In the rapidly evolving landscape of fintech, few platforms have achieved the cultural ubiquity and financial success of Cash App. Originally launched by Block, Inc. (formerly Square) in 2013 as “Square Cash,” the platform began as a simple peer-to-peer (P2P) payment service designed to compete with Venmo. However, over the last decade, it has morphed into a comprehensive financial “super-app” that serves as a bank, a brokerage, a Bitcoin exchange, and a tax preparer for millions of users.

For the casual user, Cash App often feels like a free service. You can send $20 to a friend for dinner or receive a birthday gift from a relative without paying a dime. This leads to a logical question for the financially curious: How does a company that offers so much for free generate billions of dollars in annual revenue? The answer lies in a sophisticated multi-layered business model that monetizes convenience, merchant relationships, and high-frequency financial activities.

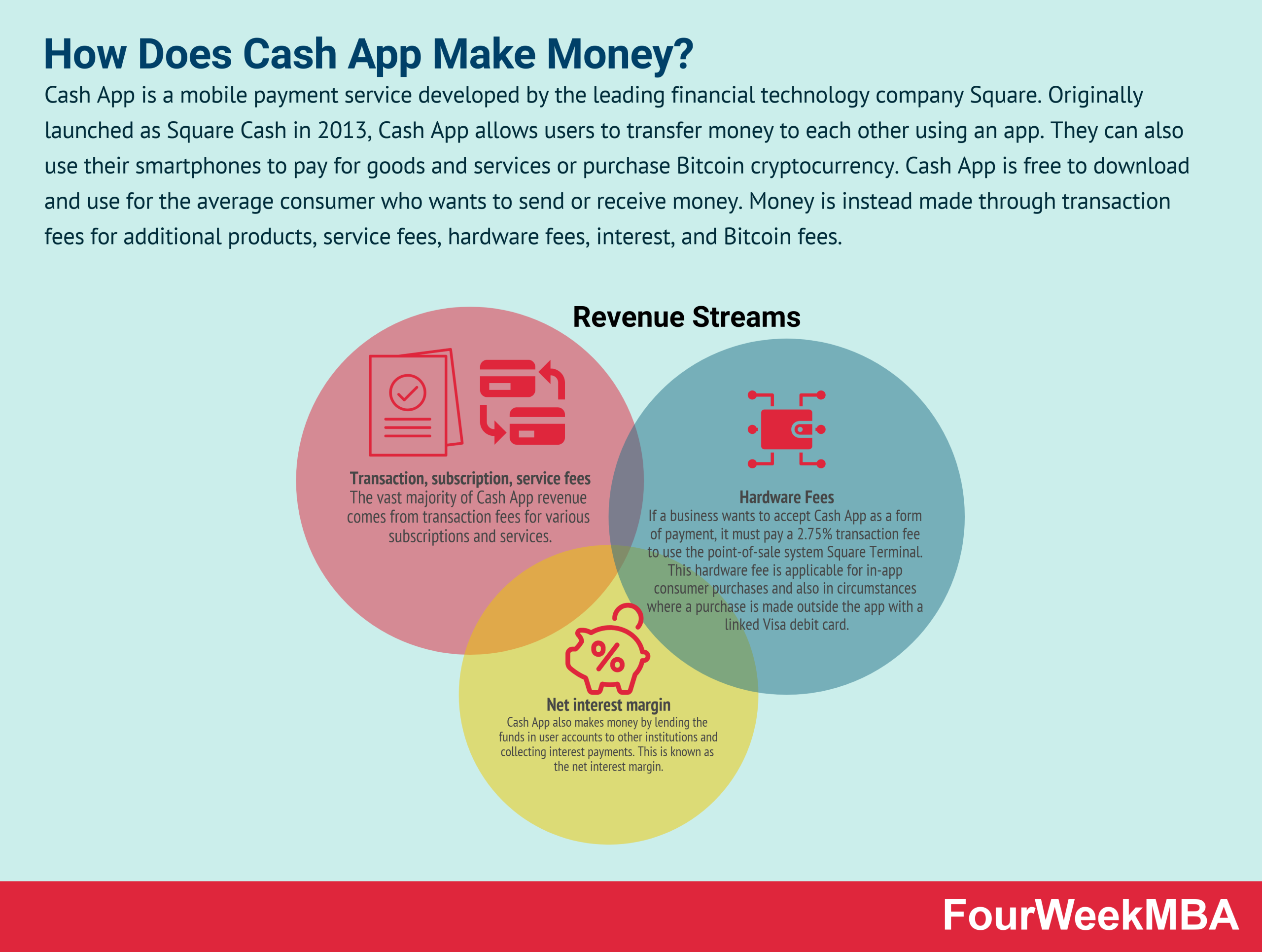

Transactional Revenue: Monetizing the Need for Speed and Credit

The bedrock of Cash App’s revenue model is built on the friction points of traditional banking. While standard transfers between users are free, Cash App identifies specific moments where users are willing to pay for convenience or the use of credit.

Instant Deposit Fees

Perhaps the most visible revenue generator for Cash App is the “Instant Deposit” feature. When a user receives money in their Cash App balance, they have two choices: they can transfer it to their linked bank account for free (which typically takes 1–3 business days via the ACH network), or they can opt for an Instant Deposit.

For the privilege of moving money to a debit card immediately, Cash App charges a fee ranging from 0.5% to 1.75% (with a minimum fee of $0.25). In an era where “liquidity is king,” millions of users—particularly those in the gig economy or those living paycheck to paycheck—willingly pay this small premium to access their funds instantly. For Block, these micro-transactions aggregate into hundreds of millions of dollars in high-margin revenue.

Credit Card Transaction Surcharges

Cash App allows users to link credit cards to their accounts to fund P2P payments. However, unlike transfers funded by a bank account or a debit card, sending money via a credit card incurs a 3% processing fee. This fee covers the interchange costs charged by card networks (Visa/Mastercard) while leaving a small margin for Cash App. By offering this feature, Cash App ensures that users can settle debts even when they lack immediate cash, effectively monetizing the user’s access to credit.

Cash Card Interchange Fees

The “Cash Card” is a customizable Visa debit card linked to a user’s Cash App balance. While the card is free to order (in its basic form), it serves as a massive revenue driver through interchange fees. Every time a user swipes their Cash Card at a grocery store, a gas station, or an online retailer, the merchant pays a small percentage of the transaction to the card issuer and the network. Cash App receives a portion of this fee. As users shift more of their daily spending away from traditional bank cards and toward their Cash Card, Block captures a growing slice of the massive consumer spending pie.

Business and Merchant Services: The “Pro” Ecosystem

While Cash App is primarily known as a consumer tool, it has made significant inroads into the business sector. By positioning itself as an alternative to traditional merchant accounts, Cash App has created a streamlined revenue stream from entrepreneurs and small businesses.

Cash for Business Accounts

Cash App offers “Business Accounts” for individuals selling goods or services. Unlike personal accounts, which are free to use for receiving money, Business Accounts are charged a flat 2.75% fee on every payment received. For many micro-merchants, such as hairstylists, photographers, or local artisans, this 2.75% fee is a fair trade for the simplicity of the interface and the ability to accept payments from a massive existing user base without needing a separate point-of-sale (POS) terminal.

Cash App Pay

Cash App Pay is a relatively newer integration that allows users to pay third-party merchants directly using their Cash App balance or linked debit card by scanning a QR code or selecting the option at an online checkout. For merchants, this offers a streamlined checkout experience that often has higher conversion rates than traditional credit card entries. For Cash App, it provides another avenue to collect transaction fees from the merchant side, further diversifying their income away from the individual consumer.

The Bitcoin Engine: Driving Volume and Engagement

One of the most significant pivots in Cash App’s history was its early adoption of Bitcoin. Under the leadership of Jack Dorsey, Block integrated Bitcoin buying and selling into Cash App in 2018. Since then, Bitcoin has become a primary driver of the app’s gross revenue, though it operates on lower margins than other services.

The Spread and Service Fees

When a user buys or sells Bitcoin on Cash App, the platform generates revenue in two ways. First, it charges a small service fee for the transaction. Second, it applies a “spread”—the difference between the market price of Bitcoin and the price offered to the user. While these fees are competitive, the sheer volume of Bitcoin transactions on the platform is staggering. In peak bull markets, Bitcoin revenue can account for more than half of Cash App’s total revenue, acting as a powerful engine for top-line growth.

On-Ramping the “Unbanked” and Tech-Savvy

Beyond direct transaction fees, Bitcoin serves as a customer acquisition tool. By providing an easy, “one-click” way to enter the cryptocurrency market, Cash App attracts a demographic that might not have otherwise engaged with the app. Once these users are in the ecosystem for Bitcoin, they are more likely to use the Cash Card, opt for Instant Deposits, or explore the app’s other financial products. This “cross-selling” strategy increases the lifetime value (LTV) of every user who joins for the crypto features.

Investing and Advanced Financial Tools

Cash App has strategically expanded into broader personal finance categories, transforming from a wallet into a full-scale financial hub. By lowering the barriers to entry for investing, they have unlocked new ways to monetize user behavior.

Cash App Investing

Cash App allows users to buy fractional shares of stocks for as little as $1. While Cash App does not currently charge commissions for buying or selling stocks—following the industry trend popularized by Robinhood—the feature serves a vital role in user retention. The more “sticky” a user’s relationship with the app (i.e., the more of their net worth that resides within the app), the more likely they are to use other revenue-generating features. Additionally, there are back-end monetization strategies for stock platforms, such as earning interest on uninvested cash balances.

Cash App Borrow

In recent years, the platform has experimented with “Cash App Borrow,” a short-term lending feature that allows eligible users to take out small loans (typically up to $600). Users are charged a flat fee (usually 5%) to borrow the funds for a month. If they fail to pay it back within the grace period, additional interest is applied. This foray into micro-lending is highly lucrative, as the interest rates on these short-term loans can be significantly higher than traditional personal loans, reflecting the risk and convenience of the service.

The Strategic Flywheel: Why the Model Works

The brilliance of Cash App’s money-making strategy isn’t just in any single fee; it’s in the “ecosystem” or “flywheel” effect. Unlike traditional banks that spend hundreds of dollars in marketing to acquire a single customer (Customer Acquisition Cost or CAC), Cash App’s P2P nature allows it to grow virally. When a user wants to send money to a friend who doesn’t have the app, they invite them. This peer-led growth keeps CAC remarkably low.

By keeping the “entrance” to the app free and frictionless, Cash App builds a massive user base. Once users are inside, the app provides a buffet of optional, fee-based services that prioritize speed, ease of use, and accessibility. Whether it is an instant transfer to a bank, a 3% fee for using a credit card, or a spread on a Bitcoin trade, Cash App has successfully found a way to charge for the “seconds” and “cents” of the digital economy.

In conclusion, Cash App makes money by functioning as a high-velocity financial intermediary. By capturing fees from merchants, charging for instant liquidity, and facilitating the trade of digital assets, Block has created a resilient business model that thrives regardless of whether a user is looking to buy a cup of coffee, invest in a tech stock, or simply send money to a roommate for rent.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.