The landscape of personal finance has undergone a seismic shift over the last decade. Gone are the days when settling a debt with a friend or paying a local vendor required a physical trip to an ATM or the cumbersome exchange of bank account numbers. Today, fintech platforms have democratized access to liquid capital, turning the smartphone into a high-powered financial hub. At the forefront of this revolution is Cash App, a versatile financial tool that has redefined how we perceive and move money.

Understanding how to send money via Cash App is more than just a technical skill; it is an essential component of modern financial literacy. Whether you are managing household expenses, splitting a dinner bill, or paying a freelancer, mastering this platform ensures your capital remains fluid and your transactions remain secure.

The Evolution of Mobile Finance: Why Cash App is a Pillar of Personal Finance

To understand the utility of sending money via Cash App, one must first recognize its position within the broader financial ecosystem. Developed by Block, Inc. (formerly Square), Cash App was designed to bridge the gap between traditional banking and the immediate needs of the digital-first consumer. It serves as a comprehensive financial tool that integrates peer-to-peer (P2P) payments, banking services, and even investment opportunities.

The Shift from Traditional Banking to App-Based Ecosystems

Traditional banking systems are often characterized by latency. Wire transfers can take days, and ACH transfers are rarely instantaneous. Cash App circumvents these legacy hurdles by creating a closed-loop ecosystem where transfers between users happen in real-time. This “instant” nature of capital movement is vital for personal financial agility. For many users, Cash App acts as a secondary bank account, providing a layer of separation between their primary savings and their daily discretionary spending.

Financial Sovereignty and the Digital Wallet

The concept of a “digital wallet” is central to the Money niche. By holding a balance in Cash App, users exercise a form of financial sovereignty. They are no longer tethered to the physical hours of a brick-and-mortar institution. Sending money becomes a 24/7 activity, allowing for global connectivity and local convenience. This shift represents a transition from institutional control to individual empowerment in the management of personal wealth.

A Step-by-Step Financial Manual: Sending Money with Precision

Executing a transaction on Cash App is designed to be intuitive, yet it requires a high level of precision to ensure funds reach the correct destination. In the world of digital finance, errors can be difficult to reverse, making it imperative to follow a disciplined process.

Setting Up Your Digital Wallet for Success

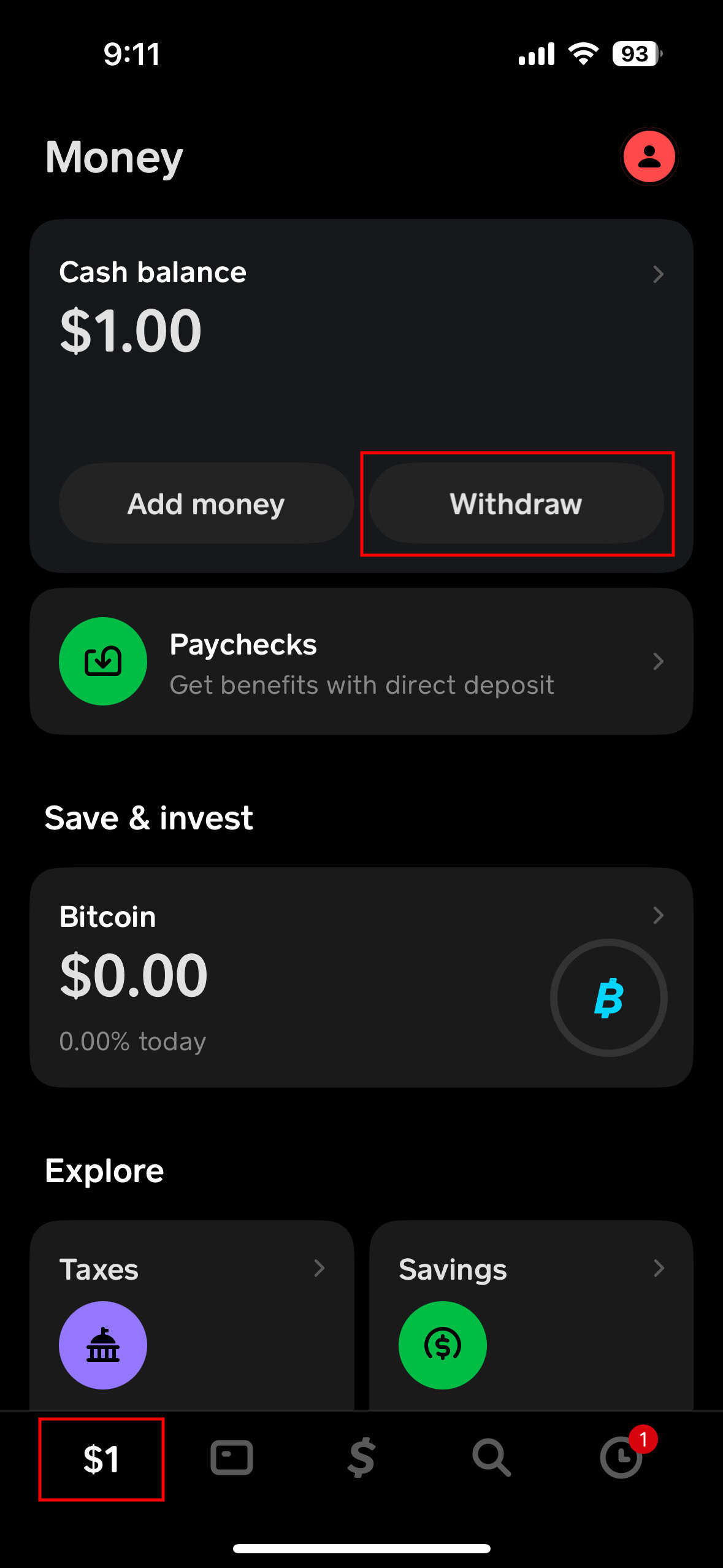

Before a single dollar is sent, your financial foundation must be secure. This involves linking a primary funding source—typically a debit card or a bank account. From a personal finance perspective, linking a debit card is often preferred for sending money because it facilitates the “Instant” transfer feature. Once your account is funded or your card is linked, the “Cash Balance” serves as your primary ledger for outgoing payments.

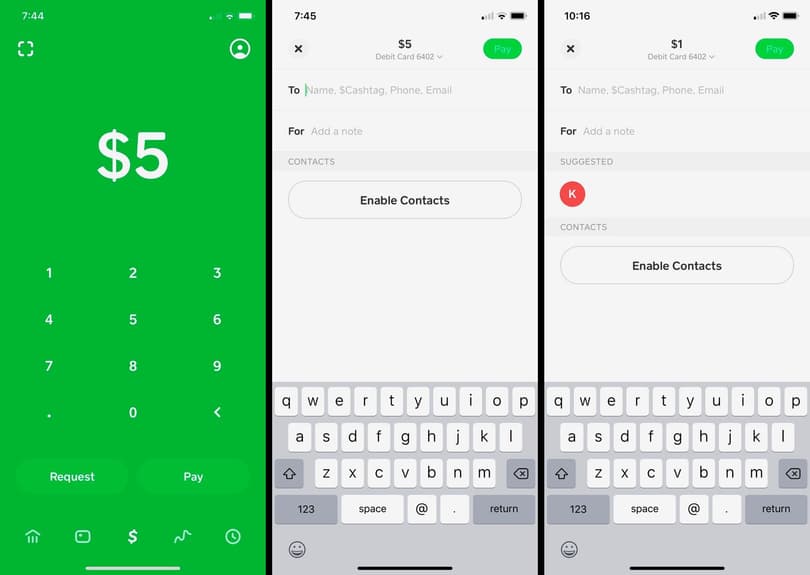

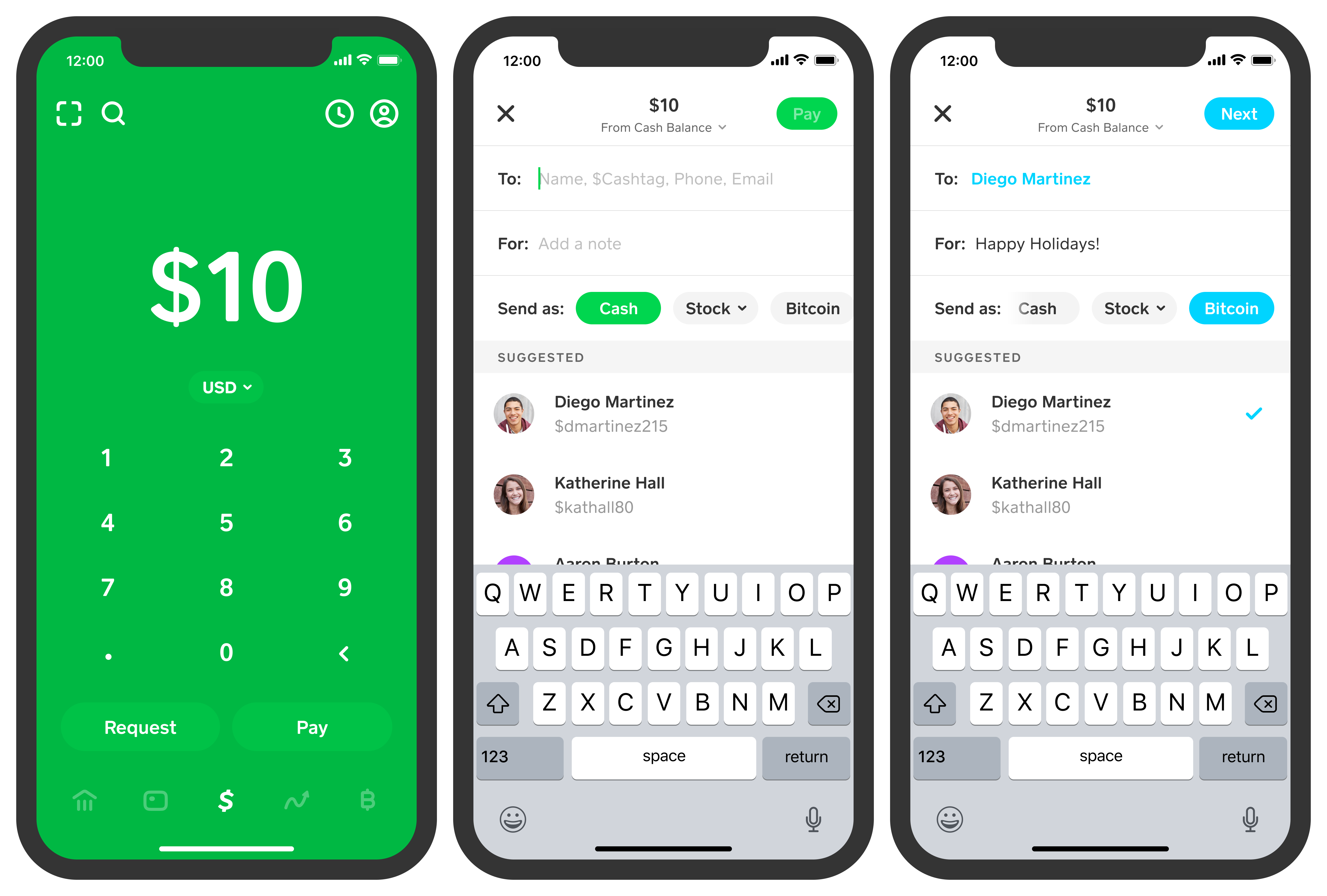

Executing the Transaction: Tags, Phone Numbers, and Emails

To send money, you begin by opening the app and entering the desired amount. The platform offers three primary ways to identify a recipient:

- The $Cashtag: A unique identifier that acts as a financial username. Using a $Cashtag is the most secure method, as it minimizes the risk of mistyping a sensitive phone number.

- Phone Number: Directly pulls from your contacts or manual entry.

- Email Address: Useful for business-to-consumer transactions.

Once the recipient is identified, a brief note or “For” memo should be added. In professional or business finance contexts, this memo serves as an essential digital receipt for bookkeeping and tax reconciliation.

Understanding Instant vs. Standard Transfers

A critical component of managing your money on Cash App is understanding the mechanics of “cashing out” or receiving funds. When you send money, the recipient receives it in their Cash App balance immediately. However, when moving that money to a traditional bank account, you face a choice:

- Standard Transfers: These are free and typically take 1–3 business days. This is the choice for those practicing patient capital management.

- Instant Transfers: For a small percentage fee (usually 0.5% to 1.75%), funds are moved to a debit card immediately. This is a tool for liquidity management when immediate cash flow is required.

Managing Your Cash App Balance: Fees, Limits, and Fiscal Responsibility

Effective financial management requires a keen eye on the “hidden” costs of doing business. While Cash App is largely free for personal use, there are specific parameters that every user must navigate to maintain fiscal health.

Decoding the Fee Structure for Personal and Business Accounts

For the average user, sending money from a linked bank account or Cash App balance is free of charge. However, using a credit card to send money incurs a 3% fee. From a personal finance standpoint, using a credit card for P2P transfers is generally discouraged, as the high fee and potential “cash advance” interest rates from the card issuer can quickly erode your net worth.

Furthermore, users who utilize Cash App for business (selling goods or services) are subject to a standard processing fee of 2.75% per transaction. Distinguishing between personal and business accounts is vital for accurate financial reporting.

Navigating Transaction Limits and Identity Verification

To prevent money laundering and ensure financial security, Cash App imposes limits on unverified accounts. Initially, users may be limited to sending $250 within any 7-day period and receiving $1,000 within any 30-day period.

To increase these limits—an essential move for anyone using the app for significant financial transactions—you must complete the identity verification process. This involves providing your full legal name, date of birth, and the last four digits of your Social Security Number. Once verified, limits are significantly increased, allowing for the movement of larger tranches of capital.

Tax Implications and Reporting for P2P Transactions

In recent years, the IRS has increased its scrutiny of digital payment platforms. Under current regulations, platforms like Cash App are required to report business transactions that exceed certain thresholds via Form 1099-K. While sending money to a friend for a shared pizza is not a taxable event, using the platform for a side hustle or freelance work carries tax obligations. Maintaining clear records of every “send” and “receive” is a hallmark of a responsible financial strategy.

Maximizing Your Money: Cash Card, Boosts, and Financial Growth

Cash App is not merely a pipeline for sending money; it is a tool for capital optimization. By integrating the “Cash Card” and “Boosts,” users can actually save money while they spend, creating a virtuous cycle of financial efficiency.

Leveraging “Cash Card” Boosts for Instant Savings

The Cash Card is a free Visa debit card linked to your Cash App balance. The “Boost” feature allows users to select specific discounts at popular retailers, coffee shops, and grocery stores. For example, a 10% Boost at a grocery store results in an immediate discount at the point of sale. In the context of personal finance, these small, consistent savings contribute to a higher overall savings rate, which can then be diverted into long-term investments.

Integrating Cash App into a Broader Investment Strategy

Perhaps the most unique aspect of Cash App in the money niche is its integration of equities and cryptocurrency. The money you receive from a friend can be immediately diverted into fractional shares of stocks or Bitcoin. This removes the friction typically associated with moving money from a payment app to a brokerage account. By automating “round-ups” or investing small portions of your balance, you can utilize Cash App as a gateway to wealth accumulation.

Protecting Your Wealth: Advanced Security Protocols for Digital Transfers

In the digital age, financial security is synonymous with financial success. Because Cash App transfers are near-instant and often irreversible, protecting your account is the most important part of the “sending money” process.

Identifying and Avoiding Common Financial Scams

Scammers often leverage the speed of Cash App to defraud users. Common tactics include “accidental” payments where a stranger asks you to send money back, or “Cash App Fridays” giveaways that require an initial “clearance fee.” A professional approach to finance involves a healthy skepticism: never send money to someone you do not know, and never “test” a transaction with a stranger.

Utilizing Two-Factor Authentication and Security Locks

To safeguard your capital, Cash App provides several security layers. Enabling the “Security Lock” feature requires a passcode or biometric (FaceID/TouchID) verification for every single transfer. Additionally, enabling text or email notifications for every transaction ensures that you have a real-time audit trail of your money’s movement. If you notice unauthorized activity, the ability to “Lock” your Cash Card instantly from the app is a powerful tool in preventing further financial loss.

Conclusion: The Future of Your Wallet

Mastering how to send money from Cash App is an entry point into a larger world of digital financial management. By understanding the nuances of transaction speeds, fee structures, tax implications, and security protocols, you transform a simple app into a robust financial instrument.

As we move toward an increasingly cashless society, the ability to navigate these platforms with professional-grade precision will separate those who simply spend money from those who manage it effectively. Whether you are using it for daily convenience or as a component of your broader investment and savings strategy, Cash App represents the intersection of technology and personal finance—a space where your money moves at the speed of your life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.