Understanding exactly how much money lands in your bank account every month is the cornerstone of effective personal finance. While the question “how do I calculate my monthly salary?” might seem straightforward, the answer is often layered with complexities ranging from tax jurisdictions and benefit deductions to the nuances of pay cycles. For anyone looking to build a robust budget, plan for a major purchase, or negotiate a new job offer, mastering the math behind your paycheck is an essential skill.

In this guide, we will break down the components of your compensation, explore the mathematical formulas for different pay structures, and discuss how to use your monthly net income as a springboard for long-term financial stability.

Understanding the Fundamentals: Gross vs. Net Income

The first step in calculating your monthly salary is distinguishing between your gross income and your net income. Many people make the mistake of budgeting based on their gross salary, only to find themselves in a financial crunch when their actual take-home pay arrives.

The Definition of Gross Salary

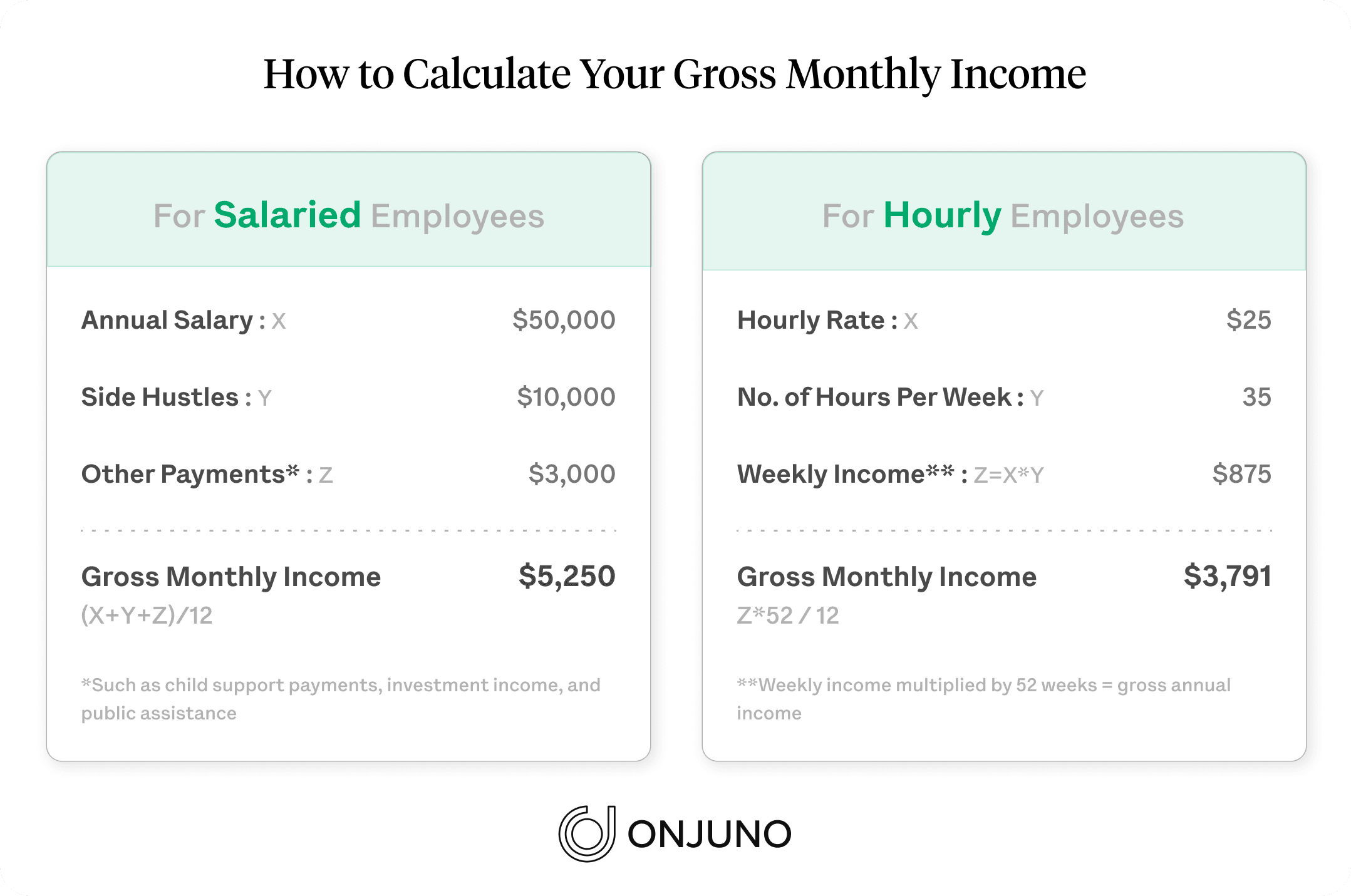

Gross salary is the total amount of money an employer pays you before any taxes or deductions are removed. If you are offered a job with a “salary of $60,000 per year,” that $60,000 is your gross annual income. While this figure is the benchmark for your earning power and is used by lenders to determine loan eligibility, it is not the amount of money you actually have available to spend. Gross income includes your base pay plus any bonuses, commissions, or overtime earned during that period.

Identifying Common Deductions

The “gap” between your gross and net income is comprised of several types of deductions. Understanding these is vital for an accurate calculation:

- Mandatory Taxes: This includes federal, state, and local income taxes, as well as contributions to social insurance programs (such as Social Security and Medicare in the United States).

- Pre-Tax Deductions: These are highly beneficial as they lower your taxable income. Examples include contributions to a 401(k) or 403(b) retirement plan, Health Savings Accounts (HSA), and flexible spending accounts (FSA).

- Post-Tax Deductions: These are taken out after taxes have been calculated. Examples might include certain life insurance premiums or union dues.

- Health and Wellness Benefits: Your portion of health, dental, and vision insurance premiums is typically deducted directly from your gross pay.

The Reality of Net Income (Take-Home Pay)

Net income is the “bottom line”—the actual amount deposited into your checking account. This is the figure you must use for your monthly budgeting. To calculate this accurately, you must subtract all the aforementioned deductions from your monthly gross pay.

Step-by-Step Calculation Methods for Different Pay Structures

Not everyone is paid on a simple annual salary. Depending on whether you are an hourly worker, a salaried professional, or a freelancer, the method for determining your monthly income will vary.

Converting Annual Salary to Monthly

If you are a salaried employee with a fixed annual rate, the calculation is the most direct, but there is a catch regarding pay cycles.

- The Simple Method: Divide your gross annual salary by 12. For a $72,000 annual salary, the gross monthly pay is $6,000.

- The Net Method: To find the net monthly salary, you must apply your effective tax rate. If your total deductions (taxes + benefits) account for 25% of your pay, you would multiply your gross monthly pay by 0.75. ($6,000 x 0.75 = $4,500 net).

Calculating Monthly Income for Hourly Workers

Hourly calculations require a bit more legwork because months do not have an equal number of days.

- The Standard Work Week: If you work 40 hours a week at $25 per hour, your weekly gross is $1,000.

- The 4.33 Rule: Finance professionals often use the multiplier of 4.33 to represent the average number of weeks in a month (52 weeks divided by 12 months). Using this, your average monthly gross would be $1,000 x 4.33 = $4,330.

- Actual Hours Worked: For precise monthly tracking, you should sum your actual hours worked during that specific calendar month, as some months contain five pay periods if you are paid weekly.

Factoring in Bi-Weekly and Weekly Pay Cycles

The frequency of your paycheck significantly impacts your monthly cash flow.

- Bi-Weekly (Every two weeks): There are 26 pay periods in a year. This means that in two months of the year, you will receive three paychecks instead of two. When calculating your “standard” monthly salary, it is often wisest to base your budget on two paychecks and treat the “extra” checks as a bonus for savings or debt repayment.

- Semi-Monthly (Twice a month): There are 24 pay periods, usually on the 1st and 15th. This is the easiest for monthly budgeting as your income is perfectly divided into two equal halves every month.

Advanced Considerations: Bonuses, Overtime, and Commissions

For many professionals, a “base salary” is only one part of the equation. Variable income can make monthly calculations fluctuate, requiring a more sophisticated approach to financial management.

Managing Variable Income and Commissions

If a significant portion of your pay comes from sales commissions or performance bonuses, calculating a monthly average is safer than relying on peak months.

- The Conservative Estimate: Look at your lowest-earning month over the last year. Use this “floor” to cover your essential expenses (rent, utilities, groceries).

- The Rolling Average: Calculate the average of your last six months of income. This provides a realistic middle ground for lifestyle planning.

The Impact of Overtime on Your Take-Home Pay

Overtime pay (usually 1.5 times your hourly rate) can provide a significant boost. However, it is also subject to higher “withholding.” It is a common misconception that overtime moves you into a higher tax bracket for your entire income; rather, only the additional dollars earned are taxed at the higher marginal rate. When calculating your monthly salary, it is best to treat overtime as “supplemental” income rather than “guaranteed” income to avoid lifestyle creep.

Accounting for Annual and Quarterly Bonuses

Bonuses are often taxed at a flat supplemental rate (which can be higher than your standard withholding). When these arrive, they should be calculated separately from your standard monthly salary. From a personal finance perspective, these are best utilized for “one-off” financial goals like funding an IRA, paying off a car loan, or building a home down payment.

Strategic Financial Planning Based on Your Monthly Net Pay

Once you have arrived at an accurate figure for your monthly net salary, the real work of wealth building begins. Knowing the number is only useful if you apply it to a strategic framework.

Creating a Realistic Budget: The 50/30/20 Rule

A popular and effective way to allocate your monthly salary is the 50/30/20 rule:

- 50% for Needs: Half of your net monthly salary should cover essentials like housing, insurance, utilities, and basic groceries.

- 30% for Wants: This portion goes toward lifestyle choices, such as dining out, subscriptions, and hobbies.

- 20% for Financial Goals: The final fifth of your income should be aggressively directed toward debt repayment, emergency funds, and long-term investments.

Emergency Funds and Debt Repayment Strategies

Your monthly salary calculation dictates the size of your “safety net.” Most financial experts recommend an emergency fund of three to six months of essential expenses. If your calculation shows that your monthly “needs” total $3,000, your goal should be an emergency fund between $9,000 and $18,000. Additionally, knowing your exact monthly surplus allows you to choose between the “Debt Snowball” (paying off smallest balances first) or the “Debt Avalanche” (paying off highest interest rates first) with precision.

Leveraging Automation for Financial Growth

The most successful earners don’t just calculate their salary; they automate it. Once you know your monthly net pay, set up automatic transfers that trigger on payday. This ensures that your “20%” for savings and investments is moved before you have the chance to spend it on “wants.”

Conclusion: The Power of Financial Literacy

Calculating your monthly salary is more than a simple math exercise; it is an act of taking control over your financial destiny. By understanding the journey your money takes from “gross” to “net,” you demystify your paystub and eliminate the anxiety of “where did my money go?”

Whether you are navigating the complexities of an hourly wage with fluctuating overtime or managing a steady executive salary with quarterly bonuses, the principles remain the same: calculate accurately, account for taxes, and allocate intentionally. When you master the calculation of your monthly income, you gain the clarity needed to make informed decisions that lead to lasting financial freedom and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.