Writing a business plan is often viewed as a bureaucratic hurdle or a necessary evil to secure a bank loan. However, in the world of high-stakes finance and wealth creation, a business plan is far more than a document; it is a comprehensive financial roadmap. It is the architectural blueprint that dictates how capital will be deployed, how revenue will be generated, and how a venture will ultimately achieve solvency and profitability. For any entrepreneur looking to bridge the gap between a conceptual “side hustle” and a legitimate, scalable corporation, the ability to articulate a financial vision is paramount.

This guide explores the mechanics of constructing a business plan through the lens of business finance and investment. By focusing on fiscal discipline and market viability, you can transform an idea into a bankable asset.

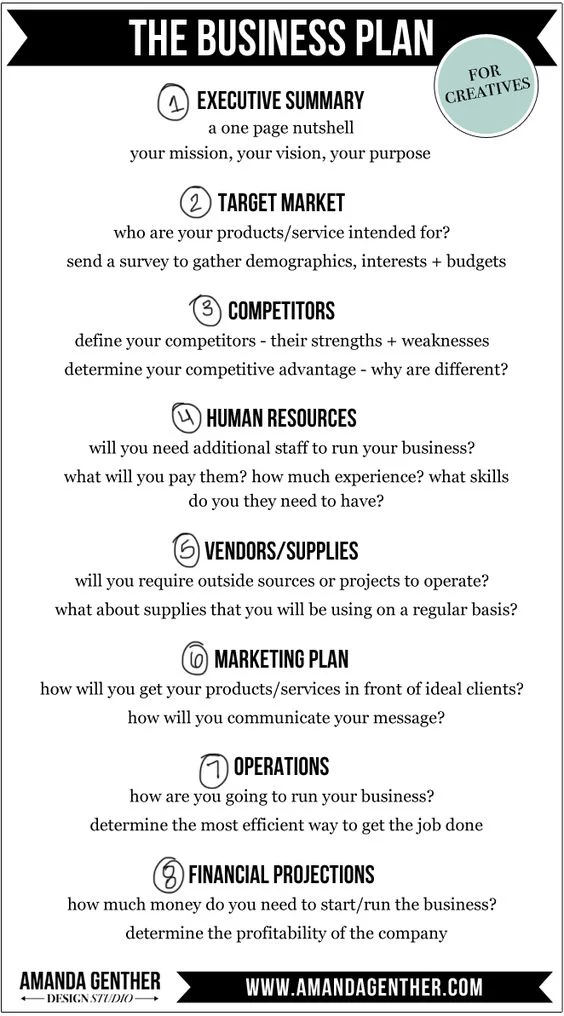

The Strategic Foundation: Defining Value and Fiscal Mission

Every successful financial venture begins with a clear articulation of its purpose and its path to profitability. In the “Money” niche, the executive summary and company description aren’t just introductory text; they are the “pitch” to your future self and potential investors.

Crafting a Compelling Executive Summary

The executive summary is arguably the most critical section of your business plan. It should provide a snapshot of your financial goals. If you are seeking investment, this section must highlight the “ask”—how much capital you need and what the projected Return on Investment (ROI) looks like. A well-constructed summary outlines the problem, the solution, and, most importantly, the economic opportunity.

The Value Proposition and Revenue Potential

Why will people pay for your product or service? From a business finance perspective, your value proposition must be linked to a gap in the market that represents a significant “Total Addressable Market” (TAM). You need to define whether your business is a high-volume, low-margin play or a low-volume, high-premium luxury model. This decision dictates your entire financial structure, from your marketing budget to your cost of goods sold (COGS).

Defining Business Milestones

Investors and financial planners look for “traction.” In your initial plan, set specific, time-bound financial milestones. These might include reaching a “break-even” point, securing your first $100,000 in revenue, or achieving a specific profit margin. These milestones act as fiscal guardrails, ensuring that the business remains focused on capital efficiency.

Market Analysis and the Mechanics of Revenue Generation

A business plan fails when it assumes customers will simply appear. A robust financial plan requires a deep dive into market dynamics, competitor pricing, and revenue modeling. Understanding the flow of money within your industry is the only way to ensure your business captures a share of it.

Quantitative Market Research

To build a credible financial forecast, you must quantify your market. This involves looking at industry trends, growth rates, and spending patterns. Are you entering a “Red Ocean” where price wars drive margins to zero, or a “Blue Ocean” where you can command premium pricing? Your financial projections depend entirely on these external economic factors.

Pricing Strategy and Margin Analysis

Pricing is where finance meets psychology. In this section of your plan, you must detail your pricing model. Will you use a subscription-based recurring revenue model, which offers high predictability and valuation? Or will you rely on one-time transactions? You must also account for your “Gross Margin”—the percentage of revenue that exceeds the cost of producing your product. A healthy margin is the lifeblood of any business, providing the cash flow necessary to reinvest in growth.

Customer Acquisition Cost (CAC) vs. Lifetime Value (LTV)

In modern business finance, the relationship between CAC and LTV is the ultimate indicator of success. Your business plan must estimate how much it will cost to “buy” a customer through marketing and sales efforts (CAC) and compare that to the total profit that customer will generate over time (LTV). If your LTV is not significantly higher than your CAC, the business is financially unsustainable in the long run.

Operational Structure and Capital Allocation

How you organize your business and allocate your resources determines your “burn rate”—the speed at which you spend your initial capital. A business plan must detail the operational costs required to keep the doors open and the wheels turning.

Management and Human Capital

In the eyes of an investor, the team is often more important than the idea. This section should outline the organizational structure and the cost of talent. Salaries, benefits, and payroll taxes represent a significant portion of business expenditure. Your plan should justify these costs by linking each role to a specific revenue-generating activity or operational efficiency.

Resource Allocation and Overhead

Operational excellence is about doing more with less. Your plan should detail your “Fixed Costs” (rent, utilities, software subscriptions) and your “Variable Costs” (materials, shipping, commissions). By identifying these early, you can perform a “Sensitivity Analysis” to see how a 10% increase in material costs or a 5% dip in sales would affect your bottom line.

Scalability and Infrastructure

A business that cannot scale is merely a job. To transition into the realm of true business finance, your plan must explain how the business will grow without a linear increase in costs. This might involve investing in automation, outsourcing non-core functions, or developing proprietary systems that increase output per dollar spent.

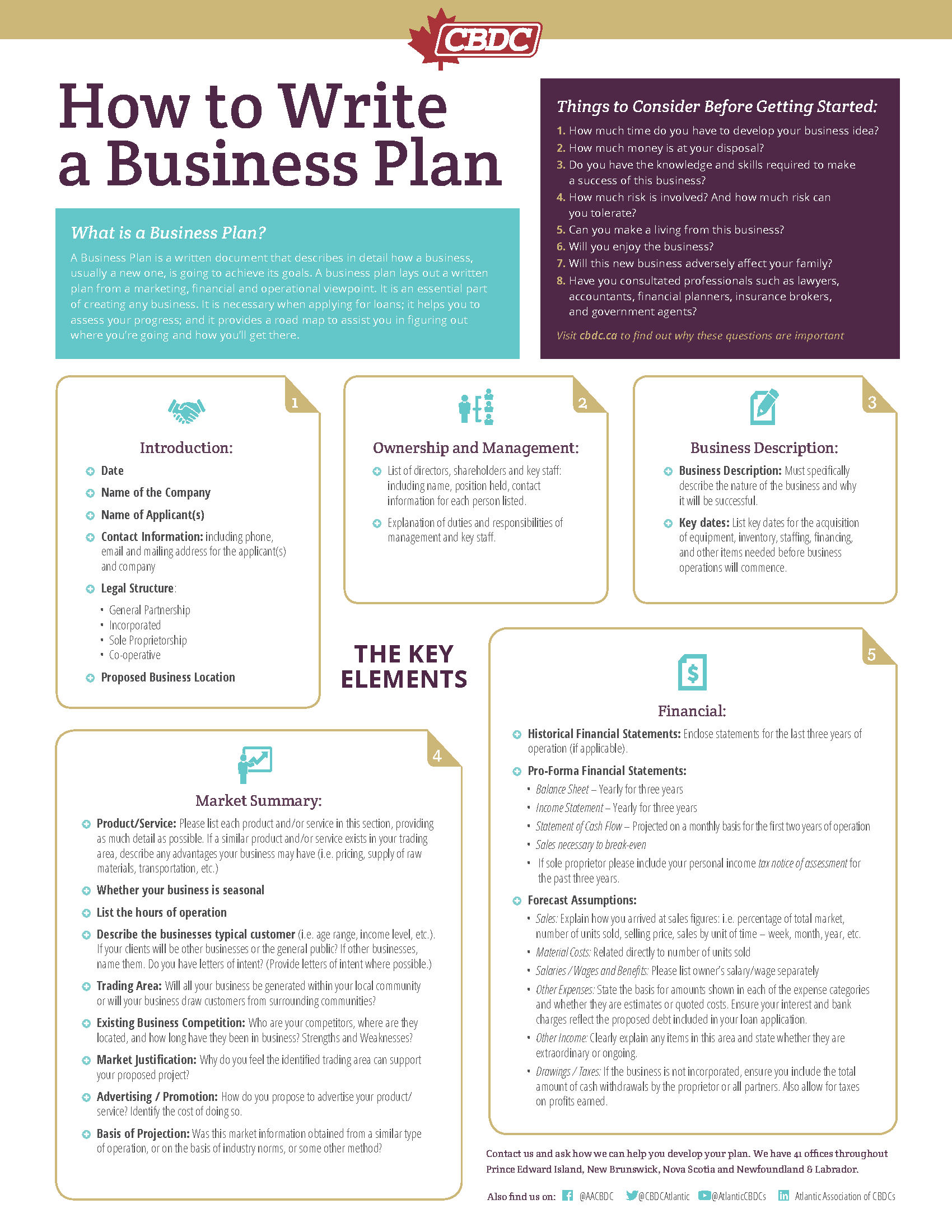

The Financial Plan: Projections, Cash Flow, and Funding

This is the core of the document for anyone focused on the “Money” aspect of entrepreneurship. It is the section where you move from theory to hard data. For a new business, these are “pro-forma” statements—educated estimates based on market research and logical assumptions.

The Three Pillars: Income Statement, Balance Sheet, and Cash Flow

A professional business plan must include these three financial statements:

- The Income Statement (P&L): This shows your projected revenue, expenses, and profit over a specific period (usually three to five years).

- The Balance Sheet: This provides a snapshot of your business’s financial health, listing assets (what you own), liabilities (what you owe), and equity.

- The Cash Flow Statement: This is the most vital document for a startup. It tracks the actual movement of cash. Many profitable businesses go bankrupt because their cash is tied up in inventory or unpaid invoices while their bills come due.

Break-Even Analysis

Every investor wants to know one thing: “When do I get my money back?” The break-even analysis calculates the exact point where your total revenue equals your total expenses. Reaching this point is the first major victory for any new business, as it signifies that the venture is self-sustaining and no longer requires external capital to survive.

Funding Requests and Exit Strategies

If the purpose of your business plan is to raise money, you must be explicit about your requirements. Are you seeking debt financing (loans) or equity financing (selling a piece of the company)? Detail exactly how the funds will be used—for example, 40% for product development, 40% for marketing, and 20% for working capital. Finally, outline an “Exit Strategy.” Whether it’s an Initial Public Offering (IPO), an acquisition by a larger firm, or a long-term dividend-paying entity, you must show how the capital will eventually be returned to the stakeholders with a profit.

Risk Management and Financial Contingency Planning

The final step in writing a high-level business plan is acknowledging that things rarely go according to plan. Professional financial planning involves identifying risks and creating “Plan B” scenarios to protect capital.

Identifying Financial Risks

What happens if a key supplier goes out of business? What if interest rates rise or a global recession hits? Your business plan should include a “Risk Assessment” that identifies these external threats. By demonstrating that you have considered these variables, you build credibility with lenders and partners.

Insurance and Asset Protection

Part of business finance is protecting what you have built. Detail the types of insurance you will carry (liability, property, key-man insurance) and the legal structure of your business (such as an LLC or Corporation) to protect your personal assets from business liabilities.

Long-term Fiscal Discipline

A business plan is not a static document; it is a living entity. Conclude your plan by establishing a system for regular financial reviews. This includes monthly “budget vs. actual” reporting and quarterly strategy pivots. In the world of money, those who monitor their data the closest are the ones most likely to thrive.

By following this structured approach, you transition from someone who merely has an “idea” to someone who possesses a rigorous financial strategy. Writing a business plan is the first investment you make in your own success—an investment of time and analytical rigor that pays dividends for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.