For millions of Americans, Social Security represents a cornerstone of their financial future, a vital safety net in retirement, disability, or for survivors. Yet, despite its widespread impact, the exact mechanics of how one’s individual benefit is calculated remain a mystery to many. The question, “How much is my Social Security?” is far more complex than a simple glance at a pay stub, involving a lifetime of earnings, claiming decisions, and economic factors.

Understanding your potential Social Security benefit is not just about satisfying curiosity; it’s a critical step in comprehensive retirement planning. It empowers you to make informed decisions about when to retire, how much to save, and how to allocate other investments. This article aims to demystify the calculation process, guide you through accessing your personalized benefit estimates, and provide insights into strategies for maximizing this crucial component of your financial security.

Understanding the Pillars of Social Security Benefits

Social Security is a comprehensive program designed to provide financial protection to American workers and their families. While often associated with retirement, it encompasses a broader range of benefits that address various life circumstances. Knowing these foundational elements is the first step toward understanding your specific entitlement.

Types of Social Security Benefits

The Social Security Administration (SSA) administers several primary types of benefits, each with distinct eligibility criteria and payment structures:

- Retirement Benefits: This is the most widely known benefit, providing monthly income to eligible individuals who have reached a certain age and accumulated sufficient work credits. The amount you receive depends heavily on your earnings history and the age at which you choose to start collecting benefits.

- Disability Benefits: If you become unable to work due to a severe physical or mental condition, Social Security Disability Insurance (SSDI) can provide income. Eligibility requires meeting the SSA’s strict definition of disability and having enough work credits, similar to retirement benefits, but focused on recent work history.

- Survivors Benefits: In the unfortunate event of a worker’s death, certain family members—including spouses, children, and dependent parents—may be eligible for monthly benefits. These benefits offer crucial financial support during a difficult time, based on the deceased worker’s earnings record.

- Supplemental Security Income (SSI): While often confused with Social Security, SSI is a separate, needs-based program that provides financial assistance to aged, blind, or disabled people who have little or no income. Unlike Social Security benefits, SSI is not based on your work history or contributions.

For the purpose of answering “How much is my Social Security,” our focus will primarily remain on retirement benefits, as this is what most people are referring to when they pose this question.

Eligibility Requirements: Earning Work Credits

To qualify for Social Security retirement benefits, you must accumulate “work credits.” These credits are earned through your employment, with one credit awarded for a specific amount of earnings each year. The amount needed to earn a single credit changes annually, but the principle remains the same.

- How Credits are Earned: You can earn up to four work credits each year. For most of your working life, earning the maximum four credits is quite achievable through regular employment.

- Minimum Credits Required: Generally, you need to accumulate 40 work credits to be eligible for retirement benefits. This translates to roughly 10 years of covered work, as long as you earned at least the minimum amount each year to get four credits. If you stop working before earning 40 credits, you may not qualify for retirement benefits unless you later return to work and earn the remaining credits.

- Disability and Survivors Benefits: The number of work credits required for disability or survivors benefits can vary depending on your age at the time of disability or death, often requiring fewer credits for younger individuals.

Understanding your work credit status is foundational. If you have any doubt about your eligibility, the SSA’s online portal is the best place to check your current work credit count.

Factors Influencing Your Benefit Amount

Once you’ve established your eligibility, the next critical step is understanding what determines the actual dollar amount you’ll receive. This isn’t a fixed sum; it’s a highly personalized calculation influenced by several key variables that span your entire working life and beyond.

Your Earnings Record: A Lifetime of Contributions

The most significant factor in determining your Social Security retirement benefit is your lifetime earnings record. The SSA uses a complex formula to calculate your “primary insurance amount” (PIA), which is the benefit you would receive if you claim at your full retirement age.

- The 35 Highest-Earning Years: The SSA doesn’t just look at your last few years of work. Instead, it considers your 35 highest-earning years, adjusted for inflation (indexed), up to the Social Security taxable earnings limit for each year. If you have fewer than 35 years of earnings, the missing years will be counted as zeros, which can significantly reduce your benefit. This highlights the importance of working consistently for at least 35 years.

- Average Indexed Monthly Earnings (AIME): Your earnings from those 35 highest-earning years are totaled, indexed to reflect changes in general wage levels over time, and then divided by 420 (35 years x 12 months) to arrive at your AIME. This AIME is then used in a tiered formula to calculate your PIA. The formula is progressive, meaning it replaces a higher percentage of earnings for lower-income workers than for higher-income workers.

Your Age When You Claim: The Crucial Decision

The age at which you choose to begin receiving your Social Security benefits is perhaps the single most impactful decision you’ll make regarding the monthly amount. There’s a wide window for claiming, each with its own financial implications.

- Full Retirement Age (FRA): This is the age at which you are entitled to 100% of your Primary Insurance Amount (PIA). Your FRA depends on your birth year. For those born between 1943 and 1954, it’s 66. It gradually increases for later birth years, reaching 67 for anyone born in 1960 or later.

- Claiming Early (as early as age 62): You can start receiving benefits as early as age 62, but doing so results in a permanent reduction of your monthly payment. The reduction is significant: approximately 6.67% for each of the first three years before your FRA, and another 5% for each year prior to that. For someone with an FRA of 67, claiming at 62 means a benefit reduction of up to 30%.

- Delaying Benefits (up to age 70): Conversely, if you delay claiming benefits past your FRA, you can earn “delayed retirement credits.” These credits permanently increase your monthly benefit by 8% for each year you delay, up to age 70. There is no additional benefit to waiting past age 70. For someone with an FRA of 67, waiting until 70 can result in a benefit that is 124% of their PIA (3 years x 8% = 24% increase).

This decision involves a careful balance of financial need, health status, and other retirement income sources.

Cost-of-Living Adjustments (COLAs) and Future Projections

Once you begin receiving Social Security benefits, your payments are not static. They are subject to annual Cost-of-Living Adjustments (COLAs), which are designed to help maintain the purchasing power of your benefits as inflation erodes the value of money over time.

- How COLAs Work: COLAs are determined by changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If the CPI-W increases, your benefits will generally increase by a corresponding percentage, usually announced in October for the following year.

- Impact on Future Planning: While COLAs help, they don’t always perfectly match individual inflation experiences, and they can sometimes be zero in periods of low inflation. It’s important to factor in these potential adjustments, or lack thereof, when projecting your long-term retirement income.

Spousal, Survivor, and Dependent Benefits

While the core question is about your Social Security, it’s crucial to remember that Social Security is a family benefit program. Your benefit amount can be indirectly influenced by (or augmented by) benefits available to your spouse, ex-spouse, children, or as a survivor.

- Spousal Benefits: A spouse may be eligible for benefits based on their working spouse’s record, even if they never worked themselves or have a lower benefit from their own record. This benefit can be up to 50% of the primary worker’s PIA.

- Survivors Benefits: If you are a surviving spouse, child, or even a dependent parent of a deceased worker, you may be eligible for benefits based on that worker’s record.

- Divorced Spousal Benefits: Even after divorce, you may be eligible for benefits on your ex-spouse’s record if certain conditions are met (e.g., marriage lasted 10+ years, you are currently unmarried, and are age 62 or older).

These family benefits can significantly impact the overall financial security of a household and should be considered when evaluating your total Social Security picture.

How to Find Your Estimated Benefit Amount

Given the myriad factors involved, you might wonder how to get a concrete estimate tailored to your unique situation. Fortunately, the Social Security Administration provides excellent resources to help you do just that.

The Social Security Statement: Your Personalized Report

The Social Security Statement is arguably the most valuable tool for understanding your benefits. This personalized report provides a wealth of information specific to your earnings and work history.

- What it Contains: Your statement details your complete earnings record, year by year, as reported to the SSA. It also provides estimates of your future benefits at different claiming ages (e.g., age 62, your full retirement age, and age 70), as well as estimates for disability and survivors benefits. It also indicates how many work credits you’ve accumulated.

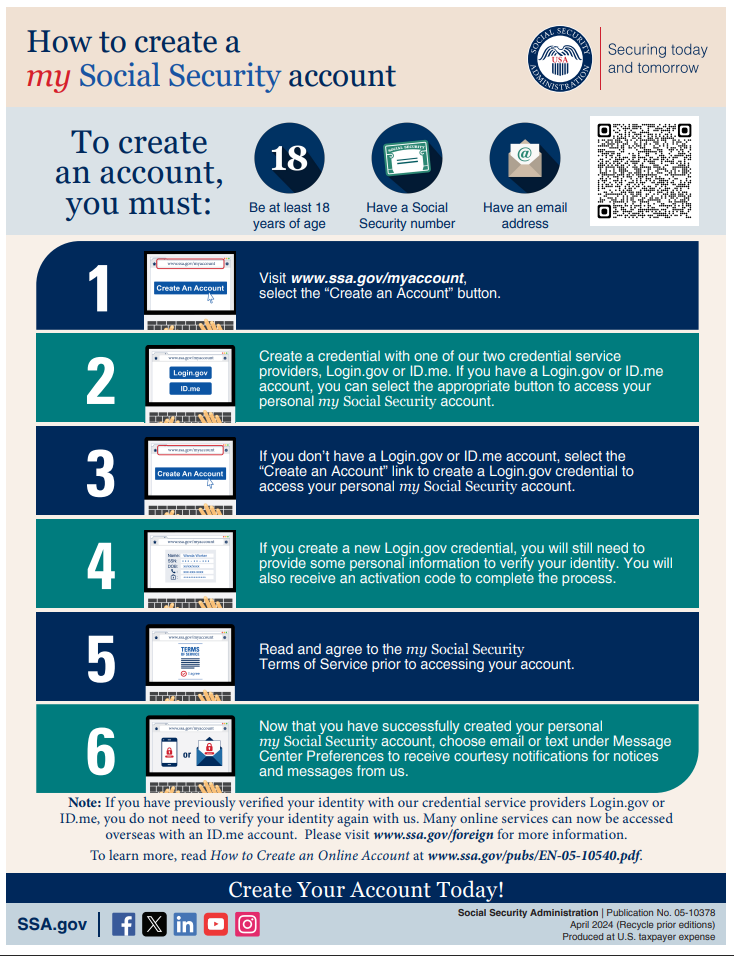

- How to Access It: The easiest and most reliable way to get your statement is by creating an account on the SSA’s official website: www.ssa.gov/myaccount. Once registered, you can view, download, or print your statement at any time. The SSA primarily relies on online access now but still mails paper statements to those approaching retirement age who haven’t registered online.

- Reviewing for Accuracy: It is critical to review your earnings record on the statement for accuracy. Mistakes can happen, and unreported or misreported earnings could reduce your future benefits. If you find an error, contact the SSA to correct it.

Online Tools: The SSA’s Benefit Estimator

Beyond your personalized statement, the SSA website also hosts several interactive online tools that allow you to explore different claiming scenarios.

- Retirement Estimator: This tool is incredibly useful for modeling various “what if” scenarios. You can input different retirement dates, future earnings projections, or even adjust your planned claiming age, and the estimator will instantly show you how these changes would impact your monthly benefit. This helps in strategic planning.

- Other Calculators: The SSA website offers other calculators, such as a life expectancy calculator, which can provide additional context for your claiming decisions.

These tools are invaluable for personalizing your benefit projections and understanding the financial consequences of different choices.

Consulting with the Social Security Administration

While online tools and your statement provide substantial information, sometimes you might have complex questions or need personalized guidance.

- Calling the SSA: You can call the SSA’s toll-free number (1-800-772-1213) to speak with a representative. They can answer questions about your record, eligibility, and the application process.

- Visiting a Local Office: For more complex situations or if you prefer in-person assistance, you can visit a local Social Security office. It’s often advisable to call ahead to schedule an appointment, as wait times can be significant.

- Professional Financial Advice: For integrating Social Security into a broader retirement strategy, consider consulting a qualified financial advisor. They can help you factor Social Security benefits into your overall financial plan, taking into account investments, taxes, and other income sources.

Maximizing Your Social Security Benefits

Understanding your potential benefits is one thing; strategizing to get the most out of the system is another. There are several key approaches you can take to potentially increase your Social Security income.

The Power of Delayed Claiming

As discussed, delaying your claim past your Full Retirement Age (FRA) can significantly boost your monthly benefit. This is one of the most powerful strategies available to most individuals.

- The 8% Annual Increase: For every year you delay claiming benefits past your FRA, up to age 70, your monthly payment increases by 8%. This is a guaranteed, inflation-adjusted return that is hard to beat in most other investments, especially in a low-interest-rate environment.

- Long-Term Impact: While it requires delaying income, the higher monthly payment is permanent. Over a long retirement, this can amount to tens or even hundreds of thousands of dollars in additional lifetime benefits. This strategy is particularly advantageous for individuals who are in good health, have other retirement savings to live on in their early retirement years, or continue to work.

Working Longer and Earning More

Your Social Security benefit is based on your 35 highest-earning years. This means that working longer and earning more, especially later in your career, can have a surprisingly positive effect.

- Replacing Lower-Earning Years: If you continue to work past your previous 35-year mark, your current higher earnings can replace lower-earning years from earlier in your career (which may have been indexed lower or were simply less productive). This effectively raises your average indexed monthly earnings (AIME) and thus your Primary Insurance Amount (PIA).

- Beyond 35 Years: Even if you’ve already worked for 35 years, every additional year of higher earnings can potentially increase your benefit by bumping out a lower-earning year from your calculation.

Coordinating with Other Retirement Income

Social Security should be viewed as one component of a holistic retirement income strategy. Coordinating it with other assets can optimize your overall financial picture.

- Bridging the Gap: If you plan to delay Social Security benefits, you’ll need a “bridge” to cover your living expenses in the interim. This bridge might come from personal savings, investments (like 401(k)s or IRAs), or continuing to work part-time.

- Tax Efficiency: Understand how Social Security benefits are taxed in conjunction with other income. Strategically drawing down taxable accounts versus Roth accounts in different years can minimize your overall tax burden.

- Spousal Strategies: For married couples, coordinating claiming strategies can yield significant combined benefits. For example, one spouse might claim early while the other delays, or one might claim a spousal benefit while their own benefit grows.

Integrating Social Security into Your Retirement Plan

Understanding your Social Security benefits is not merely an academic exercise; it’s a fundamental step in crafting a robust retirement plan. It serves as a financial bedrock, but its role must be properly contextualized alongside other income streams and considerations.

Social Security as a Foundation, Not the Sole Pillar

It’s tempting to view Social Security as the entirety of your retirement income, but for most people, this is an insufficient approach. While essential, it’s designed to replace only a portion of your pre-retirement income.

- Partial Income Replacement: On average, Social Security replaces about 40% of an average worker’s pre-retirement earnings. This percentage is higher for lower-income earners and lower for higher-income earners. This means a significant portion of your retirement income will need to come from other sources, such as personal savings, employer-sponsored plans (401(k), 403(b)), individual retirement accounts (IRAs), pensions, or part-time work.

- Diversification is Key: Relying solely on Social Security can leave you vulnerable to potential future program changes or unexpected expenses. A diversified approach, integrating personal savings and investments, provides greater financial resilience and flexibility.

Planning for Taxes on Social Security Benefits

Many people are surprised to learn that their Social Security benefits can be subject to federal income tax, and in some states, to state income tax as well. This is a crucial consideration for retirement income planning.

- Provisional Income: The amount of your benefits subject to federal tax depends on your “provisional income,” which is generally calculated as your adjusted gross income (AGI) plus tax-exempt interest income, plus one-half of your Social Security benefits.

- Taxation Tiers:

- If your provisional income is between $25,000 and $34,000 (single) or $32,000 and $44,000 (married filing jointly), up to 50% of your benefits may be taxable.

- If your provisional income exceeds $34,000 (single) or $44,000 (married filing jointly), up to 85% of your benefits may be taxable.

- State Taxes: A handful of states also tax Social Security benefits, though most do not. It’s important to check the tax laws in your state of residence.

Strategic planning, such as balancing withdrawals from traditional IRAs/401(k)s with Roth accounts or other tax-efficient investments, can help manage your provisional income and potentially reduce the tax bite on your Social Security benefits.

Staying Informed: Future Changes and Reforms

Social Security is a dynamic program, and like any large government entitlement, it is subject to ongoing discussion, potential reforms, and legislative changes. While the core structure has remained remarkably stable, it’s prudent to stay informed.

- Long-Term Solvency: The Social Security trust funds face long-term solvency challenges, and projections indicate that without legislative action, the program may only be able to pay a reduced percentage of promised benefits in the future. Discussions about potential adjustments—such as increasing the full retirement age, modifying the COLA formula, adjusting the payroll tax rate, or increasing the taxable earnings limit—are ongoing.

- Impact on Planning: While it’s unwise to base your entire retirement plan on speculative changes, being aware of the broader context helps maintain flexibility in your planning. Continue to monitor official SSA announcements and reputable financial news sources for updates.

By understanding how your benefits are calculated, actively seeking out your personalized estimates, and proactively planning for their integration into your broader financial picture, you can approach retirement with greater confidence and clarity. Your Social Security benefit is a valuable asset, and knowing “how much is my Social Security” is the first step toward leveraging it effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.