In the modern financial landscape, the line between traditional banking and digital wallets has become increasingly blurred. Cash App, developed by Block, Inc., has evolved from a simple peer-to-peer (P2P) payment tool into a robust financial ecosystem that handles everything from tax filings to Bitcoin investing. However, for most users, the core utility remains the ability to receive money and, more importantly, move that money into a traditional bank account where it can be used for mortgages, car payments, or long-term savings.

Understanding the mechanics of transferring funds from Cash App to your bank is not just a technical necessity; it is a fundamental aspect of managing personal liquidity. Whether you are a freelancer receiving client payments or an individual splitting a dinner bill, knowing how to navigate fees, timing, and security protocols is essential for sound financial health.

Understanding the Cash App Financial Ecosystem

Before initiating a transfer, it is vital to understand where your money “lives” within the Cash App environment. Unlike a traditional bank account, your Cash App balance is a digital ledger held by a non-bank financial institution. While Cash App offers banking services through partners like Lincoln Savings Bank or Community Federal Savings Bank, the funds in your app balance are often treated differently than those in a standard checking account.

The Distinction Between Digital Wallets and Traditional Accounts

A digital wallet acts as an intermediary. When someone sends you money on Cash App, it stays in the app’s internal ledger. While you can spend this money directly using a Cash Card, the funds are not yet part of your broader banking ecosystem. Transferring these funds to a traditional bank account “finalizes” your liquidity, allowing you to integrate those earnings into your primary financial planning tools, high-yield savings accounts, or investment portfolios.

Why Liquidity Management Matters

In personal finance, liquidity is king. Keeping too much money in a P2P app can be risky; these accounts do not always offer the same robust consumer protections or interest-earning potential as a dedicated bank account. By regularly transferring your Cash App balance to a bank, you ensure your capital is working for you—whether that means earning 4% APY in a savings account or being protected by the full weight of FDIC insurance.

The Role of Linked Accounts

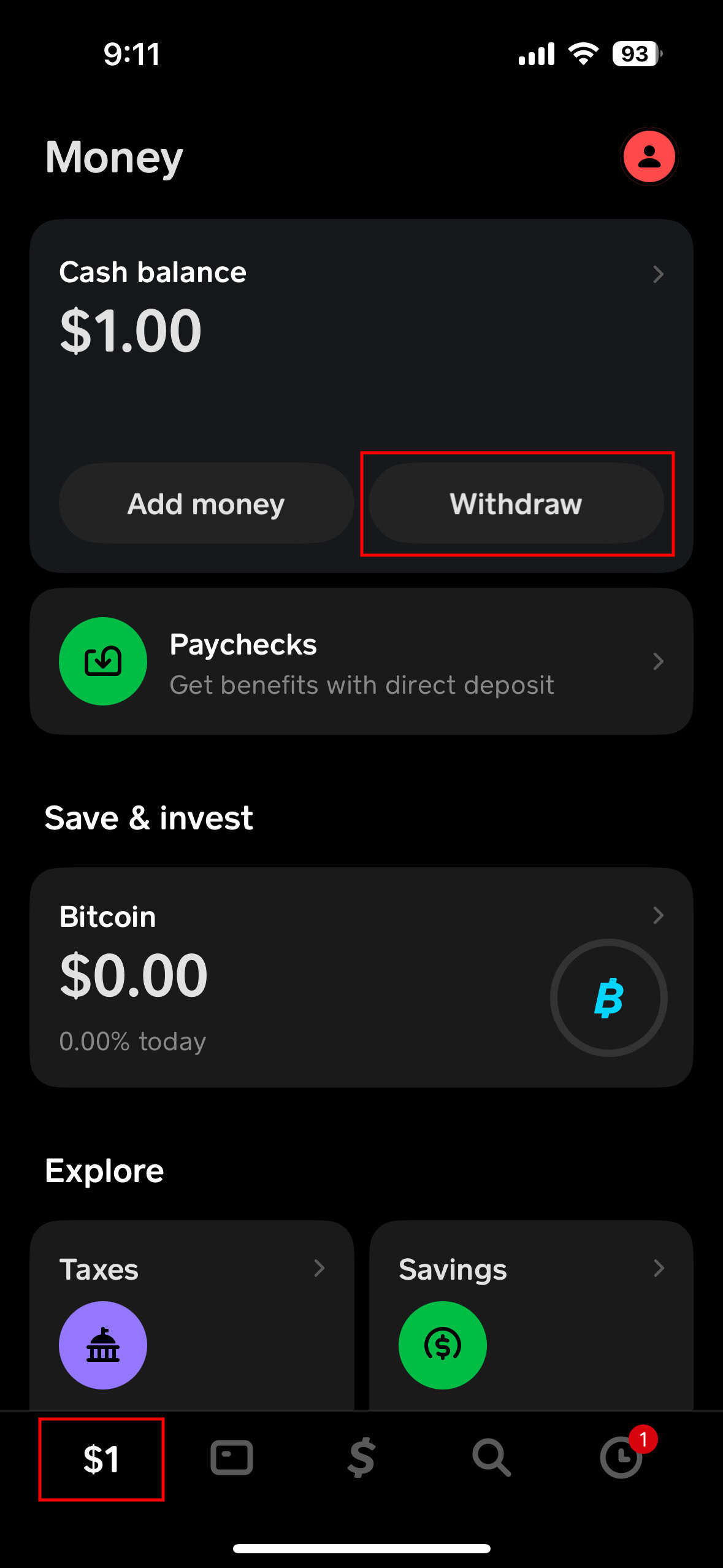

To move money out, you must first bridge the gap between the app and your bank. Cash App allows you to link both a debit card and a bank account via the ACH (Automated Clearing House) network. The debit card link is typically used for “Instant Transfers,” while the direct bank account link (using routing and account numbers) is used for “Standard Transfers.”

The Step-by-Step Mechanics of Transferring Funds

Transferring money out of Cash App is a straightforward process, but the choices you make during the procedure can impact your bottom line. Cash App offers two primary methods for moving money: Standard and Instant.

How to Initiate the “Cash Out” Process

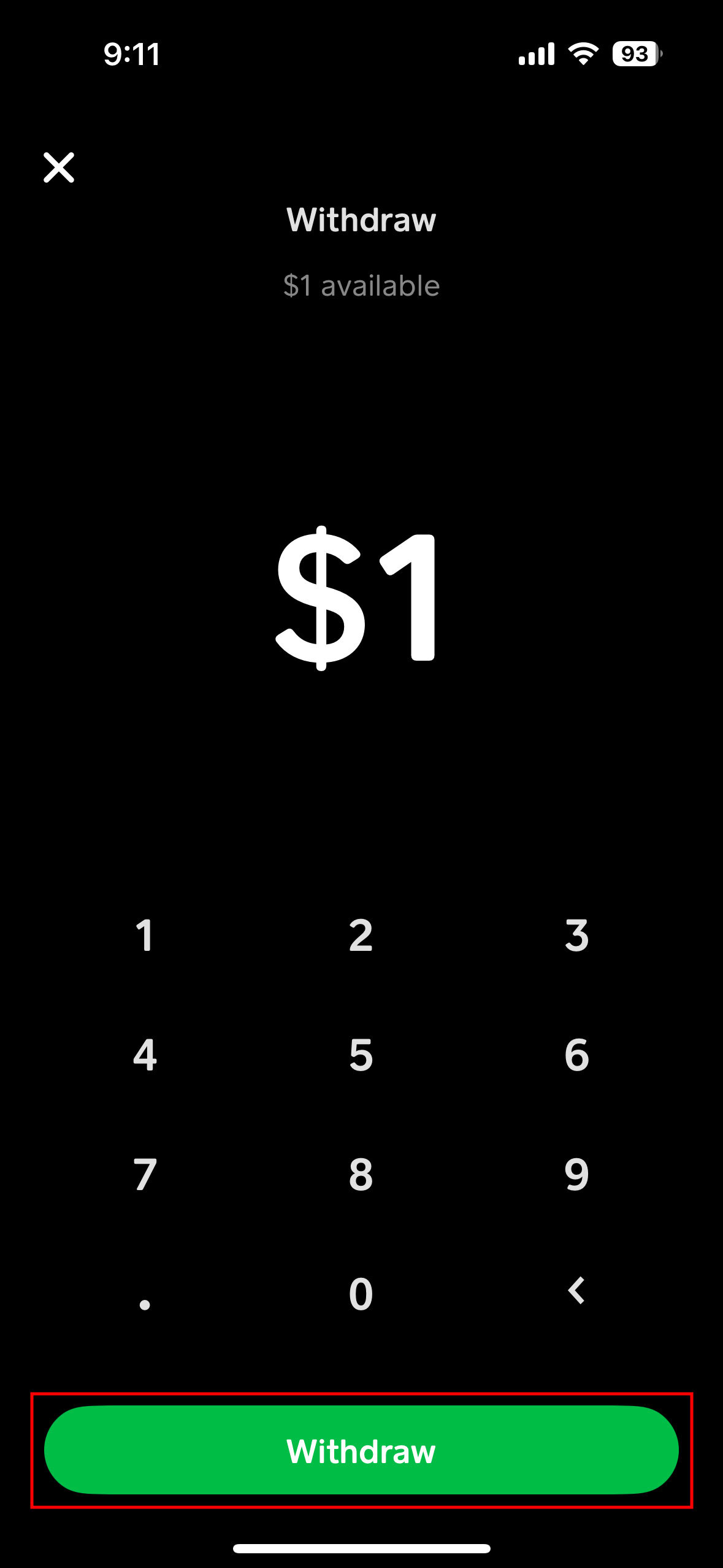

To begin, you must navigate to the “Money” tab on your Cash App home screen (the icon that looks like a dollar sign or a bank building). Once there, you will see your current balance and a “Cash Out” button. Upon clicking this, you will be prompted to choose the amount you wish to transfer. After selecting the amount, you are faced with the most important decision in the process: the speed of the transfer.

The Standard Transfer: Cost-Effective Management

The Standard Transfer is the preferred method for anyone practicing disciplined financial management. This method utilizes the ACH network to move funds.

- Cost: Free.

- Timeline: Usually 1 to 3 business days.

- Strategic Use: This is ideal for non-urgent funds, such as side hustle earnings or reimbursed expenses that aren’t needed for immediate bills. By choosing this option, you avoid the erosion of your capital through convenience fees.

The Instant Transfer: Paying for Velocity

For situations where immediate liquidity is required, Cash App offers the Instant Transfer. This method sends the funds to your linked debit card almost immediately.

- Cost: A fee ranging from 0.25% to 1.75% (with a minimum fee of $0.25).

- Timeline: Within minutes.

- Strategic Use: This should be reserved for financial emergencies or time-sensitive payments. For high-volume users, these fees can accumulate significantly over a year, potentially costing hundreds of dollars in lost interest or capital.

Optimizing Fees, Limits, and Financial Security

A professional approach to money management requires an eye for detail, especially regarding the hidden costs of digital transactions. While a 1.75% fee might seem negligible on a $20 transfer, it becomes a significant expense when dealing with larger sums or frequent transactions.

Analyzing the Impact of Instant Transfer Fees

If you transfer $1,000 via the Instant method at a 1.75% fee, you are paying $17.50 for the convenience of speed. In the world of personal finance, that $17.50 could have been invested in a fractional share of an ETF or used to cover a monthly subscription service. Managing your “transfer behavior” is a simple way to increase your net savings over time. Plan your transfers ahead of weekends and holidays to ensure the “Standard” 1-3 day window aligns with your needs.

Navigating Transfer Limits and Regulations

Cash App imposes limits on how much you can move, which is a critical consideration for business users or those using the app for significant transactions.

- Instant Limits: Generally, you can transfer up to $25,000 per transaction via Instant Transfer.

- Standard Limits: These can be higher, but are often subject to account verification status.

- Regulatory Oversight: Large transfers (typically those exceeding $10,000) may be subject to reporting requirements by financial institutions to comply with Anti-Money Laundering (AML) laws. Always ensure your account is fully verified with your legal name and SSN to prevent funds from being “flagged” or held during transit.

Security Best Practices for Digital Transfers

Transferring money is the moment of highest risk in the digital payment cycle. To protect your capital:

- Enable Security Locks: Require a PIN or Touch ID for every transfer.

- Verify Linked Accounts: Double-check that the linked bank account is indeed yours and that the account numbers are correct. A typo in an ACH transfer can lead to weeks of administrative headaches to recover the funds.

- Watch for Scams: Cash App will never call you to “verify” a transfer. If you receive a request to send money back to “cancel” a pending transfer, it is a scam.

Strategic Integration into Your Financial Plan

To truly master your money, you should treat Cash App not as a standalone island, but as a spoke in your broader financial wheel. This involves setting up systems that automate the flow of money into productive assets.

Using Cash App for Side Hustle Income

Many modern workers use Cash App to receive payments for side gigs. To keep your personal and business finances separate—a key tenet of professional money management—you should designate a specific bank account for these transfers. When you “Cash Out,” send those funds directly to a dedicated business or “tax savings” account. This makes it significantly easier to track income and prepare for quarterly tax obligations.

The “Buffer” Strategy

A common mistake is waiting until your bank account hits zero before cashing out from the app. A more sophisticated strategy is to maintain a “buffer” in your traditional checking account and use the Standard (free) transfer method exclusively. By keeping a small cushion of cash in your bank, you remove the “need” for the Instant Transfer, effectively giving yourself a 1.75% “raise” on every dollar you move.

Leveraging the Cash Card for Bridge Liquidity

If you need to spend your Cash App balance immediately but don’t want to pay the Instant Transfer fee, consider using the Cash Card. This is a Visa debit card that spends directly from your Cash App balance. By using the card for daily expenses (groceries, gas), you are effectively “transferring” the value of your balance into the real world without paying the 1.75% “convenience tax.” You can then keep your bank balance untouched, achieving the same net result as a transfer.

![]()

Conclusion: Developing a Digital Transfer Protocol

The ability to move money seamlessly between Cash App and your bank is a powerful tool for the modern consumer. However, the most successful financial actors are those who move money with intention. By choosing the Standard Transfer whenever possible, staying mindful of fee structures, and integrating these movements into a larger financial strategy, you turn a simple app interaction into a disciplined wealth-management habit.

In summary, remember the three pillars of digital liquidity: Planning (avoiding instant fees), Security (protecting your transit), and Purpose (moving money toward long-term goals). As the fintech world continues to evolve, maintaining this level of control over your capital ensures that your money is always working for you, rather than for the platforms that host it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.