. Power (formerly NADA), and Edmunds. These platforms use massive datasets of historical sales and auction results to provide a statistical average. “Market value,” however, is the real-time price a buyer is willing to pay today. During periods of high inflation or supply chain disruptions, market value can significantly decouple from book value. A savvy owner looks at both: the book value as a baseline and local listings (such as Autotrader or Cars.com) to see the real-time “street” price.

Utilizing Digital Appraisal Platforms

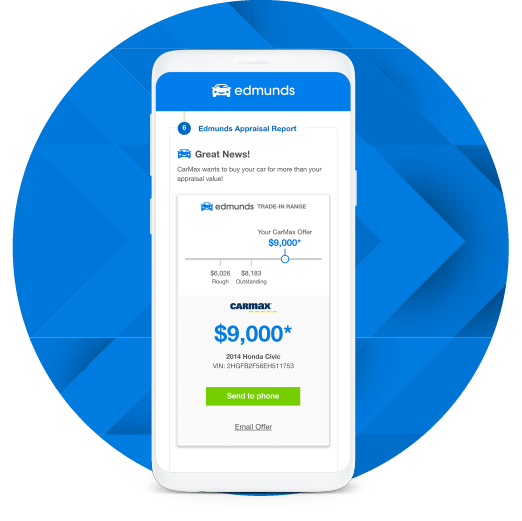

The rise of “fintech” in the automotive space has introduced instant-offer platforms like Carvana, Vroom, and CarMax. These companies use proprietary algorithms to provide a “buy-it-now” price. While these offers might be slightly lower than what you could get in a private sale, they represent the most accurate “liquidity value” of your car—the amount of cash you could theoretically have in your bank account within 48 hours. Using these tools in conjunction with traditional blue-books provides a high-low range for your asset’s value.

Private Party vs. Trade-In Value

It is vital to distinguish between these two figures. The Trade-In Value is essentially the wholesale price. The dealer must account for reconditioning costs, overhead, and a profit margin when they resell the car. Consequently, this value is usually the lowest. The Private Party Value is higher because you are selling directly to the end-user, capturing the margin the dealer would otherwise take. Finally, the Retail Value is what a dealer would ask for the car on their lot. When valuing your car, you must decide which exit strategy you intend to use, as the delta between trade-in and private party can be thousands of dollars.

Economic Variables Influencing Depreciation and Resale

The value of a vehicle is not static; it is subject to a variety of economic pressures and physical metrics. To find an accurate value, you must apply these variables to the baseline numbers provided by valuation tools.

Mileage and Condition Metrics

The most immediate factors are mileage and physical condition. In the financial world of automobiles, there are “milestone” markers—30,000, 60,000, and 100,000 miles—where value tends to drop more sharply due to the expiration of warranties or the requirement of major maintenance. Furthermore, the “condition” grade (Excellent, Good, Fair, Poor) is often subjective. Most owners overrate their vehicle’s condition. A professional perspective requires an honest assessment of mechanical integrity, tire tread depth, and cosmetic imperfections, each of which carries a specific “deduction” in the eyes of a professional appraiser.

Regional Market Fluctuations

Geography plays a massive role in valuation. A rear-wheel-drive convertible has a higher market value in Miami or Los Angeles than it does in Anchorage during November. Conversely, a four-wheel-drive SUV commands a premium in mountainous or snowy regions. When using valuation tools, always ensure you are inputting your specific zip code to account for these regional supply-and-demand imbalances.

Brand Equity and Historical Reliability

Not all brands depreciate at the same rate. Vehicles from manufacturers with high “perceived reliability” (such as Toyota or Honda) often retain a higher percentage of their original MSRP than luxury vehicles with high maintenance costs. From a financial planning perspective, understanding the “Depreciation Curve” of your specific brand allows you to time your exit. Some vehicles lose 20% of their value in the first year, while others might take three years to hit that same mark.

Maximizing Your Return: Financial Strategies for Sellers

Once you have identified the value of your car, the goal shifts to “value preservation” or “value enhancement.” How can you ensure you actually capture the highest possible amount during the transaction?

Strategic Reconditioning

Before selling, consider the “Return on Investment” (ROI) of repairs. Spending $500 on a professional detail and minor dent repair can often add $1,000 to $1,500 to the perceived value of the car. However, major mechanical repairs often do not offer a 1-to-1 return. If your car needs a $3,000 transmission, it may be more financially sound to sell it “as-is” at a discounted price rather than trying to recoup that specific expense in the sale price.

Timing the Market

Automotive markets have seasonal cycles. For instance, the “Tax Season Effect” in the United States often leads to an increase in used car prices in the spring, as consumers use tax refunds for down payments. Similarly, selling an AWD vehicle just before the first snowfall can result in a quicker sale at a higher price point. Monitoring these cycles allows you to “sell high” and potentially “buy low” on your next vehicle.

Tax Implications of Sale or Trade-In

From a business finance perspective, the “Trade-In Tax Credit” is a critical consideration. In many jurisdictions, you only pay sales tax on the difference between your new car’s price and your trade-in’s value. For example, if you buy a $40,000 car and trade in a $20,000 car, you only pay sales tax on $20,000. If your state sales tax is 8%, that is a $1,600 savings. If a private buyer offers you $21,000 for the car, you are actually financially better off taking the $20,000 trade-in because of the tax shield. Always calculate the “effective value” of a trade-in including tax savings before dismissing it in favor of a private sale.

Conclusion: The Asset Management Mindset

Finding the value of your car is more than a simple Google search; it is an exercise in market analysis and financial literacy. By understanding the distinction between book and market values, acknowledging the impact of depreciation variables, and calculating the tax implications of your exit strategy, you treat your vehicle as a serious component of your financial life.

In an era of economic volatility, being an informed consumer is your best defense against inflation and market shifts. Whether you are holding onto your vehicle for another five years or preparing to list it tomorrow, a regular “audit” of your car’s value ensures that you are always in the driver’s seat of your personal finances. Accurate valuation leads to better budgeting, smarter investing, and ultimately, a more robust bottom line.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.