In the realm of personal finance and wealth management, few concepts are as transformative as compound interest. Often referred to as the “eighth wonder of the world,” compound interest is the engine that drives long-term investment growth and capital accumulation. Unlike simple interest, which is calculated solely on the principal amount, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods.

Understanding the mathematical foundation of this concept is not merely an academic exercise; it is a fundamental requirement for anyone looking to achieve financial independence, plan for retirement, or optimize their business’s cash flow. By mastering the formula for compound interest, investors can move beyond guesswork and begin to make data-driven decisions about their financial futures.

Decoding the Compound Interest Formula: A Mathematical Breakdown

To harness the power of compounding, one must first understand the variables that dictate its trajectory. The standard formula for calculating the future value of an investment with compound interest is:

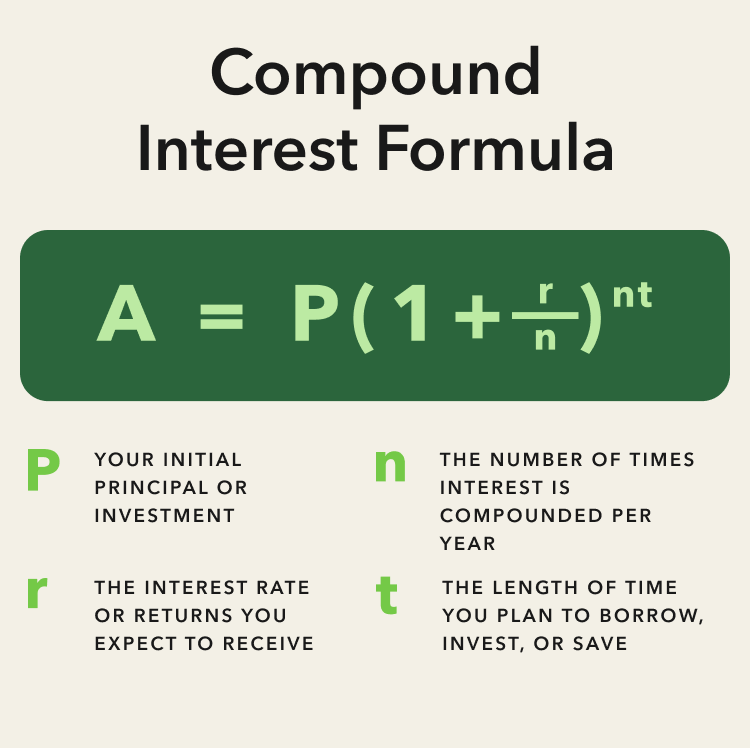

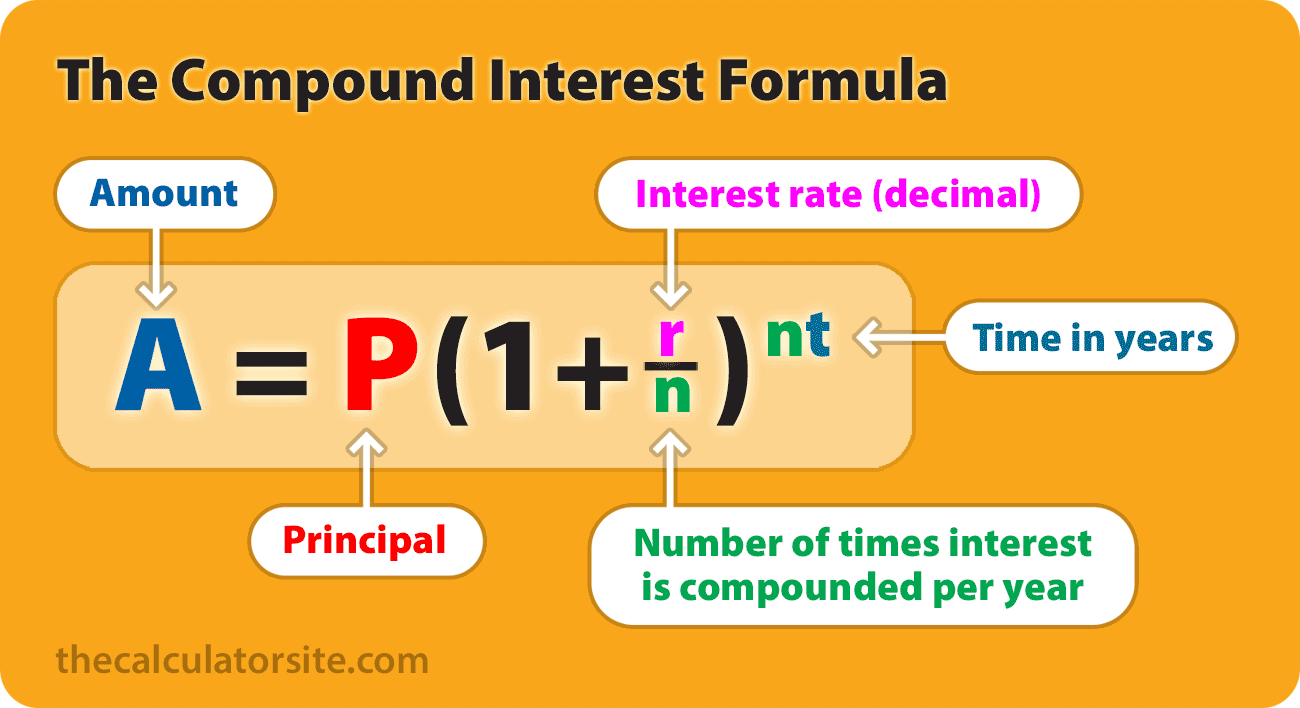

A = P(1 + r/n)^(nt)

At first glance, the equation may seem daunting to those without a background in finance, but when broken down into its constituent parts, it reveals a logical flow of how money grows over time.

Identifying the Variables

To use the formula effectively, you must define five key components:

- A (Future Value): This represents the final amount of money you will have after the interest has been applied over the specified time period.

- P (Principal): This is the initial sum of money you invest or borrow. It is the baseline upon which all future growth is built.

- r (Annual Interest Rate): This is the nominal annual interest rate, expressed as a decimal. For example, an interest rate of 5% would be written as 0.05.

- n (Compounding Frequency): This denotes how many times the interest is compounded per year. Common frequencies include annually (n=1), semi-annually (n=2), quarterly (n=4), monthly (n=12), or daily (n=365).

- t (Time): This is the number of years the money is invested or borrowed for.

Simple vs. Compound Interest: What Sets Them Apart?

To appreciate the compound interest formula, it is helpful to contrast it with simple interest. The formula for simple interest is I = P × r × t. In this scenario, your earnings remain linear. If you invest $10,000 at a 5% simple interest rate, you will earn $500 every single year. After 20 years, you will have your original $10,000 plus $10,000 in interest ($500 × 20), totaling $20,000.

However, using the compound interest formula (compounded annually), that same $10,000 at 5% grows exponentially. In the first year, you earn $500. In the second year, you earn 5% of $10,500 ($525). By the 20th year, your total balance would be approximately $26,532. The “interest on interest” creates a curve that steepens over time, rewarding the disciplined investor far more than a linear model ever could.

The Mechanics of Frequency: How Compounding Intervals Shape Wealth

One of the most critical variables in the compound interest formula is n—the frequency of compounding. While the interest rate (r) and time (t) are often the focus of financial discussions, the frequency at which interest is calculated and added back to the principal can significantly alter the final outcome.

Daily, Monthly, and Annual Compounding

The more frequently interest is compounded, the higher the effective annual yield. This is because interest begins earning its own interest sooner. Let’s look at how the value of $10,000 changes over 10 years at a 7% interest rate with different compounding frequencies:

- Annual Compounding (n=1): The interest is calculated once a year. After 10 years, the total is $19,671.51.

- Monthly Compounding (n=12): The interest is calculated every month. After 10 years, the total is $20,096.61.

- Daily Compounding (n=365): The interest is calculated every day. After 10 years, the total is $20,136.18.

While the jump from monthly to daily compounding may seem marginal in the short term, over decades and with larger sums of money, these differences represent thousands of dollars in “found” wealth. In the world of business finance, understanding these nuances is essential when comparing different savings accounts, Certificates of Deposit (CDs), or bond yields.

The “Magic” of Reinvestment

The formula assumes that the interest earned is reinvested back into the account. If an investor withdraws the interest as it is earned, the compounding process is “broken,” and the investment reverts to a simple interest model. For compound interest to work its “magic,” the investor must maintain a hands-off approach, allowing the mathematical cycle of growth to remain uninterrupted. This is why dividend reinvestment plans (DRIPs) are so popular in equity investing; they automate the compounding process by using stock dividends to purchase more shares, which in turn produce more dividends.

Strategic Applications in Personal Finance and Investing

The formula for compound interest is more than just a calculation; it is a roadmap for wealth creation. By manipulating the variables within the formula, individuals can design strategies that maximize their long-term financial health.

Retirement Planning and the Cost of Delay

The most influential variable in the compound interest formula is arguably t (time). Because the growth is exponential, the final years of an investment period see the most dramatic increases in value. This highlights the “cost of delay.”

Consider two investors: Investor A starts saving $500 a month at age 25. Investor B starts saving the same $500 a month but waits until age 35. Assuming a 7% annual return compounded monthly, by age 65, Investor A will have approximately $1.3 million. Investor B, despite starting only 10 years later, will have approximately $600,000. By delaying for a decade, Investor B loses out on more than half of the potential wealth. This underscores a vital rule in money management: time in the market is often more important than timing the market.

Leveraging the Rule of 72 for Quick Projections

While the standard formula is precise, it can be difficult to calculate mentally. Financial professionals often use the “Rule of 72” as a shortcut to estimate how long it will take for an investment to double at a fixed annual rate of interest.

The Rule of 72 is simple: Divide 72 by the annual interest rate.

- At a 6% return, your money doubles in 12 years (72 / 6 = 12).

- At an 8% return, your money doubles in 9 years (72 / 8 = 9).

- At a 12% return, your money doubles in just 6 years (72 / 12 = 6).

This mental model allows investors to quickly gauge the impact of different interest rates on their portfolios without needing a financial calculator. It serves as a stark reminder that even a 1% or 2% difference in fees or returns can have a massive impact on the velocity of wealth accumulation.

Compound Interest in Modern Business and Debt Management

While we often discuss compound interest in the context of building assets, it is equally important to understand how it functions on the liability side of the balance sheet. In business and personal finance, compound interest is a double-edged sword that can either build a fortune or create an inescapable cycle of debt.

The Double-Edged Sword of Credit Card Debt

For many consumers, the compound interest formula works against them. Credit cards are notorious for using daily compounding on outstanding balances. When you carry a balance at a 20% interest rate, the “r/n” part of our formula (0.20 / 365) is applied every single day.

Because the compounding frequency is so high and the interest rate is aggressive, the debt can grow at a pace that far outstrips the borrower’s ability to pay it down. Understanding the formula reveals why making only the “minimum payment” is a financial trap; the payment often barely covers the interest accrued during that period, leaving the principal virtually untouched and allowing the compounding cycle to continue indefinitely.

Corporate Finance and Yield-on-Cost

In the corporate world, compound interest principles are applied to capital budgeting and “yield-on-cost” metrics. When a company reinvests its profits into research and development or expanding its operations, it is essentially seeking a compound return on its retained earnings.

Sophisticated investors look for companies that can consistently generate a high Return on Equity (ROE). If a company can earn 15% on its capital and reinvest those earnings at the same rate, the value of the company compounds internally. For the shareholder, this results in capital appreciation that mirrors the compound interest formula, even if the company doesn’t pay a direct dividend.

Conclusion: Mastering the Math of Wealth

The formula for compound interest—A = P(1 + r/n)^(nt)—is the most powerful tool in a financier’s arsenal. It teaches us that wealth is not merely a product of how much we earn, but a product of how much we keep, the rate at which we grow it, and the time we allow it to mature.

To succeed in the “Money” niche, one must respect the variables. Maximize your principal (P) by living below your means; maximize your rate of return (r) through education and diversified investing; maximize your frequency (n) by choosing the right financial instruments; and, most importantly, maximize your time (t) by starting as early as possible. By aligning your financial habits with the mathematical reality of compound interest, you turn the passage of time into your greatest economic ally.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.