Understanding how to compute the inflation rate is more than just an academic exercise in economics; it is a fundamental skill for any savvy investor, business owner, or individual looking to preserve their purchasing power. Inflation is the silent thief of the financial world, gradually eroding the value of the currency in your pocket. When you understand the mechanics behind how inflation is measured, you gain the clarity needed to make informed decisions about your savings, investments, and long-term financial planning.

In this comprehensive guide, we will break down the mathematical formulas used by economists, explore the different metrics that track price changes, and discuss how you can calculate your own personal inflation rate to better manage your household budget.

Foundations of Inflation: Why Computing the Rate Matters

Before diving into the numbers, it is essential to understand what we are actually measuring. Inflation represents the rate at which the general level of prices for goods and services is rising. As inflation climbs, every dollar you own buys a smaller percentage of a good or service. For anyone in the “Money” niche, ignoring inflation is a recipe for financial stagnation.

Defining Inflation and Its Economic Impact

Inflation is not necessarily a sign of a failing economy; in fact, most central banks, such as the Federal Reserve in the United States, aim for a target inflation rate of around 2%. This low, predictable increase encourages consumers to spend rather than hoard cash, which keeps the economy moving. However, when inflation outpaces wage growth or interest rates on savings, it creates a “real” loss in wealth. Computing the inflation rate allows you to determine your “real” rate of return on investments—the amount you actually earn after accounting for the rising cost of living.

The Role of the Consumer Price Index (CPI)

The most common tool used to compute inflation is the Consumer Price Index (CPI). The CPI tracks the weighted average of prices of a “basket” of consumer goods and services, such as transportation, food, and medical care. Government agencies, like the Bureau of Labor Statistics (BLS), survey thousands of households and retail establishments to see how prices change over time. When we talk about “the inflation rate,” we are usually talking about the percentage change in the CPI from one period to the next.

The Step-by-Step Formula for Calculating Inflation

Calculating inflation is a straightforward mathematical process once you have the right data points. Whether you are looking at national statistics or your own business expenses, the formula remains the same. It is essentially a “percentage change” formula applied to price indices.

Identifying the Base Year and Current Year Prices

To begin your calculation, you need two distinct data points: the price (or index value) at the beginning of the period (the Base Year) and the price at the end of the period (the Current Year).

- Base Year Index (B): This is the starting point. If you are using the CPI, you would look up the index value for the month or year you wish to start from.

- Current Year Index (C): This is the most recent data point.

Applying the Mathematical Formula

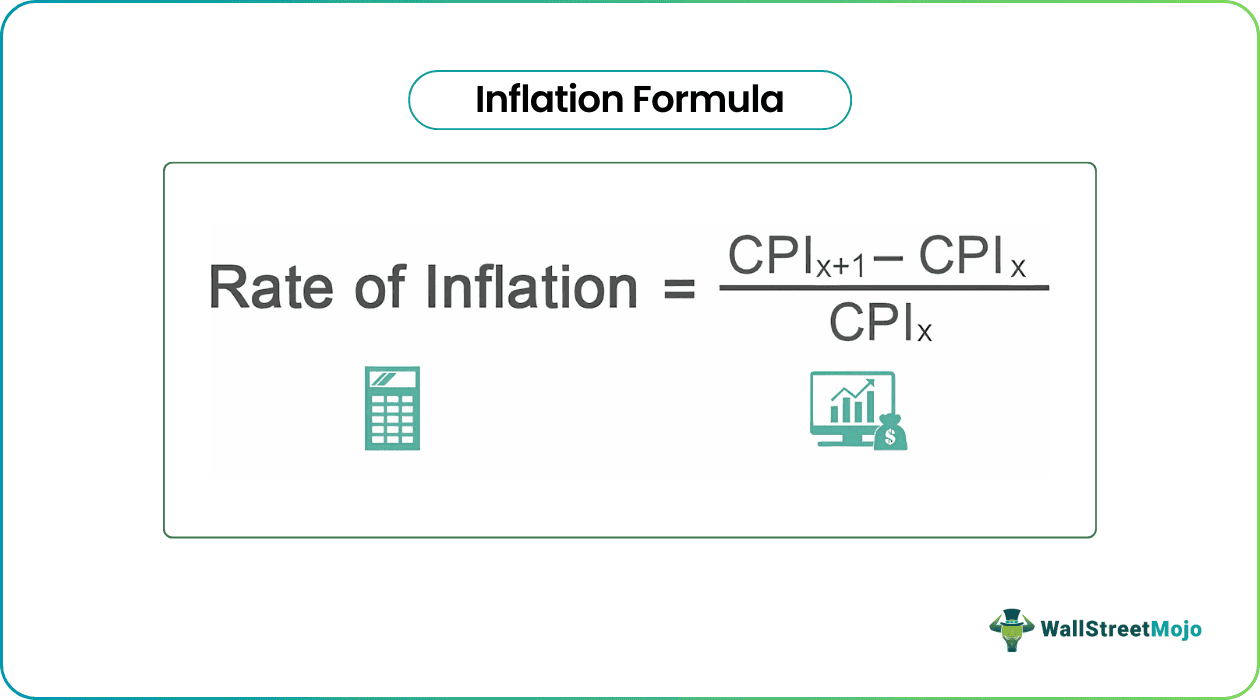

The standard formula for computing the inflation rate is:

Inflation Rate = ((CPI in Current Year – CPI in Base Year) / CPI in Base Year) x 100

By subtracting the old price from the new price, you find the total “increase.” By dividing that increase by the original price, you find the ratio of growth. Multiplying by 100 converts that ratio into a percentage, which is the “Inflation Rate.”

Real-World Example: A Practical Walkthrough

Let’s look at a hypothetical example to ground the theory. Suppose the CPI for a basket of goods was 250 in January of last year. This year, for the same month, the CPI has risen to 265.

- Subtract: 265 – 250 = 15

- Divide: 15 / 250 = 0.06

- Multiply: 0.06 x 100 = 6%

In this scenario, the annual inflation rate is 6%. This means that, on average, you would need $1.06 today to buy what $1.00 bought you just one year ago. For a business, this might mean increasing prices by at least 6% just to maintain the same profit margins.

Beyond the Basics: Different Types of Inflation Metrics

While the CPI is the most publicized figure, it is not the only way to compute inflation. Different metrics serve different purposes in the world of finance and investment. Understanding these variations helps you interpret economic news more accurately.

Core Inflation vs. Headline Inflation

When you hear news reports about inflation, you will often hear the term “Core Inflation.”

- Headline Inflation: This is the raw CPI figure that includes everything, including food and energy prices.

- Core Inflation: This metric strips away food and energy prices because they tend to be highly volatile and subject to temporary shocks (like a bad harvest or a geopolitical conflict affecting oil).

Investors often prefer looking at Core Inflation because it provides a clearer picture of long-term price trends without the “noise” of temporary price swings.

The Producer Price Index (PPI) and Wholesale Perspectives

While the CPI measures what consumers pay, the Producer Price Index (PPI) measures the change in prices received by domestic producers for their output. In the “Money” niche, the PPI is considered a “leading indicator.” If the PPI is rising, it means it is becoming more expensive for companies to manufacture goods. Eventually, those companies will pass those costs on to consumers, leading to a rise in the CPI a few months down the road. Keeping an eye on the PPI can give you a head start on adjusting your investment portfolio before the general public reacts to CPI data.

Personal Inflation: Calculating Your Own Cost of Living

The national CPI is an average, but your personal spending habits might differ significantly from the “average” consumer. If you own your home outright, you aren’t affected by rising rents. If you don’t drive, gas price spikes don’t hit your wallet.

To compute your personal inflation rate, track your total expenses for a month and compare them to the same month the previous year (ensuring the “lifestyle” or the “basket” remains the same).

Personal Inflation = ((This Year’s Expenses – Last Year’s Expenses) / Last Year’s Expenses) x 100.

Knowing this number is vital for accurate budgeting and determining how much you need to save for retirement.

Financial Implications: How Inflation Calculations Shape Your Money Strategy

Why do we go through the trouble of computing these rates? In the realm of personal finance and business, these numbers dictate strategy. If you don’t account for inflation, you are essentially flying blind.

Adjusting Investment Returns for Real Growth

One of the most dangerous mistakes an investor can make is looking only at “Nominal Returns.” If your stock portfolio grew by 8% last year, that sounds great. However, if the inflation rate was 9%, your “Real Return” was actually -1%. You have less purchasing power than you started with, despite having more dollars.

To find your real return, use the Fisher Equation:

Real Interest Rate ≈ Nominal Interest Rate – Inflation Rate.

Always compute the inflation rate before celebrating a gain in your brokerage account.

Wage Negotiations and Cost-of-Living Adjustments (COLA)

For employees and freelancers, computing the inflation rate is a powerful tool for income negotiation. If you receive a 3% raise but inflation is 5%, you have actually received a pay cut in terms of what that money can buy. Many corporate contracts and Social Security benefits include a Cost-of-Living Adjustment (COLA), which automatically increases payments based on the CPI. Understanding how these are computed ensures you are being compensated fairly for your labor.

Protecting Your Portfolio with Inflation-Hedged Assets

Once you know the inflation rate is trending upward, you can shift your financial strategy toward assets that traditionally perform well during inflationary periods.

- TIPS (Treasury Inflation-Protected Securities): These are government bonds where the principal increases with inflation (measured by the CPI).

- Real Estate: Property values and rents often rise along with inflation, acting as a natural hedge.

- Commodities: Gold, oil, and agricultural products often see price increases when the value of the dollar falls.

- Equities: Companies with “pricing power”—the ability to raise prices without losing customers—can maintain profitability even when inflation is high.

Conclusion

Computing the inflation rate is a vital skill for anyone serious about mastering their money. By mastering the formula—subtracting the old index from the new, dividing by the old, and multiplying by 100—you gain a clear-eyed view of economic reality. Whether you are looking at the broad CPI, the producer-focused PPI, or your own personal spending, these numbers provide the data necessary to protect your wealth.

In an era of economic fluctuation, being able to calculate the “real” value of your assets ensures that you aren’t just working for money, but that your money is working effectively for you. Stay vigilant, track the indices, and always adjust your financial sails to the prevailing winds of inflation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.