Tax season often brings a sense of trepidation, not just because of the complexity of filing, but because of the logistical hurdles involved in settling a balance with the Internal Revenue Service (IRS). In the contemporary financial era, the methods available for paying federal taxes have expanded significantly, moving far beyond the traditional paper check. Whether you are a solo entrepreneur managing quarterly estimates, a high-net-worth investor with capital gains obligations, or a salaried employee who didn’t withhold enough throughout the year, understanding your payment options is a critical component of personal finance management.

Effective financial planning requires not only knowing how much you owe but also how to deliver those funds securely, efficiently, and in a way that aligns with your cash flow strategy. This guide explores the diverse ecosystem of IRS payment methods, the strategic considerations of each, and what to do if you find yourself unable to pay your balance in full.

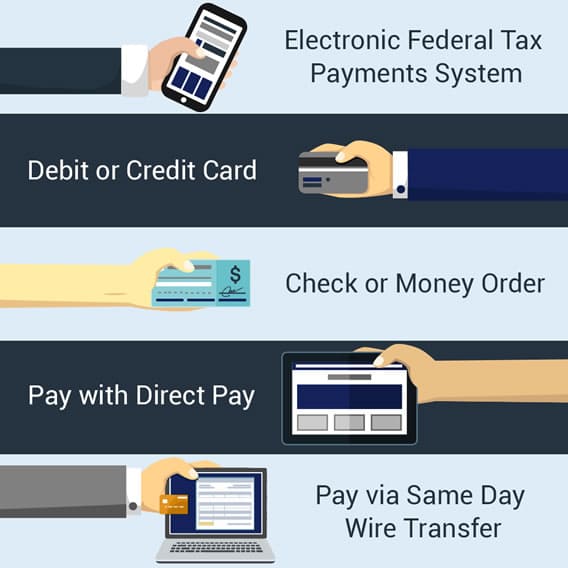

Digital-First Solutions: The Safest and Fastest Ways to Pay

In its push toward modernization, the IRS has prioritized digital payment platforms. These methods are generally preferred because they offer immediate confirmation, reduce the risk of mail theft, and integrate seamlessly with modern accounting software. For the tech-savvy taxpayer, these tools provide the highest level of transparency and control.

IRS Direct Pay: The Gold Standard for Individuals

For individual taxpayers, IRS Direct Pay is arguably the most efficient tool available. This service allows you to pay your income tax directly from your checking or savings account without any additional fees. It is designed specifically for individuals filing Form 1040, as well as those making estimated tax payments or paying for extensions.

The primary advantage of Direct Pay is its simplicity. You do not need to create an IRS account to use it, though you will need to verify your identity using information from a prior year’s tax return. Once verified, you can schedule payments up to 365 days in advance, providing a significant advantage for those who want to manage their cash flow by automating their tax obligations.

The Electronic Federal Tax Payment System (EFTPS)

While Direct Pay is excellent for individuals, the Electronic Federal Tax Payment System (EFTPS) is the heavy-duty alternative designed for businesses and high-frequency taxpayers. EFTPS is a free service provided by the U.S. Department of the Treasury that allows for the payment of all federal taxes, including corporate, employment, and excise taxes.

Unlike Direct Pay, EFTPS requires a formal enrollment process, which involves receiving a PIN via mail. While this adds a layer of initial friction, the system is exceptionally robust. It provides a detailed payment history for up to 16 months and allows for sophisticated scheduling. For business owners who must manage payroll taxes and diverse federal obligations, EFTPS is an essential financial tool that ensures compliance and provides an audit trail that paper checks simply cannot match.

Utilizing Digital Wallets and Mobile Apps

Recognizing the shift in consumer behavior, the IRS now accepts payments via digital wallets like PayPal and Click to Pay through their authorized third-party processors. Furthermore, the IRS2Go mobile app serves as a mobile gateway for making payments on the fly. This shift reflects a broader trend in personal finance where the boundaries between “official” government transactions and everyday consumer tech are blurring. Using a digital wallet can be particularly useful for those who maintain a balance in these accounts from side hustles or freelance work, allowing for a frictionless transfer of funds to the Treasury.

Traditional Payment Methods: Checks, Money Orders, and Cash

Despite the digital revolution, a significant portion of the population still relies on traditional payment methods. Whether due to a lack of high-speed internet access, a preference for physical records, or specific liquidity constraints, the IRS continues to support “analog” options. However, these methods require a higher level of diligence to ensure the payment is credited correctly.

Paying by Mail: Ensuring Your Check Reaches the IRS

If you choose to pay by mail, you must send a check or money order made out to the “U.S. Treasury.” It is a common mistake to make the check payable to the “IRS,” and while usually processed, using the correct terminology ensures fewer delays.

Crucially, every mailed payment should include a Form 1040-V (Payment Voucher). This small slip of paper contains the essential data—your Social Security Number, the tax year, and the type of tax—that tells the IRS computer system exactly where to apply the funds. Without it, your check may sit in a processing center for weeks, potentially triggering erroneous late-notices. To safeguard your finances, always send tax payments via Certified Mail with a Return Receipt Requested. This provides legal proof of “timely mailing,” which the IRS treats as “timely filing.”

In-Person Cash Payments: Utilizing Retail Partners

It may come as a surprise that you can pay the IRS with cash, but you cannot do so by walking into a local IRS office with a suitcase of bills. Instead, the IRS has partnered with retail chains like 7-Eleven, CVS, and Walgreens through services like ACI Payments, Inc. and Pay1040.

This method is vital for the “unbanked” or “underbanked” population—individuals who do not have traditional bank accounts. To use this service, taxpayers must first initiate the process online to receive a payment code, then take that code to a participating retail location. There are daily limits (usually around $1,000) and small convenience fees involved. From a financial management perspective, this is often a method of last resort due to the fees and the physical security risks of carrying large amounts of cash.

Credit and Debit Card Payments: Understanding the Costs

For some, paying a large tax bill with a credit card is an attractive option, either to bridge a short-term liquidity gap or to harvest credit card rewards points. However, the IRS does not process card payments directly; they use third-party service providers who charge “convenience fees.”

Authorized Third-Party Processors

The IRS currently uses three main processors: ACI Payments, Inc., EveryTaxPayment.com, and Link2Gov. These processors are vetted by the government, but they operate as private entities. When you pay through these portals, your tax information is secure, but you are essentially making a consumer transaction that happens to be directed to the government.

Weighing the Convenience vs. Processing Fees

From a personal finance standpoint, using a credit card to pay the IRS requires a cost-benefit analysis. Processing fees for credit cards typically hover between 1.82% and 1.98% of the total payment amount. If you are paying a $10,000 tax bill, you are looking at nearly $200 in fees.

If your credit card offers 2% or 2.5% cash back, you might technically “break even” or make a small profit. However, if you cannot pay off the credit card balance immediately, the high interest rates (often 20% or higher) will quickly dwarf any benefits. Debit card payments, conversely, usually carry a flat fee (often under $3), making them a much more cost-effective choice than credit cards for those who want the speed of a card transaction without the high percentage-based costs.

What to Do If You Can’t Pay in Full: Strategic Debt Management

One of the most dangerous financial mistakes a taxpayer can make is failing to file because they cannot afford to pay. The penalty for “failure to file” is significantly higher than the penalty for “failure to pay.” If your financial situation prevents you from settling your debt immediately, the IRS offers several structured programs to manage the liability.

Short-Term and Long-Term Installment Agreements

The IRS is, in many ways, one of the most flexible creditors if you communicate with them. An Installment Agreement allows you to pay your debt over time.

- Short-term plans: If you can pay the full amount within 180 days, you can often set up a plan with no setup fee (though interest and late-payment penalties still apply).

- Long-term plans (Direct Debit): If you need up to 72 months, you can set up a monthly payment plan. Setting this up as a direct debit from your bank account often results in a lower setup fee and a higher likelihood of approval.

Offer in Compromise (OIC): Settling for Less

For those in dire financial straits, the Offer in Compromise is a program that allows you to settle your tax debt for less than the full amount you owe. This is not a “get out of jail free” card; the IRS conducts an exhaustive review of your assets, income, and expenses to determine your “Reasonable Collection Potential.” If they determine that you truly cannot pay the full amount before the statute of limitations on collection expires, they may accept a lower lump sum or a series of payments.

Temporary Delay of Collection

If paying any amount would prevent you from meeting basic living expenses (food, rent, utilities), you can request that the IRS place your account in “Currently Not Collectible” (CNC) status. This doesn’t make the debt go away—interest and penalties continue to accrue—but it does stop the IRS from taking aggressive collection actions like levying your bank account or garnishing your wages until your financial situation improves.

Best Practices for Tax Compliance and Financial Health

Navigating IRS payments is a year-round responsibility, not just an April event. Strategic financial management involves proactive steps to ensure that when the deadline arrives, the funds are available and the process is seamless.

Keeping Records and Confirming Payment Receipts

Regardless of the method used, documentation is your best defense in the event of a dispute. Always save the confirmation number for digital payments, keep the receipt for retail cash payments, and track the delivery of mailed checks. Furthermore, taxpayers should regularly check their “Tax Account” on the IRS website. This digital portal allows you to see your balance, view your payment history, and even access transcripts of your returns, providing a comprehensive view of your standing with the federal government.

Adjusting Withholdings to Avoid Future Penalties

Finally, the best way to handle paying the IRS is to minimize the “surprise” bill at the end of the year. If you find yourself owing a significant amount, use the IRS Tax Withholding Estimator to adjust your Form W-4 with your employer. For freelancers and business owners, this means refining your quarterly estimated tax calculations. By aligning your tax payments more closely with your actual income throughout the year, you preserve your liquidity, avoid underpayment penalties, and turn the daunting task of “paying the IRS” into a predictable, managed expense within your broader financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.