The question “When will the stock market crash?” is perhaps the most frequent query posed to financial advisors, economists, and search engines alike. It is born out of a mixture of primal fear and calculated caution. For the seasoned investor, a crash represents a potential threat to decades of wealth accumulation; for the novice, it feels like an impending disaster that could wipe out their entry-level capital. However, to understand when a market might decline, one must first look past the headlines and delve into the mechanics of market cycles, economic indicators, and the psychological forces that drive price action.

Predicting the exact date of a market crash is a fool’s errand. Even the most prestigious Wall Street analysts rarely get the timing right. Yet, while we cannot predict the “when,” we can certainly analyze the “how” and “why.” By identifying the structural vulnerabilities in the financial system and maintaining a disciplined investment strategy, individuals can move from a state of anxiety to a state of readiness.

Decoding the Anatomy of a Market Crash

A stock market crash is generally defined as a rapid and often unexpected drop in stock prices. While a “correction” is a decline of 10% from recent highs, a “crash” is typically more severe, often exceeding a 20% drop within a very short timeframe. Understanding the anatomy of these events requires looking at fundamental valuation metrics and macroeconomic pressures.

Valuation Metrics and the Shiller P/E Ratio

One of the most cited indicators of a market being “overextended” is the Cyclically Adjusted Price-to-Earnings (CAPE) ratio, also known as the Shiller P/E. Developed by Nobel laureate Robert Shiller, this metric looks at real per-share earnings over a 10-year period to smooth out fluctuations in corporate profits. When the Shiller P/E is significantly higher than its historical average, it suggests that stocks are expensive relative to their earnings potential. While high valuations do not cause a crash directly, they create a “fragile” environment where even a small piece of bad news can trigger a massive sell-off.

Economic Indicators: Inflation and Interest Rates

Interest rates are the gravity of the financial world. When the Federal Reserve or other central banks raise interest rates to combat inflation, the cost of borrowing increases for both consumers and corporations. High interest rates often lead to reduced corporate spending, lower consumer demand, and a higher discount rate applied to future earnings—which drags down stock prices. Historically, many market crashes have been preceded by a period of aggressive “quantitative tightening” where the liquidity that fueled the bull market is suddenly withdrawn.

The Role of Investor Sentiment and “Irrational Exuberance”

Markets are driven by human emotion as much as they are by math. “Irrational exuberance,” a term popularized during the dot-com bubble, describes a state where investors ignore traditional valuation metrics in favor of FOMO (Fear Of Missing Out). When the “shoeshine boy” is giving stock tips, as the old adage goes, the market may be reaching a speculative peak. When sentiment reaches an extreme level of optimism, the pool of “marginal buyers” (new people left to buy stocks) dries up, leaving the market vulnerable to a reversal.

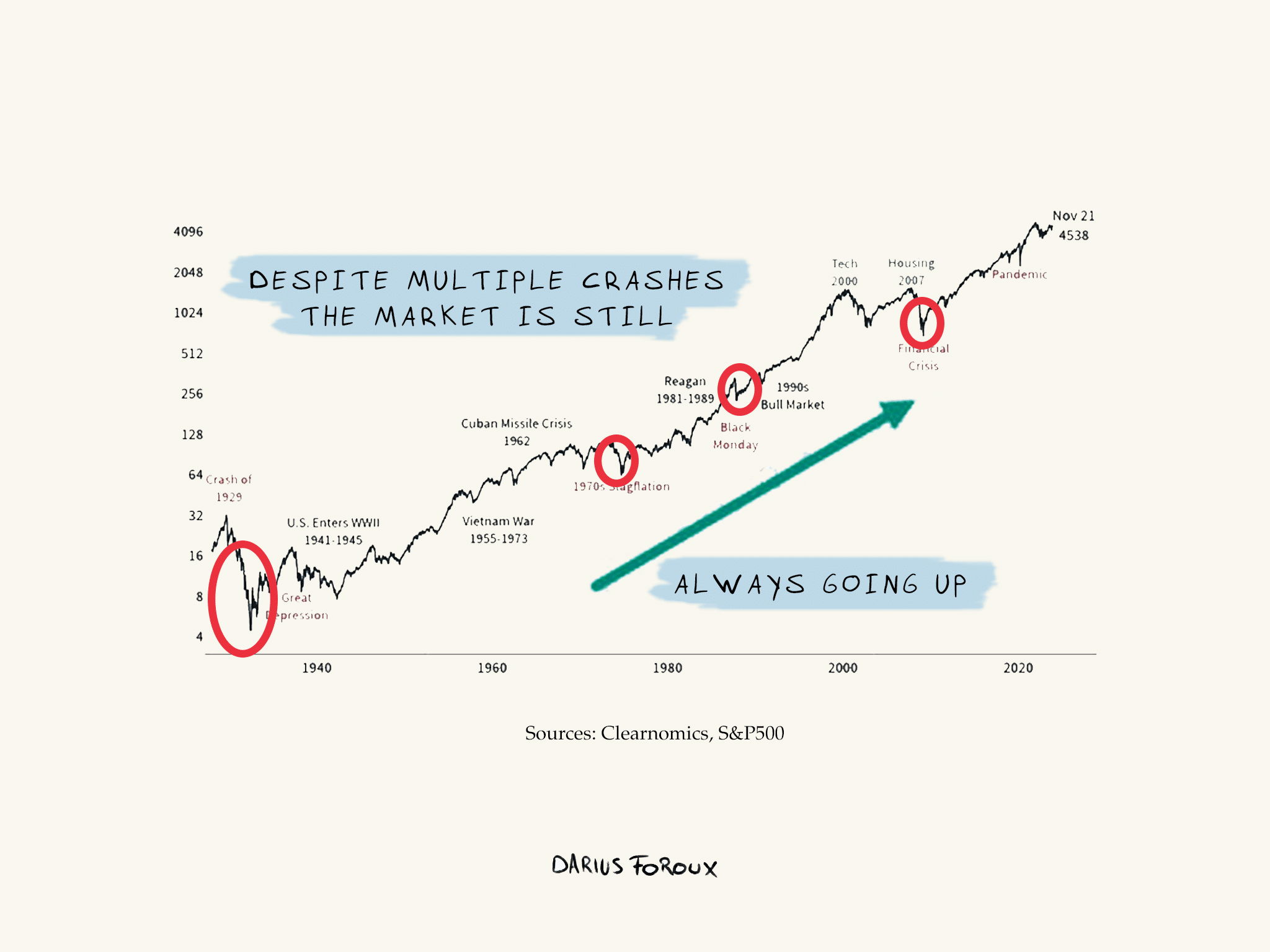

Historical Precedents and What They Teach Us

To understand future crashes, we must study the ghosts of markets past. While history does not repeat itself exactly, it often rhymes. Each major market downturn in the last century has provided invaluable lessons on the dangers of leverage, speculation, and systemic fragility.

The Dot-Com Bubble and Tech Overvaluation

The crash of 2000-2002 was a classic example of a valuation bubble. Investors poured money into internet-based companies that had no clear path to profitability, driven by the belief that the “New Economy” had rendered traditional physics of finance obsolete. When the reality of earnings finally set in, the Nasdaq plummeted, losing nearly 76% of its value from its peak. The lesson here was clear: eventually, cash flow matters more than clicks.

The 2008 Financial Crisis and Systemic Risk

The Great Recession was triggered not just by high stock prices, but by systemic rot in the housing and credit markets. The proliferation of subprime mortgages and complex derivatives created a house of cards that collapsed when housing prices turned downward. This crash taught investors about “contagion”—the idea that a problem in one sector (real estate) can rapidly paralyze the entire global financial system through interconnected banking networks.

The 2020 Flash Crash and Black Swan Events

The COVID-19 crash of March 2020 was a “Black Swan”—an unpredictable event with extreme consequences. It was the fastest 30% drop in history. However, it was also one of the fastest recoveries, fueled by unprecedented government stimulus. This event highlighted that not all crashes are caused by economic mismanagement; some are external shocks. It also proved that the modern market, driven by high-frequency trading and algorithms, can move with a speed that defies human reaction times.

Current Market Warning Signs and Resilience Factors

As we look at the contemporary financial landscape, there are several “red flags” that analysts watch closely, alongside “green flags” that suggest the market may be more resilient than we think.

Concentration Risk in “The Magnificent Seven”

A significant portion of the recent gains in the S&P 500 has been driven by a handful of mega-cap tech stocks, often referred to as “The Magnificent Seven” (including Apple, Microsoft, and Nvidia). While these companies are highly profitable, such high concentration means that if one or two of these giants stumble due to regulatory issues or earnings misses, the entire index could suffer a disproportionate blow. Diversification at the index level is lower than it has been in decades.

Geopolitical Tensions and Supply Chain Stability

We live in an era of de-globalization. Conflict in Eastern Europe, tensions in the Middle East, and trade friction between the U.S. and China all pose risks to the “just-in-time” supply chains that have kept inflation low for years. A sudden geopolitical escalation could lead to an energy price spike, which acts as a tax on the global economy and can act as a catalyst for a market downturn.

The Impact of Artificial Intelligence on Productivity

On the bullish side, the integration of Artificial Intelligence (AI) represents a potential productivity boom that could justify higher stock valuations. If AI allows corporations to operate with significantly higher margins and lower costs, the “expensive” stocks of today might actually be “cheap” relative to future earnings. This technological tailwind is currently the primary force pushing back against the gravity of high interest rates.

Strategic Asset Allocation: Weathering the Storm

Since we cannot know when the crash will happen, the only logical response is to build a “weather-proof” portfolio. Asset allocation is the most important tool in an investor’s arsenal for managing the risk of a market crash.

The Importance of Diversification Across Asset Classes

True diversification goes beyond owning different stocks. It involves owning different types of assets that do not move in perfect correlation. This includes bonds, which often (though not always) rise when stocks fall, as well as “hard assets” like real estate or commodities. By spreading risk across various categories, an investor ensures that a crash in the equity market does not result in a total loss of net worth.

Defensive Stocks vs. Growth Stocks

During a market downturn, not all stocks behave the same way. “Growth” stocks—those of companies expected to grow at a fast rate—usually get hit the hardest because their value is based on earnings far in the future. In contrast, “Defensive” stocks—such as utilities, healthcare, and consumer staples—tend to be more resilient. People still need to pay their electricity bills and buy groceries regardless of what the stock market is doing.

Holding Cash and High-Yield Liquid Assets

In a bull market, cash is often seen as a “drag” on returns. However, in a crash, cash is king. Maintaining a “dry powder” fund—cash held in high-yield savings accounts or money market funds—serves two purposes. First, it provides a psychological safety net, ensuring you don’t have to sell stocks at a loss to cover living expenses. Second, it provides the capital necessary to buy stocks when they are “on sale” during the depths of a crash.

The Psychological Blueprint for Long-Term Success

The greatest enemy of the investor during a market crash is not the market itself, but the person in the mirror. Behavioral finance shows that humans are hardwired to feel the pain of a loss twice as intensely as the joy of a gain.

Avoiding the Pitfalls of Panic Selling

Panic selling is the process of liquidating assets after they have already dropped in price, effectively “locking in” the losses. Historically, the best days in the stock market often occur within weeks of the worst days. If an investor panics and exits the market during a crash, they almost always miss the subsequent rebound, which is where the majority of long-term wealth is actually generated.

Dollar-Cost Averaging as a Volatility Shield

One of the most effective ways to combat the fear of a crash is Dollar-Cost Averaging (DCA). By investing a fixed amount of money at regular intervals, regardless of the price, you naturally buy more shares when prices are low and fewer shares when prices are high. This removes the need to “time the market” and turns market volatility into a mathematical advantage.

Why “Time in the Market” Beats “Timing the Market”

Data consistently shows that the longer your investment horizon, the lower the probability of losing money. For a one-day period, the stock market is essentially a coin flip. Over a 20-year period, the S&P 500 has historically never produced a negative return. A market crash is a terrifying event in the short term, but in the context of a 30-year investment journey, it is merely a blip on a chart that trends upward.

In conclusion, the stock market will eventually crash—it is an inevitable part of the capitalist cycle. It may be triggered by an interest rate hike, a geopolitical crisis, or a sudden shift in investor psychology. However, for the disciplined investor, the “when” is less important than the “how.” By focusing on sound valuations, maintaining a diversified portfolio, and mastering one’s own emotions, you can transform a market crash from a financial catastrophe into a generational opportunity for wealth creation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.