For millions of Americans, Social Security serves as the cornerstone of a comprehensive retirement strategy. It is often described as a “safety net,” but from a strictly financial perspective, it is a sophisticated, inflation-protected annuity backed by the federal government. To effectively plan for the future, one must move beyond the vague notion of “getting a check” and understand the specific metrics, mathematical formulas, and temporal factors that dictate exactly how much income one will receive.

Social Security is not a stagnant pool of money where you simply withdraw what you put in. Instead, it is a dynamic system based on your career-long earnings history, the timing of your claim, and the legislative framework governing the Social Security Administration (SSA). Understanding the pillars of this system allows for better integration of Social Security into a broader personal finance portfolio, including 401(k)s, IRAs, and brokerage accounts.

The Quantitative Foundation: Your Earnings History and Work Credits

The primary driver of your Social Security benefit is your lifetime earnings. However, the SSA does not simply look at your last few years of work or your highest-earning decade. The calculation is significantly more comprehensive and requires a specific threshold of participation in the labor force.

The 35-Year Average and Indexing

Social Security benefits are calculated based on your “Average Indexed Monthly Earnings” (AIME). To find this, the SSA looks at your entire work history and selects the 35 years in which you earned the most. A critical component here is “indexing.” Because $20,000 in 1985 had significantly more purchasing power than $20,000 today, the SSA uses the Average Wage Index (AWI) to adjust your historical earnings to reflect current economic conditions.

If you have fewer than 35 years of covered employment, the SSA does not shorten the denominator; they still divide by 35 years. This means they will factor in “zeros” for the missing years, which can drastically pull down your average. From a financial planning perspective, working just a few more years—even part-time—to replace those zeros can result in a permanent increase in your monthly benefit.

The Credits System (Quarters of Coverage)

Before you are even eligible to receive a benefit, you must earn enough “credits.” As of the current regulations, most workers need 40 credits to qualify for retirement benefits. You can earn up to four credits per year. The dollar amount required to earn one credit changes annually based on inflation. For most professionals, this threshold is met within ten years of full-time employment. While earning more than 40 credits doesn’t increase your benefit, failing to reach this number means you may not be eligible for Social Security at all, highlighting the importance of tracking your “Social Security Statement” throughout your career.

The Mathematical Engine: AIME to PIA and the Role of Bend Points

Once your 35-year indexed average is established, the SSA applies a formula to determine your Primary Insurance Amount (PIA). This is the base amount you would receive if you retired exactly at your Full Retirement Age (FRA). The formula is intentionally “progressive,” meaning it replaces a higher percentage of income for lower-earners than for higher-earners.

Understanding the “Bend Points”

The transition from your Average Indexed Monthly Earnings (AIME) to your actual benefit (PIA) is governed by “bend points.” These are specific dollar thresholds that dictate the “replacement rate” of your income. For example, the formula might take 90% of your first $1,174 of monthly earnings, 32% of earnings between $1,174 and $7,078, and only 15% of earnings above that second threshold (numbers adjust annually).

This structure is vital for personal finance planning. High-income earners often find that Social Security replaces only about 25–30% of their pre-retirement income, whereas lower-income earners might see a replacement rate of 50% or more. This discrepancy highlights why high-earning professionals must rely more heavily on private investments and employer-sponsored plans to maintain their lifestyle in retirement.

The Contribution and Benefit Base (The Cap)

It is also important to note that Social Security is based on earnings up to a certain limit, known as the “Taxable Maximum.” If you earn above this cap (e.g., $168,600 in 2024), you stop paying Social Security taxes for that year, and those excess earnings do not count toward your future benefit calculation. Understanding this cap is essential for tax planning and for realizing that there is a “ceiling” on how much Social Security can actually provide, regardless of how high your salary becomes.

The Temporal Factor: How Claiming Age Alters Your Financial Outcome

Perhaps the most significant variable in the Social Security equation is when you choose to start receiving benefits. While your earnings history sets the “base,” your age at the time of filing acts as a multiplier—or a divider—on that base amount.

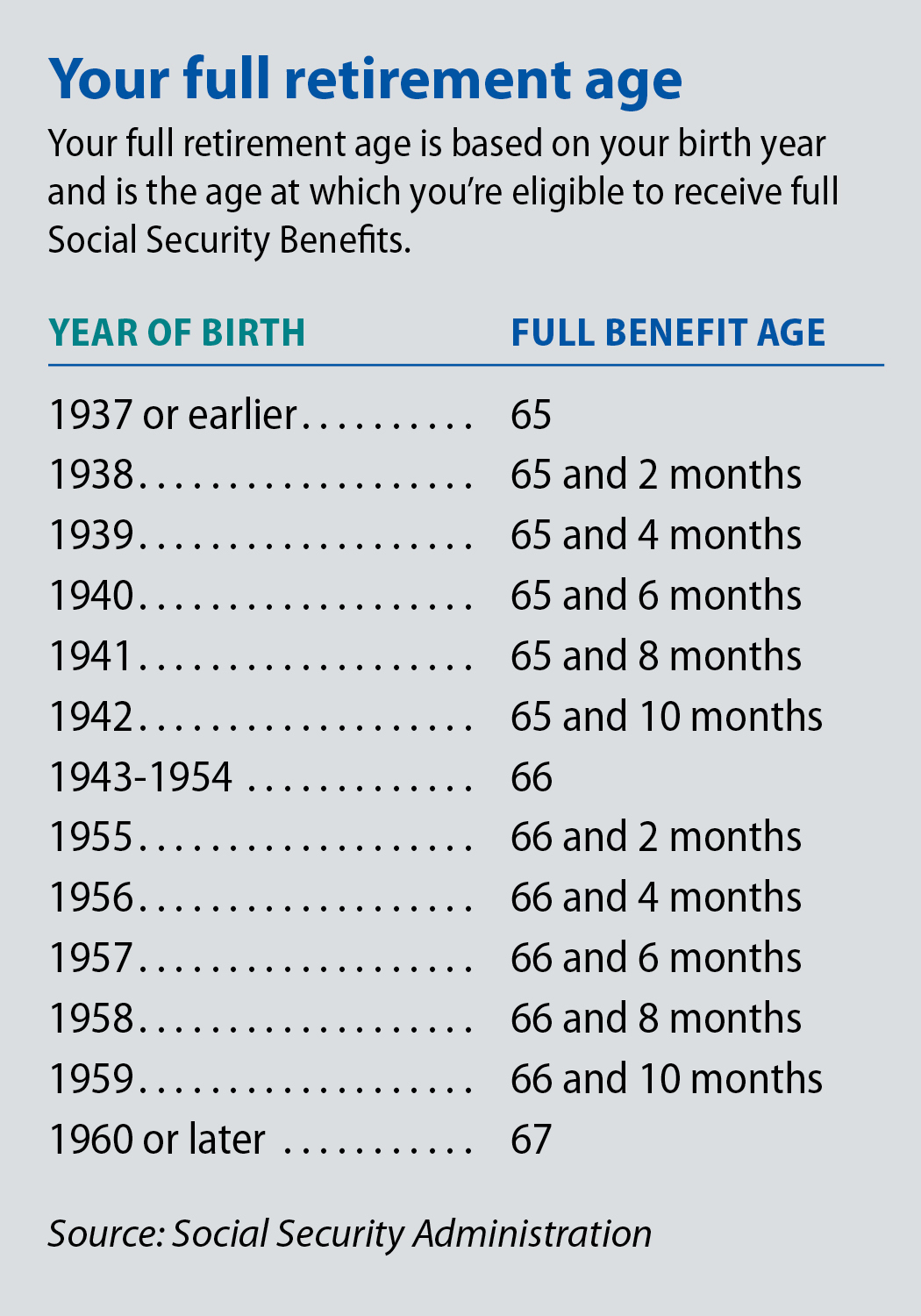

Full Retirement Age (FRA) vs. Early Filing

For those born in 1960 or later, the Full Retirement Age is 67. If you claim at this age, you receive 100% of your calculated PIA. However, the system allows you to claim as early as age 62. The trade-off is a permanent reduction in your monthly check. Filing at 62 results in a benefit reduction of roughly 30% compared to filing at 67. From a cash-flow perspective, early filing is often a necessity for those in poor health or facing unemployment, but for those with the means to wait, it represents a significant loss in lifetime “guaranteed” income.

The Power of Delayed Retirement Credits

Conversely, for every year you delay claiming Social Security beyond your FRA (up until age 70), your benefit increases by approximately 8% per year in “Delayed Retirement Credits.” This is a guaranteed, non-compounding return that is nearly impossible to match in the private market with the same level of risk.

By waiting until age 70, a retiree can receive 124% of their PIA. In the context of a holistic financial plan, “spending down” a portion of your IRA or 401(k) between the ages of 67 and 70 to allow your Social Security benefit to grow can be a mathematically superior strategy. This effectively “purchases” a larger, inflation-adjusted, government-backed annuity for the remainder of your life.

External Influences: Inflation, Taxation, and Family Dynamics

Social Security is not an isolated financial asset; it interacts with the broader economy and your specific family situation. The amount you actually see in your bank account is influenced by the cost of living and the IRS.

Cost-of-Living Adjustments (COLA)

One of the most valuable features of Social Security is the annual Cost-of-Living Adjustment (COLA). Unlike most private pensions or fixed annuities, Social Security benefits are adjusted based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). In years of high inflation, this adjustment ensures that the purchasing power of your benefit does not erode. For retirees, this serves as a critical hedge against the rising costs of healthcare and daily living expenses.

The Impact of Taxes and the “Tax Torpedo”

A common surprise for many retirees is that Social Security benefits can be taxable. If your “combined income” (adjusted gross income + tax-exempt interest + half of your Social Security benefits) exceeds certain thresholds, up to 85% of your benefits may be subject to federal income tax. This creates what financial planners call the “Tax Torpedo,” where an extra dollar of IRA withdrawal can trigger taxes on Social Security benefits, effectively creating a very high marginal tax rate. Strategic withdrawals from Roth accounts or managing capital gains can help mitigate this.

Spousal and Survivor Benefits

Social Security is also based on your marital history. A spouse may be eligible for a benefit equal to up to 50% of the worker’s PIA, even if the spouse never worked outside the home. Furthermore, survivor benefits allow a widow or widower to inherit the higher of the two spouses’ benefits. This makes “claiming strategy” a couple’s decision. Often, it makes sense for the higher-earning spouse to delay benefits as long as possible to ensure the highest possible survivor benefit for the remaining spouse.

Strategic Integration: Managing Social Security as an Asset

When we ask “what is Social Security based on,” we eventually realize it is based on a lifetime of financial decisions. It is not just a government handout; it is a complex financial instrument that requires active management.

Monitoring the Social Security Statement

The most proactive step any worker can take is to regularly review their Social Security Statement via the “my Social Security” portal. This document provides estimates for your benefits at ages 62, FRA, and 70. More importantly, it allows you to verify that your earnings have been recorded correctly. An error in your reported income from twenty years ago could result in a lower benefit for the rest of your life if left uncorrected.

Longevity Risk and the “Break-Even” Analysis

Ultimately, Social Security is a hedge against “longevity risk”—the risk of outliving your money. When deciding when to claim, many people perform a “break-even analysis” to see at what age the total value of waiting until 70 surpasses the total value of claiming at 62. Usually, the break-even point is in the late 70s or early 80s. If you expect to live past that point, waiting is the mathematically sound choice.

By understanding that Social Security is based on a 35-year earnings average, a progressive formula involving bend points, and a strict timeline of claiming ages, you can transform it from a mystery into a manageable component of your financial freedom. It is the only part of your portfolio that offers a lifetime guarantee, inflation protection, and survivor benefits all in one package—making it perhaps the most important “money” topic any individual will ever master.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.