Social Security serves as the cornerstone of retirement planning for millions of Americans. Yet, for many, the actual math behind that monthly check remains a mystery. Unlike a standard savings account where you withdraw what you put in plus interest, Social Security is governed by a complex set of formulas designed to balance individual contributions with a social safety net. Understanding how these payments are calculated is not just an academic exercise; it is a vital component of personal finance that allows you to make informed decisions about when to retire and how much you need to save in private accounts.

The calculation is a multi-step process that looks at your entire working life, adjusts for inflation, and applies a progressive formula to determine your “Primary Insurance Amount” (PIA). This guide breaks down the technical mechanics of the Social Security Administration’s (SSA) methodology to help you take control of your financial future.

The Foundation: Your Average Indexed Monthly Earnings (AIME)

Before the SSA can determine your benefit, they must first determine your career-long average earnings. This isn’t as simple as adding up your paychecks; the government uses a specific metric called Average Indexed Monthly Earnings (AIME).

The 35-Year Rule

The Social Security calculation is based on your highest 35 years of earnings. If you worked for 40 years, the SSA will automatically pick the 35 years in which you earned the most (after indexing for inflation) and discard the lowest five. However, if you worked fewer than 35 years, the SSA does not shorten the denominator. Instead, they fill in the remaining years with zeros. These “zero years” can significantly drag down your career average, which is why financial planners often recommend working at least 35 years to maximize your benefit potential.

Inflation Indexing and Earnings Caps

To ensure that wages earned in 1985 are comparable to wages earned in 2024, the SSA “indexes” your past earnings. They use the Average Wage Index (AWI) to adjust your historical pay to reflect the general rise in standard of living. This ensures that your benefit reflects the economic reality of the year you turn 60.

It is also important to note the “Social Security Wage Base.” Each year, there is a cap on the amount of income subject to Social Security taxes ($168,600 in 2024). Any income earned above this threshold is not taxed for Social Security and, consequently, is not factored into your AIME calculation.

The Formula: From AIME to Primary Insurance Amount (PIA)

Once your AIME is established, the SSA applies a progressive formula to determine your Primary Insurance Amount (PIA). The PIA is the base figure the government uses to set your benefit if you claim at your Full Retirement Age.

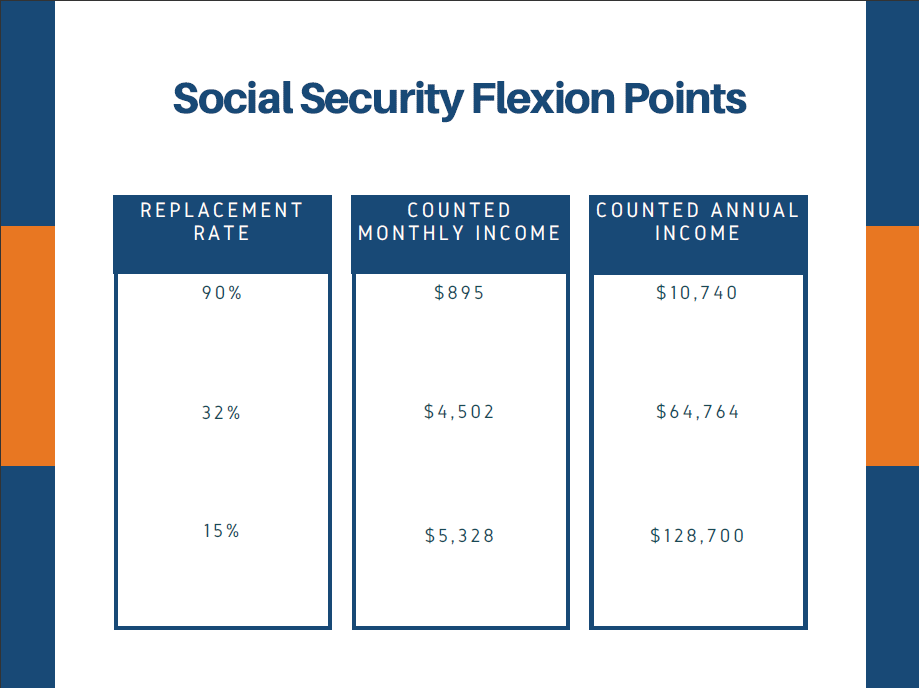

Understanding the “Bend Points”

The Social Security formula is “regressive” in terms of percentage but “progressive” in its social intent. It uses three distinct percentages—90%, 32%, and 15%—applied to different portions of your AIME. These portions are separated by dollar amounts known as “bend points.”

For an individual reaching age 62 in 2024, the formula looks like this:

- 90% of the first $1,174 of AIME.

- 32% of AIME between $1,174 and $7,078.

- 15% of AIME above $7,078.

These bend points change annually to keep pace with national wage trends.

The Progressive Nature of the Benefit

This weighted formula is designed to provide a higher “replacement rate” for lower-income workers. A person with a lower AIME will see the vast majority of their earnings calculated at the 90% rate. In contrast, a high-earner will see a significant portion of their income calculated at the 15% rate. From a personal finance perspective, this means that while higher earners receive more total dollars, Social Security replaces a smaller percentage of their pre-retirement income compared to lower earners. This reality necessitates more aggressive private investing for those in higher tax brackets.

The Timing Factor: Full Retirement Age and Claiming Strategies

The PIA calculated in the previous step is not necessarily what you will receive. The actual amount is heavily influenced by when you choose to begin receiving benefits.

Full Retirement Age (FRA) Variations

Your Full Retirement Age (FRA) is the age at which you are entitled to 100% of your PIA. For anyone born in 1960 or later, the FRA is 67. For those born earlier, it ranges between 66 and 67. Claiming exactly at your FRA ensures you receive the standard amount calculated by the AIME formula without any penalties or bonuses.

The Cost of Early Claiming

You can choose to claim Social Security as early as age 62, but there is a permanent financial trade-off. If you claim at 62 when your FRA is 67, your monthly check is reduced by approximately 30%. This reduction is calculated monthly: the benefit is reduced by 5/9 of 1% for each month before FRA, up to 36 months, and 5/12 of 1% for each month beyond that. For many, the “break-even” point—the age at which the total lifetime value of waiting for a larger check surpasses the total value of taking a smaller check early—is typically in the late 70s or early 80s.

Delayed Retirement Credits

Conversely, the SSA rewards those who delay benefits past their FRA. For every year you wait beyond your FRA (up until age 70), your benefit increases by 8% annually. This is a guaranteed, inflation-adjusted return that is nearly impossible to match in the private market. If your FRA is 67 and you wait until 70, you will receive 124% of your PIA for the rest of your life. For individuals with high life expectancy, delaying is often the most effective way to maximize the “Money” aspect of their retirement strategy.

External Variables Impacting Your Final Check

Beyond the core formula, several external factors can increase or decrease your actual take-home pay from the Social Security Administration.

Cost-of-Living Adjustments (COLA)

One of the most valuable features of Social Security is the Cost-of-Living Adjustment (COLA). Unlike most private pensions, Social Security benefits are adjusted annually based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This ensures that inflation does not erode the purchasing power of your benefits over a 20- or 30-year retirement.

Taxes and the Earnings Test

Personal finance planning must account for the fact that Social Security benefits can be taxable. If your “provisional income” (adjusted gross income + tax-exempt interest + 50% of your Social Security benefits) exceeds certain thresholds, up to 85% of your benefits may be subject to federal income tax.

Additionally, if you claim benefits before your FRA and continue to work, you are subject to the “Earnings Test.” In 2024, if you earn more than $22,320, the SSA will withhold $1 in benefits for every $2 earned above that limit. While these withheld benefits are eventually added back to your check once you reach FRA, it can create a short-term cash flow hurdle for those pursuing side hustles or part-time employment.

Strategic Planning to Maximize Your Monthly Payment

Knowing how the math works allows you to pull specific levers in your financial life to increase your eventual payout.

Increasing Your Earnings Base

Since the formula uses your top 35 years, a high-earning year in your 60s can replace a low-earning year from your 20s. For those who may have taken time off for caregiving or had low-paying early career roles, working just a few extra years at a peak salary can have a disproportionate impact on the AIME and the final PIA.

Coordination with Spousal and Survivor Benefits

In a household, the calculation isn’t just about one person. Spouses are entitled to up to 50% of the higher earner’s PIA if that amount is greater than their own earned benefit. Furthermore, survivor benefits allow a widowed spouse to step into the higher monthly payment of the deceased. A common strategy for couples is for the higher-earning spouse to delay benefits until age 70. This not only maximizes their own lifetime benefit but also locks in the highest possible “safety net” for the surviving spouse.

Conclusion: The Value of Long-Term Financial Literacy

The calculation of Social Security payments is a rigorous process designed to reward long-term participation in the workforce while providing an inflation-protected base for retirement. By understanding the components of the AIME, the progressive nature of bend points, and the massive impact of claiming age, you can move from passive recipient to active strategist.

Social Security should not be viewed in isolation. It is a predictable, government-guaranteed annuity that complements your 401(k), IRA, and other investments. When you master the math behind the payment, you gain the clarity needed to build a robust financial plan that ensures dignity and security throughout your retirement years. Regardless of where you are in your career, the decisions you make today regarding your earnings and your eventual claiming age will echo for decades.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.