For investors, analysts, and business enthusiasts, the question “how many Home Depot stores are there?” is rarely about simple geography. Instead, it serves as a fundamental metric for assessing the health of the retail sector, the robustness of the housing market, and the strategic direction of one of the world’s most successful “big box” retailers. As of the most recent fiscal reports, The Home Depot operates approximately 2,335 stores across North America, including the United States, Canada, and Mexico.

However, the sheer number of storefronts is only one piece of a complex financial puzzle. To understand the “Money” aspect of Home Depot, one must look at how these 2,300+ locations translate into billions of dollars in shareholder value, consistent dividend growth, and a dominant market share in the home improvement industry.

The Financial Scale of the Home Depot Empire

To appreciate the magnitude of Home Depot’s physical presence, one must look at the revenue generated per square foot. While many retailers struggled during the transition to digital-first commerce, Home Depot leveraged its physical locations to become high-efficiency distribution hubs.

Store Count Evolution and Strategic Saturation

Unlike many retail chains that pursued aggressive, unchecked expansion in the early 2000s, Home Depot reached a point of “strategic saturation.” For the past decade, the company has focused less on opening hundreds of new locations and more on optimizing the profitability of its existing 2,335 stores. This shift from capital expenditure (CAPEX) on new construction to investment in technology and supply chain efficiency has drastically improved the company’s Return on Invested Capital (ROIC).

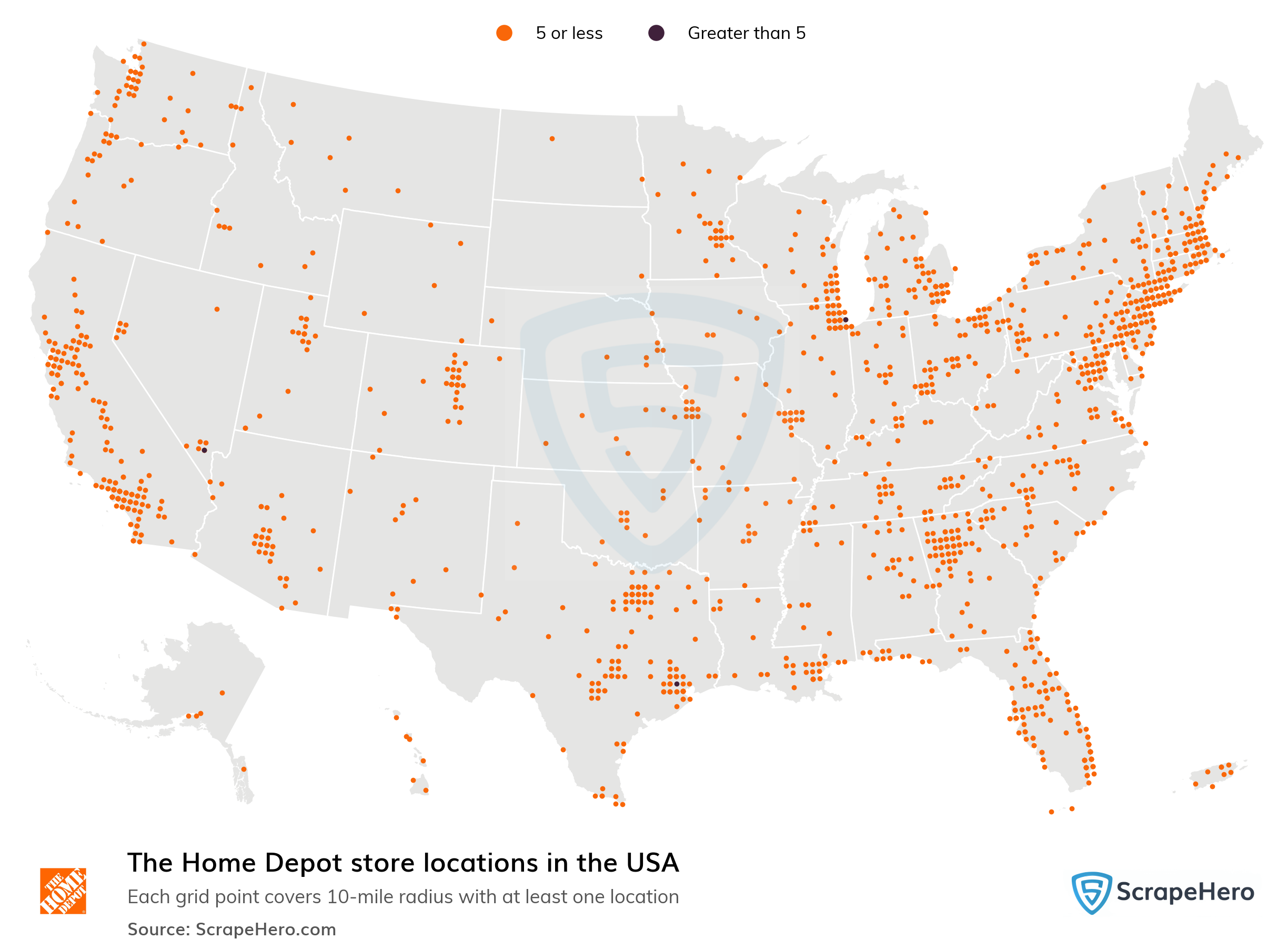

In the United States alone, the company operates approximately 2,000 stores, with the remainder spread across all ten Canadian provinces and 32 Mexican states. This geographic spread ensures that Home Depot remains within a 10-mile radius of the vast majority of the U.S. population, a key driver of its “Interconnected Retail” strategy.

Revenue per Store Metrics

When evaluating Home Depot as a business entity, the “per store” metrics are staggering. With annual sales often exceeding $150 billion, the average Home Depot location generates roughly $64 million in annual revenue. This high productivity is a result of the company’s ability to serve two distinct customer bases: the Do-It-Yourself (DIY) consumer and the “Pro” (professional contractor). By utilizing the physical store as both a showroom and a wholesale warehouse, Home Depot maximizes the utility of its real estate.

Real Estate Value and Geographic Dominance

From a business finance perspective, Home Depot’s store count represents a massive real estate portfolio. The company owns approximately 90% of its store locations, a rarity in modern retail where many companies prefer sale-leaseback agreements to keep debt off the balance sheet.

The Power of Owned Real Estate

By owning the majority of its locations, Home Depot insulates itself from rising commercial rent costs. This ownership structure provides a significant “moat” during inflationary periods. In a financial downturn, the value of the land and buildings acts as a massive asset on the balance sheet, providing the company with better credit ratings and lower borrowing costs compared to competitors who lease their space.

For investors, this means Home Depot isn’t just a retail company; it is effectively a massive real estate holding company. The 2,335 locations are strategically placed in high-traffic corridors and growing suburban areas, ensuring that the underlying land value continues to appreciate alongside the retail business.

North American Market Penetration and Expansion

While the U.S. market is largely saturated, Home Depot continues to find growth opportunities in Mexico and Canada. The Mexican market, in particular, offers a different financial dynamic. With a growing middle class and a fragmented local hardware market, Home Depot’s standardized “big box” model provides a competitive advantage that drives high margins. The capital allocated to international stores often yields a higher growth rate than domestic stores, contributing to the overall diversified income stream of the corporation.

Analyzing Stock Performance (HD) and Shareholder Returns

The store count is the engine, but the stock performance is the output. The Home Depot (ticker: HD) has long been a darling of Wall Street, known for its consistency, management quality, and aggressive capital return program.

Historical Returns and Market Resilience

If you look at the growth of HD stock over the last twenty years, it has significantly outperformed the S&P 500. This is largely due to the company’s “Total Value” philosophy. By maintaining a steady store count while increasing the efficiency of each location, Home Depot has been able to generate massive amounts of free cash flow.

During the 2008 housing crisis, the company proved its resilience by tightening operations without mass store closures. More recently, during the pandemic-era housing boom, the company saw a surge in “wallet share” as consumers redirected travel and leisure spending into home renovations. This agility is a primary reason why institutional investors view the 2,300+ stores as a safe harbor for capital.

Dividend Growth and Share Repurchases

For the income-focused investor, Home Depot’s store count translates into reliable dividends. The company has a long history of increasing its dividend payout, often at double-digit rates. This is supported by a disciplined share buyback program. Because the company is no longer spending billions of dollars annually on building new stores from scratch, it can redirect that cash back to shareholders. This financial strategy—transitioning from a “growth” stock to a “value/income” powerhouse—is a classic case study in corporate finance.

Future Outlook: Scaling Beyond the Physical Footprint

As we look toward the future, the relevance of “how many stores” is changing. The next phase of Home Depot’s financial growth isn’t about hitting 3,000 stores; it’s about the “Pro” ecosystem and e-commerce integration.

The High-Margin “Pro” Segment

Professional contractors represent about 10% of Home Depot’s customer base but account for nearly 50% of its sales. The company is currently investing billions into “Project One,” a strategy designed to capture more of the complex Pro market. This involves building specialized distribution centers that bypass the traditional retail store for large-scale job site deliveries. From a financial perspective, this allows Home Depot to grow its revenue without needing to increase its retail store count, thereby increasing profit margins and reducing overhead.

The Interconnected Retail Model (Omnichannel)

The modern Home Depot store is no longer just a place to buy a hammer; it is a fulfillment center. Approximately 50% of Home Depot’s online orders are picked up in a physical store. This “Click and Collect” model is a financial masterstroke. It reduces the “last mile” shipping costs—one of the biggest expenses in e-commerce—and drives additional foot traffic into the stores, leading to impulse purchases.

By integrating the 2,335 physical locations with a sophisticated digital platform, Home Depot has created a defensive barrier against digital-only competitors like Amazon. The physical store provides immediate gratification and expert advice that an algorithm cannot replicate, ensuring the long-term viability of the company’s capital investments.

Conclusion: The Financial Significance of 2,335

In conclusion, when we ask “how many Home Depot stores are there,” we are really asking about the scale of a financial titan. Those 2,335 stores represent over 200 million square feet of prime real estate, $150 billion in annual consumer spending, and a foundation for one of the most reliable dividend-paying stocks in the Dow Jones Industrial Average.

Home Depot’s strategy of “quality over quantity”—focusing on the productivity of existing stores rather than mindless expansion—has made it a blueprint for successful modern retail. For the investor or the business professional, these stores are more than just warehouses for lumber and appliances; they are high-output financial engines that continue to dominate the North American economic landscape. Whether through the lens of real estate value, stock performance, or market share, the footprint of Home Depot remains a vital indicator of financial health in the 21st century.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.