In the world of finance, whether you are managing a household budget, overseeing a corporate balance sheet, or navigating the complexities of the stock market, numbers are the primary language of progress. Among the various mathematical tools at a financier’s disposal, the ability to calculate and interpret a percentage reduction is perhaps one of the most vital. It is the metric that defines the success of a cost-cutting initiative, the severity of a market correction, and the true value of a seasonal discount.

Understanding how to work out a percentage reduction is more than just a classroom exercise; it is a fundamental skill for anyone looking to optimize their wealth and improve their financial literacy. By mastering this calculation, you gain the ability to strip away marketing jargon and see the raw data behind every financial decision. This guide explores the mechanics of percentage reduction within the “Money” niche, providing you with the insights needed to apply these formulas to personal finance, investing, and business operations.

The Fundamentals of Percentage Reduction in Finance

Before applying mathematics to complex investment portfolios, one must first master the basic arithmetic of the reduction. A percentage reduction represents the decrease in value of an asset or cost relative to its original amount, expressed as a fraction of 100. In financial terms, this allows for a standardized comparison across different scales—whether you are looking at a $5 discount on a shirt or a $5 million reduction in corporate overhead.

Understanding the Core Formula: New vs. Old Values

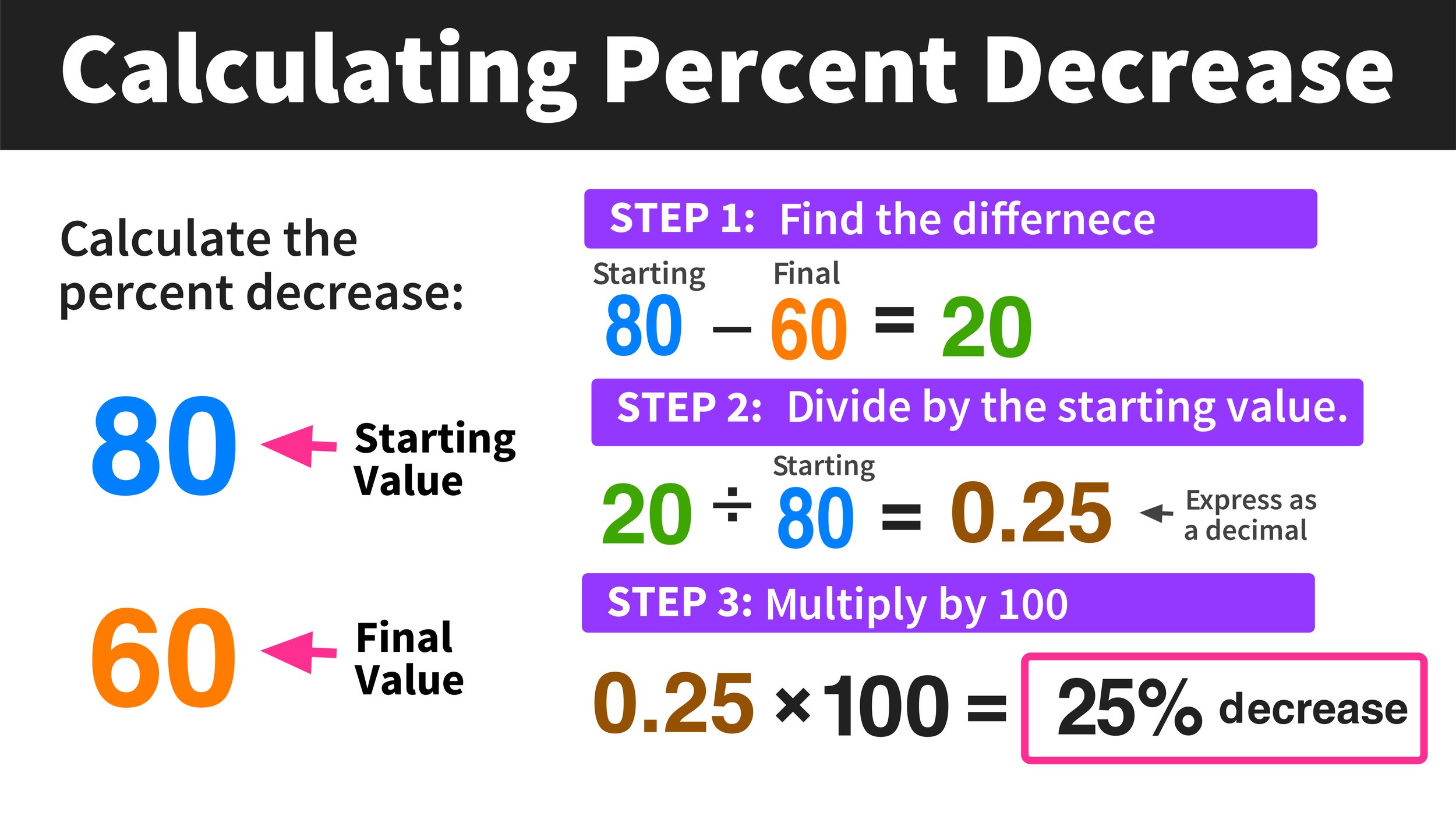

The mathematical formula for calculating a percentage reduction is straightforward, yet its implications are profound. To find the percentage decrease between an original value and a new, lower value, follow these steps:

- Subtract the new value from the original value to find the “decrease.”

- Divide that decrease by the original value.

- Multiply the result by 100 to get the percentage.

Mathematically, it looks like this:

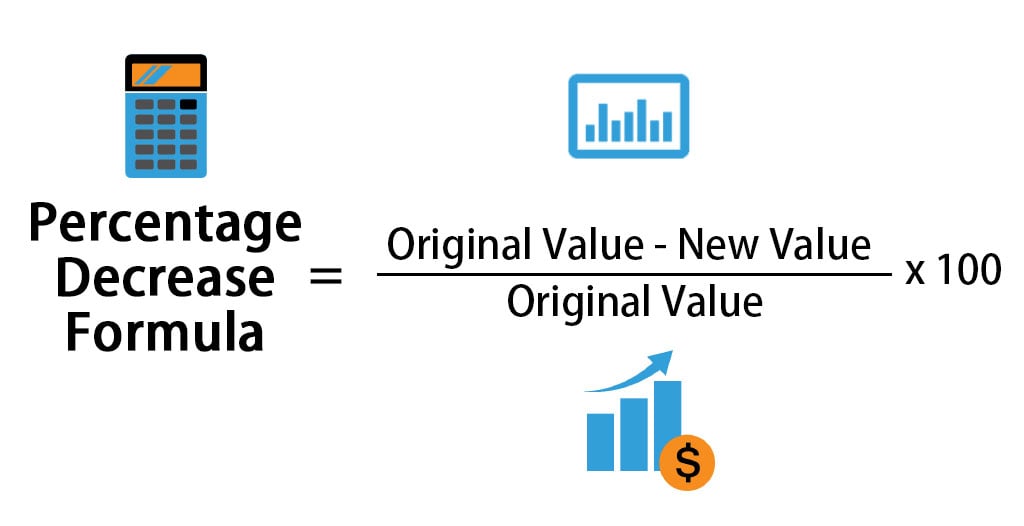

((Original Value – New Value) / Original Value) * 100 = Percentage Reduction

For example, if an investor bought a stock at $200 and its value dropped to $150, the calculation would be: ($200 – $150) / $200 = 0.25. Multiplying by 100 gives a 25% reduction. Understanding this formula is the first step in moving from a passive observer of your finances to an active manager of your capital.

Why Precision Matters in Personal Finance

In personal finance, “rounding errors” or a lack of precision can lead to significant leaks in a budget. When you work out a percentage reduction in your monthly expenses—such as negotiating a lower premium on insurance or switching to a more efficient utility provider—knowing the exact percentage helps you benchmark your progress.

A 10% reduction in a high-cost category, like housing or transport, often yields more significant real-dollar savings than a 50% reduction in a low-cost category like entertainment. By calculating the percentage, you can prioritize your efforts on the areas of your financial life that offer the highest impact.

Leveraging Percentage Reductions for Strategic Investing

For investors, percentage reductions are often associated with “drawdowns”—the peak-to-trough decline during a specific record period of an investment. Strategic investing requires a cold, analytical look at these reductions to manage risk and understand the volatility of an asset class.

Analyzing Market Drawdowns and Portfolio Recoveries

When the stock market enters a “correction” (a 10% reduction) or a “bear market” (a 20% or more reduction), investors must keep a level head. Calculating the percentage reduction of your total portfolio during these times allows you to assess whether your asset allocation is performing within its expected risk parameters.

For instance, if the S&P 500 drops by 15%, but your diversified portfolio only experiences an 8% reduction, your risk-mitigation strategies are working. Conversely, if your portfolio drops by 25% in the same period, you are over-leveraged or over-exposed to high-beta assets. Knowing how to calculate these figures allows for data-driven adjustments rather than emotional reactions.

The “Break-even” Trap: Why a 50% Loss Needs a 100% Gain

One of the most critical lessons in financial mathematics is the asymmetry of percentage reductions and gains. This is a concept that every investor must internalize: it is much harder to recover from a loss than it is to experience one.

If your investment portfolio suffers a 10% reduction, you do not need a 10% gain to get back to even; you need an 11.1% gain. If you suffer a 50% reduction, you need a staggering 100% gain—a doubling of your money—just to return to your starting point. This mathematical reality highlights the importance of capital preservation. By understanding the math behind percentage reductions, savvy investors learn to prioritize “downside protection” to avoid the deep mathematical holes that are difficult to climb out of.

Business Finance: Optimizing Profitability through Cost Reduction

In the corporate world, percentage reduction is the primary metric for efficiency. Business owners and financial officers use these calculations to measure the success of Lean initiatives, negotiate with vendors, and improve the bottom line without necessarily having to increase sales volume.

Calculating Operational Overhead Decreases

For a business to scale sustainably, it must often reduce its overhead as a percentage of its total revenue. If a company generates $1 million in revenue with $400,000 in expenses, its overhead is 40%. If, through better systems and automation, they reduce those expenses to $350,000 while maintaining revenue, they have achieved a 12.5% reduction in costs.

However, more importantly, they have improved their profit margin. By calculating these reductions monthly, management can identify which departments are becoming more efficient and which are lagging. It provides a standardized “scorecard” that transcends the raw dollar amounts, which can fluctuate based on seasonal demand.

Evaluating the Impact of Vendor Discounts on Gross Margin

Procurement is another area where mastering percentage reduction pays dividends. When a supplier offers a “volume discount,” a business owner must calculate the percentage reduction in the unit price to see if it justifies the increased inventory carrying costs.

If a component costs $10.00 and a bulk order reduces it to $9.20, that is an 8% reduction. If the cost of storing that extra inventory increases your warehouse expenses by 10%, the “discount” is actually costing the business money. Being able to quickly work out these percentage reductions allows for better negotiation and smarter resource allocation.

Consumer Finance: Mastering the Art of Discounting and Savings

On a daily basis, we are bombarded with offers of “20% off” or “Save 30% today.” Without a firm grasp of how to calculate these reductions, consumers often fall prey to “sale fatigue” or deceptive pricing practices.

Deciphering Retail Sales and Unit Price Reductions

Retailers often use percentage reductions to move inventory, but not all sales are created equal. A “30% reduction” on an item that was marked up by 50% last week is not a true saving. Savvy consumers use the percentage reduction formula to compare the value of different offers.

For example, is it better to take “Buy Two, Get One Free” or “33% off everything”? By converting the “free” offer into a percentage reduction (1 divided by 3, which is 33.3%), you can see that the offers are nearly identical. This level of financial clarity prevents impulse spending and ensures that your “savings” are actual reductions in the outflow of your wealth.

The Long-term Impact of Interest Rate Reductions on Debt

One of the most powerful applications of percentage reduction in money management is in debt service. A seemingly small reduction in the interest rate of a mortgage or a student loan can result in tens of thousands of dollars saved over the life of the loan.

If you refinance a $300,000 mortgage from a 6% interest rate to a 4.5% interest rate, you have achieved a 25% reduction in the interest rate itself. While 1.5% sounds small, the compounded effect over 30 years is massive. Calculating the percentage reduction in your monthly interest payment provides the motivation needed to go through the paperwork of refinancing, as it clearly illustrates the increase in your future net worth.

Digital Tools and Automation for Financial Calculations

While knowing how to perform these calculations manually is essential for “on-the-fly” decision-making, modern finance relies heavily on digital tools to handle bulk data and complex scenarios.

Utilizing Spreadsheet Formulas for Bulk Data Analysis

For anyone serious about their money, Microsoft Excel or Google Sheets are indispensable. To work out percentage reduction across hundreds of budget line items or stock prices, you can use a simple formula. If your original value is in cell A2 and your new value is in cell B2, the formula is:

=(A2-B2)/A2

By formatting the result as a percentage, you can instantly see the reduction across an entire year of data. This allows for “Horizontal Analysis” in financial statements—comparing this year’s expenses to last year’s to see exactly where the largest percentage reductions (or increases) are occurring.

Modern Financial Calculators and Apps

Beyond spreadsheets, specialized financial calculators and mobile apps can help you work out percentage reductions for specific niches, such as real estate (cap rate reductions) or retail (margin calculators). These tools often incorporate the “Time Value of Money,” allowing you to see how a percentage reduction in expenses today translates into a larger portfolio value in twenty years.

In conclusion, the ability to work out a percentage reduction is a foundational pillar of financial intelligence. It allows you to navigate the stock market with a clear head, run a business with surgical precision, and manage your personal household budget with the eye of a professional auditor. By looking past the raw numbers and focusing on the percentages, you gain a clearer perspective on the direction of your financial journey, ensuring that every reduction in cost or risk is a step toward greater wealth and stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.